Roaming

What's happened with AT&T Mexico since the Iusacell acquisition?

In early 2015, AT&T finalized the acquisition of Iusacell from Grupo Salinas for over USD $2.5 billion. Through this acquisition, the U.S. telecom giant incorporated all of Iusacell’s network assets, licenses, and its 9.2 million subscribers—a figure that, at the time, accounted for approximately 8% of the total share of mobile contracts in Mexico.

In a press release, former AT&T CEO Randall Stephenson emphasized the acquisition’s strategic significance:

“We look forward to bringing more wireless competition to Mexico along with an improved mobile Internet experience for customers. Expanding and enhancing Iusacell’s mobile network to cover millions of additional consumers and businesses is our top priority.”

Just four months later, AT&T announced the acquisition of Nextel for USD $1.9 billion. The merger of Iusacell and Nextel marked a clear move to aggressively compete with América Móvil for leadership in Mexico’s wireless market.

So, what’s happened to AT&T’s business in Mexico since the acquisition?

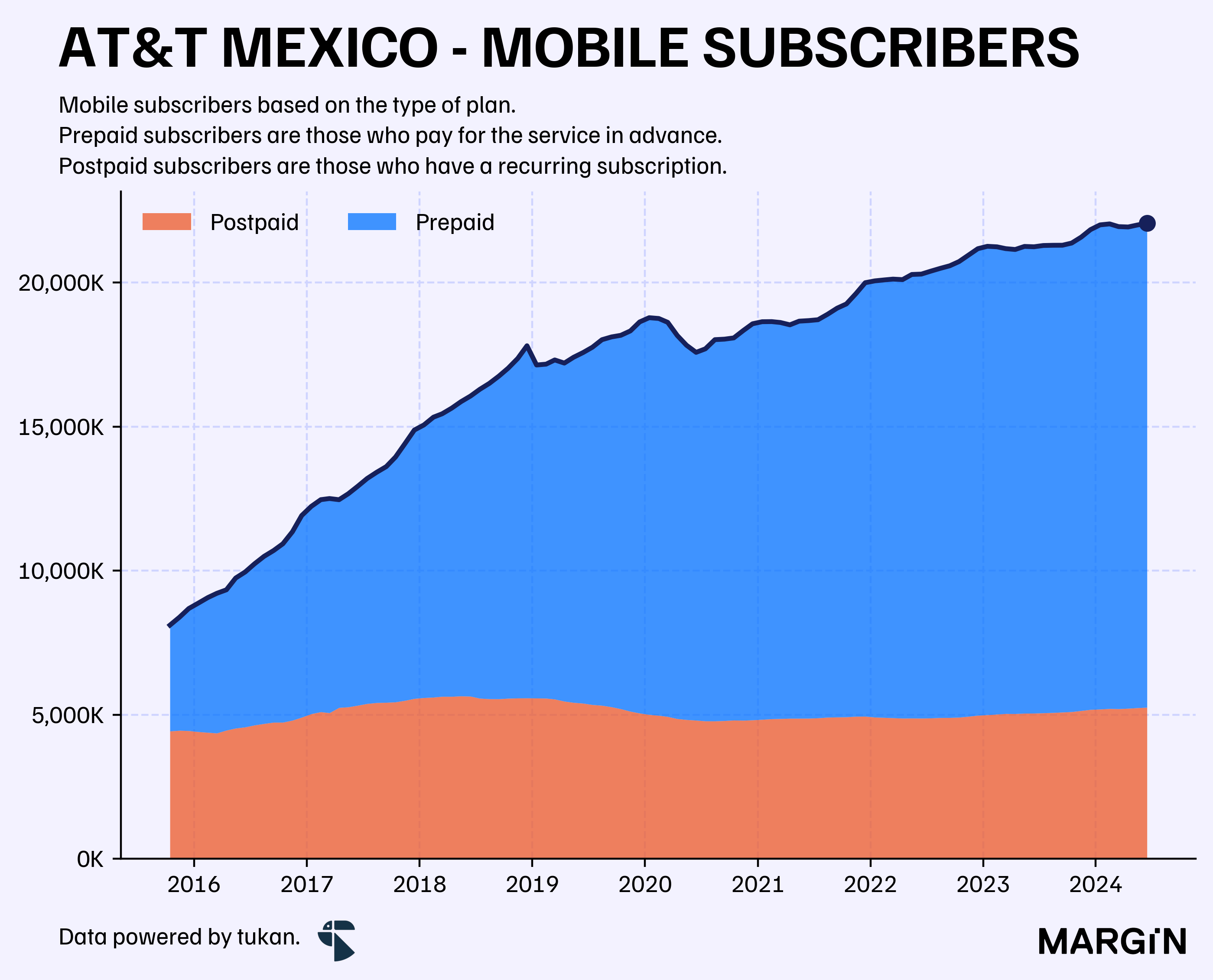

According to data from the Mexican regulator (IFT), AT&T’s subscriber base has grown at a compound annual growth rate (CAGR) of 12% since their entrance into the Latin American market. This growth has increased the total number of customers from 8 million at the end of October 2015 to over 22 million as of the second quarter of 2024.

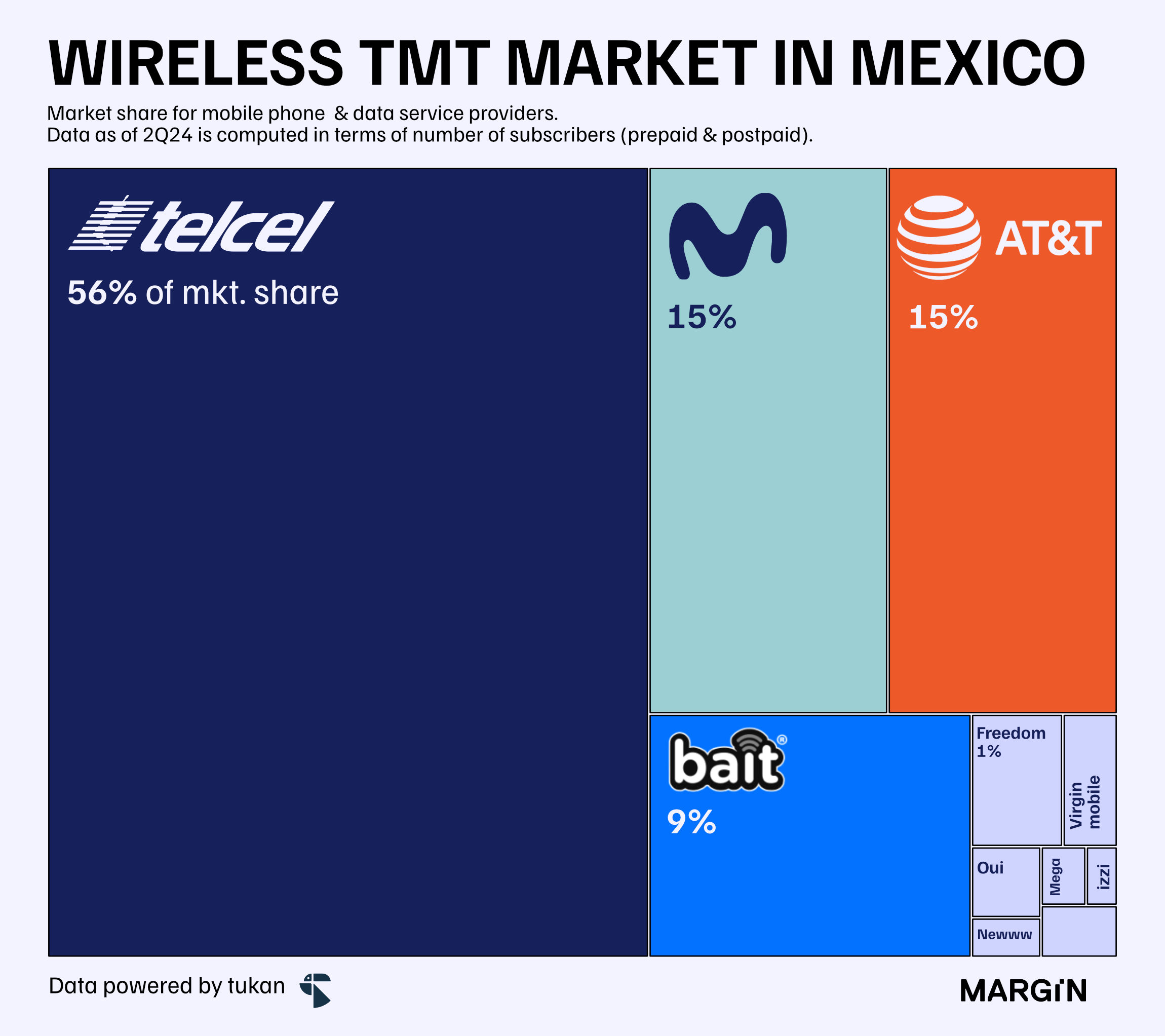

Since 2015, AT&T’s market share in Mexico reached a peak of 16.2% in September 2023 but has since declined to 14.8%. This decrease is primarily attributed to intensified competition from well-funded mobile virtual network operators (MVNOs) such as Bait (Walmart), izzi Móvil (Televisa), Oui (Grupo Salinas), and Mega Móvil (Megacable).

As shown in the chart below, postpaid customers for the American telecom giant have remained relatively stable since the brand’s inception in late 2015. In contrast, prepaid customers have driven most of the company's growth.

In the wireless industry, postpaid customers are generally considered more valuable due to their higher average revenue per user (ARPU), lower churn rates, and greater lifetime value.

In the Mexican market, the mobile space has traditionally been dominated by prepaid customers. As of the second quarter of 2024, 84% of all mobile lines in the country were prepaid — a proportion that has remained virtually unchanged since 2013.

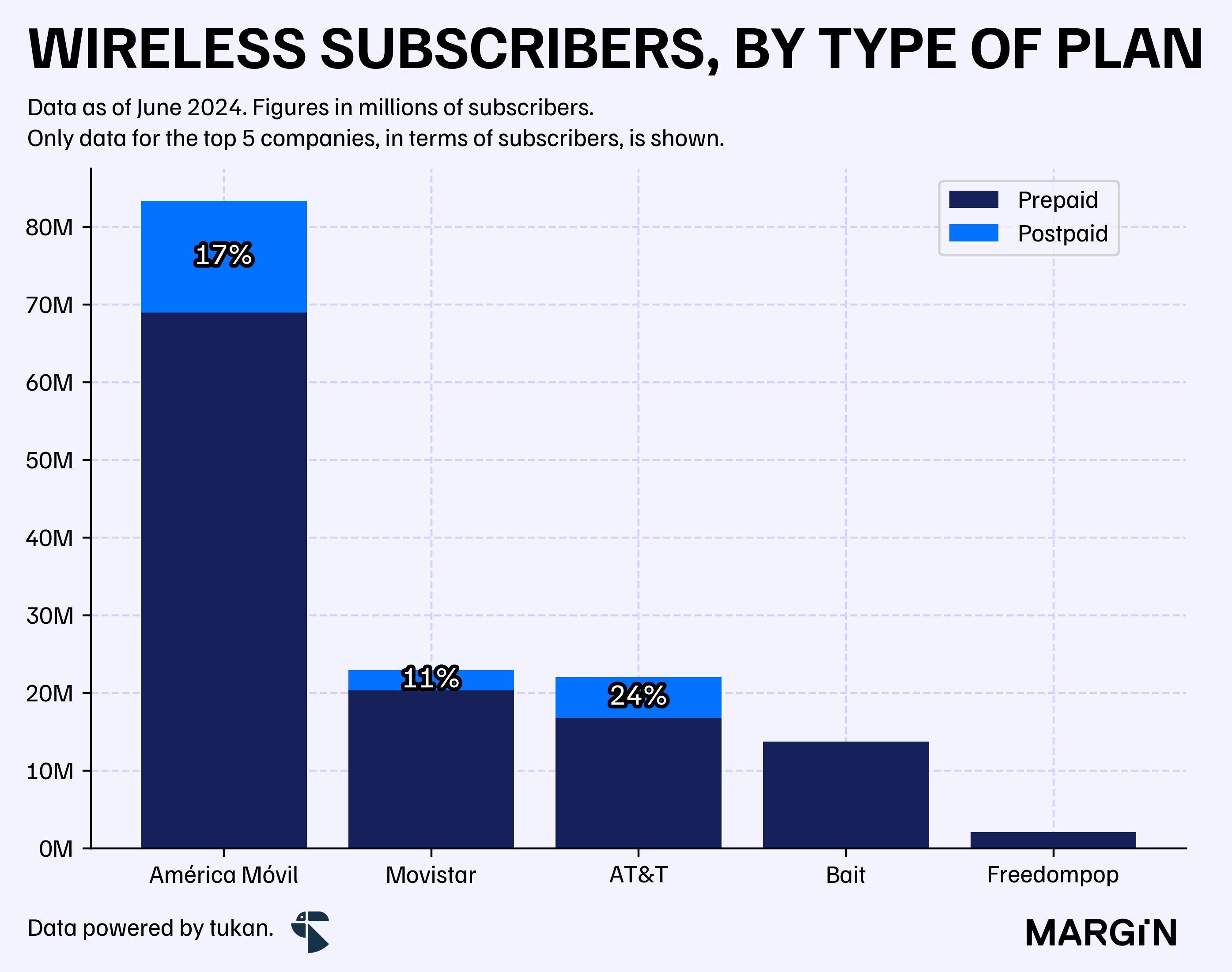

Regulatory data shows that among the five companies with more than 1% market share in Mexico, AT&T has the highest exposure to postpaid subscribers. As of June 2024, postpaid clients accounted for approximately 23% of AT&T’s portfolio.

This ratio was of 55% when they took over in 2015.

On the other hand, MVNOs like Megacable and izzi operate almost entirely on postpaid plans. However, their market presence is still quite limited, representing just 0.3% and 0.2% of total subscribers in the country, respectively.

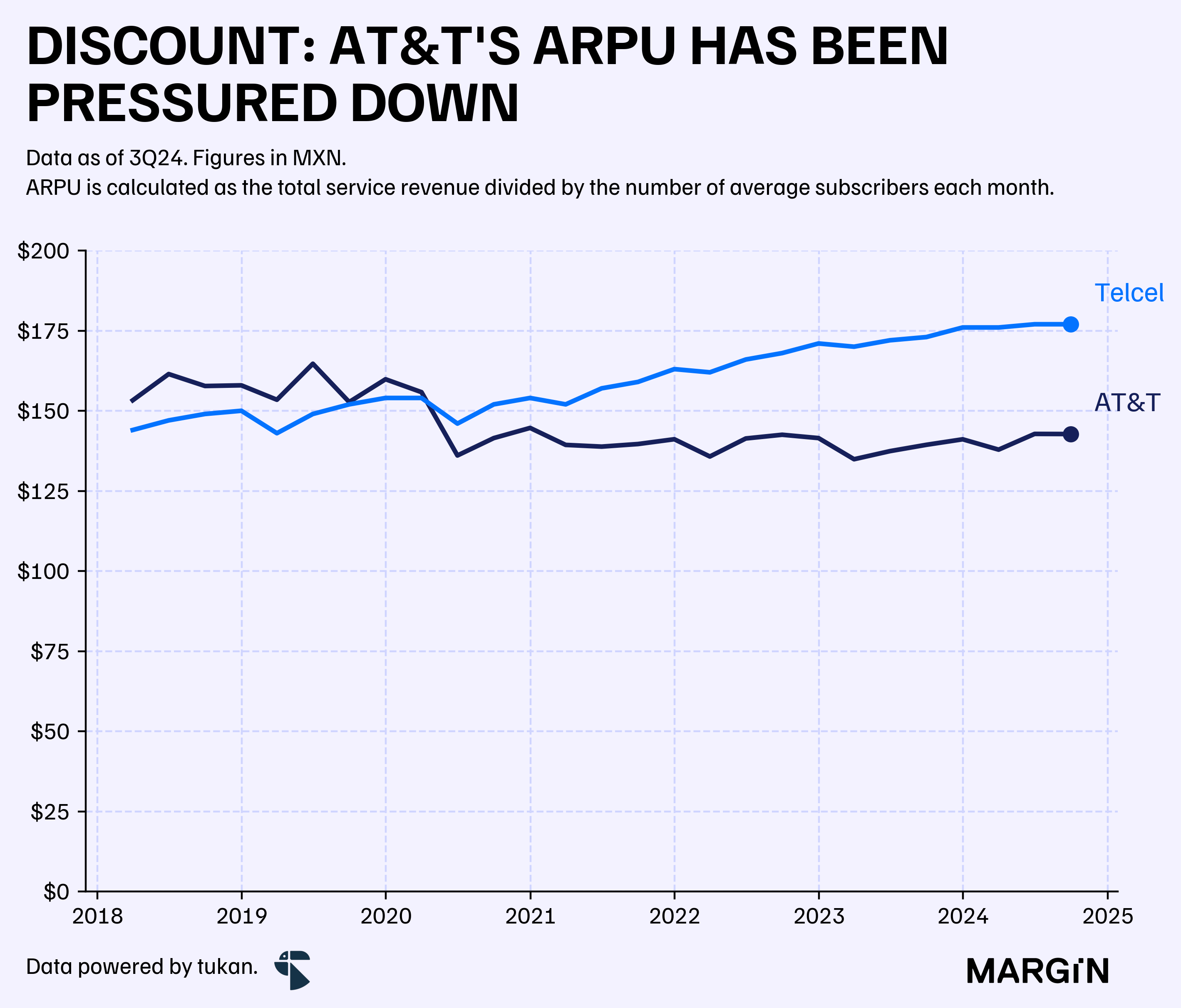

In theory, this would imply that AT&T would have higher than average ARPUs (average revenue per user), and lower churn rates than the competition.

However, company filings from the three largest players in the space point towards a different trend.

Based on company data, AT&T’s ARPU has recently been 20% lower than Telcel’s — a company with a much higher share of prepaid customers.

As of the latest quarter, AT&T’s ARPU stood at $142 pesos per user, Telcel’s at $177 pesos and Movistar’s is estimated at $100 pesos per month.

This highlights how AT&T has had to further contract ARPUs in order to continue to gain market share in the country.

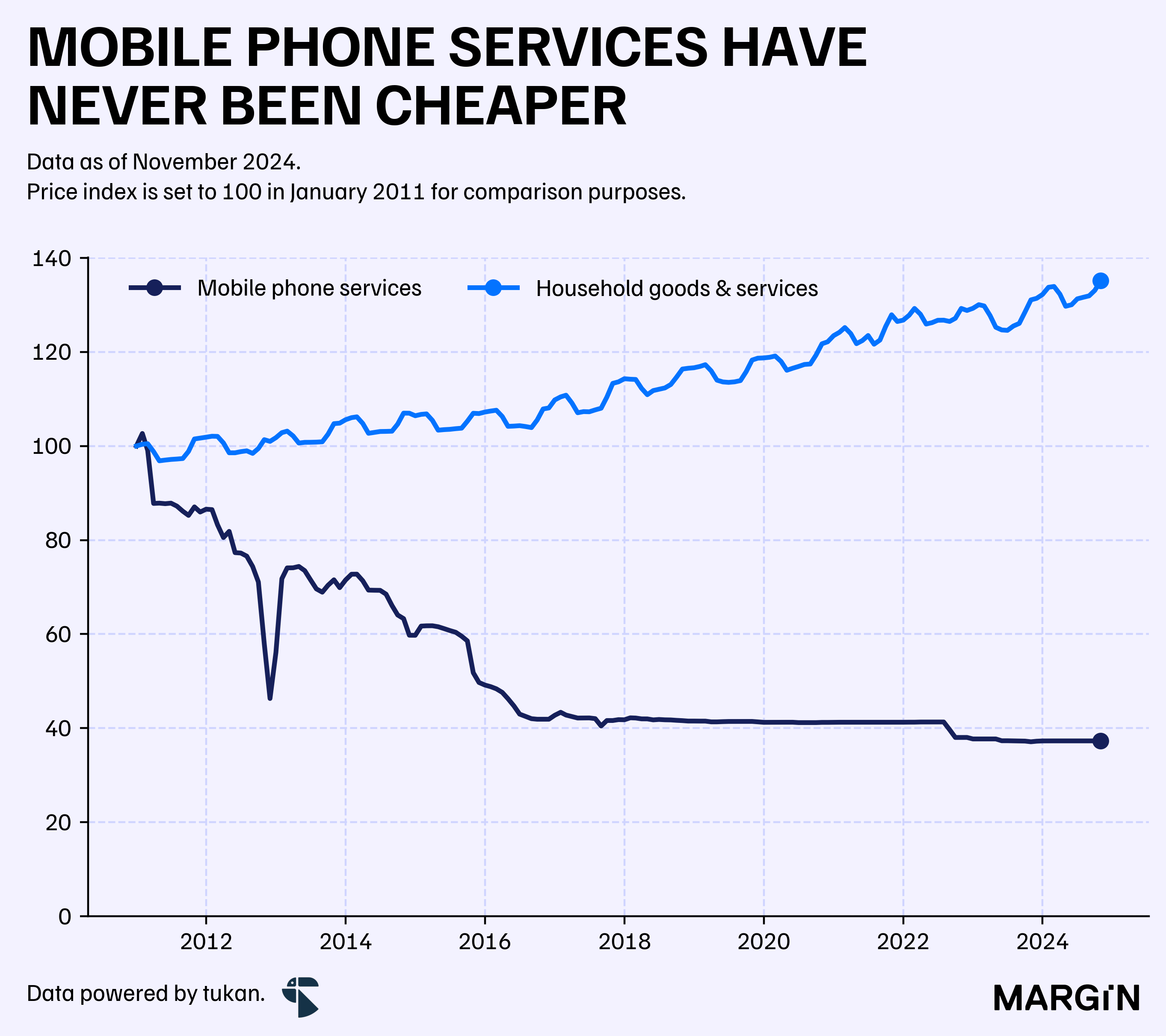

More so, cost of mobile services as a whole for consumers have reached record lows — showcasing a sharp declines each year since 2011 and reaching a “stable” price point in 2018.

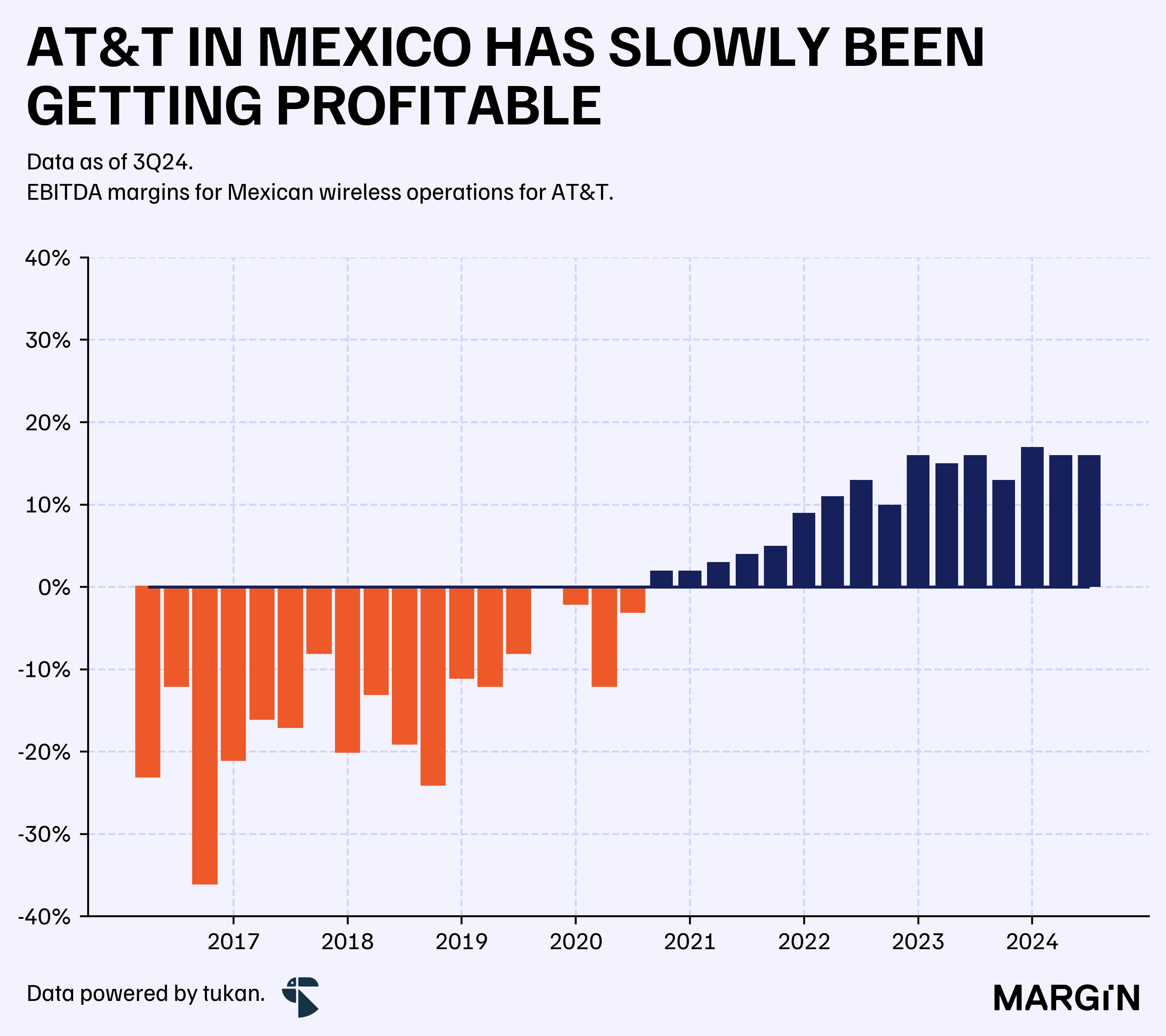

In spite of this, the company has managed to work towards financial sustainability across their Mexican operations. Positive EBITDA was first reached in 2020, and since 2Q22 the Latin American business unit has consistently achieved +10% EBITDA margins.

Although not exactly “apples to apples”, América Móvil’s Mexican wireless operations (Telcel) posted a 32% operating margin during 2023.

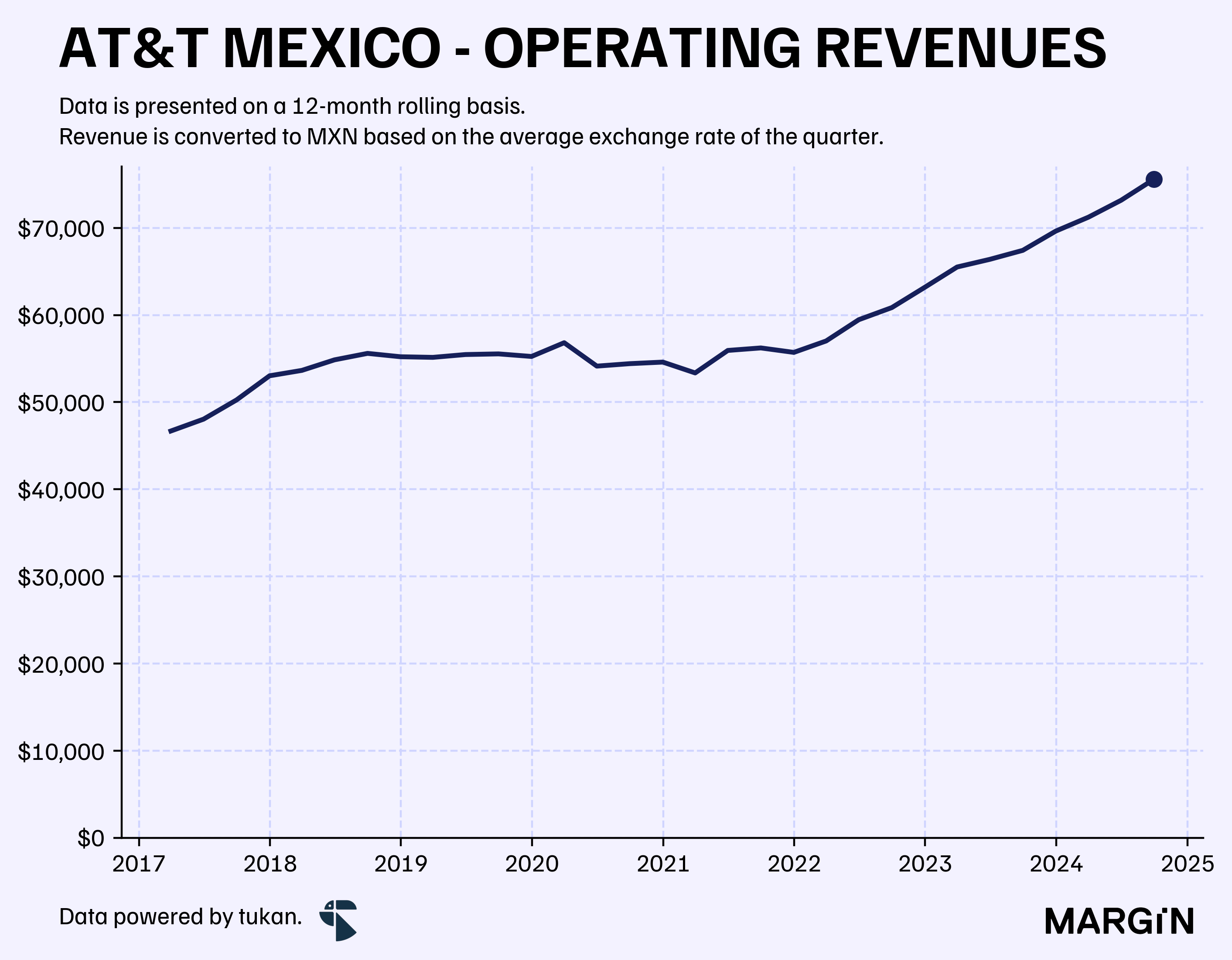

According to the company’s press releases, approximately 3.2% of AT&T’s total operating revenues were generated in Mexico during 2023, an increase of more than 1.4 percentage points compared to 2020.

Overall, full-year revenues from the Mexican division have grown at a compound annual growth rate (CAGR) of 6.5% since 2018, reaching over USD $3.9 billion in 2023. However, when adjusted for foreign exchange rates, the CAGR for this business segment’s top line drops to +4.7%.

For context, the country’s incumbent, América Móvil, posted a 2.9% CAGR in its wireless operations in Mexico over the same period.

Despite this modest long-term growth, AT&T’s Mexican division has shown significant top-line expansions, particularly since early 2022. With the exception of two quarters, operating revenues grew at a double-digit pace starting from 1Q22—a trend largely driven by strong growth in equipment-based revenues.

In a company like AT&T, equipment-based revenues primarily consist of smartphone sales to post-paid customers.

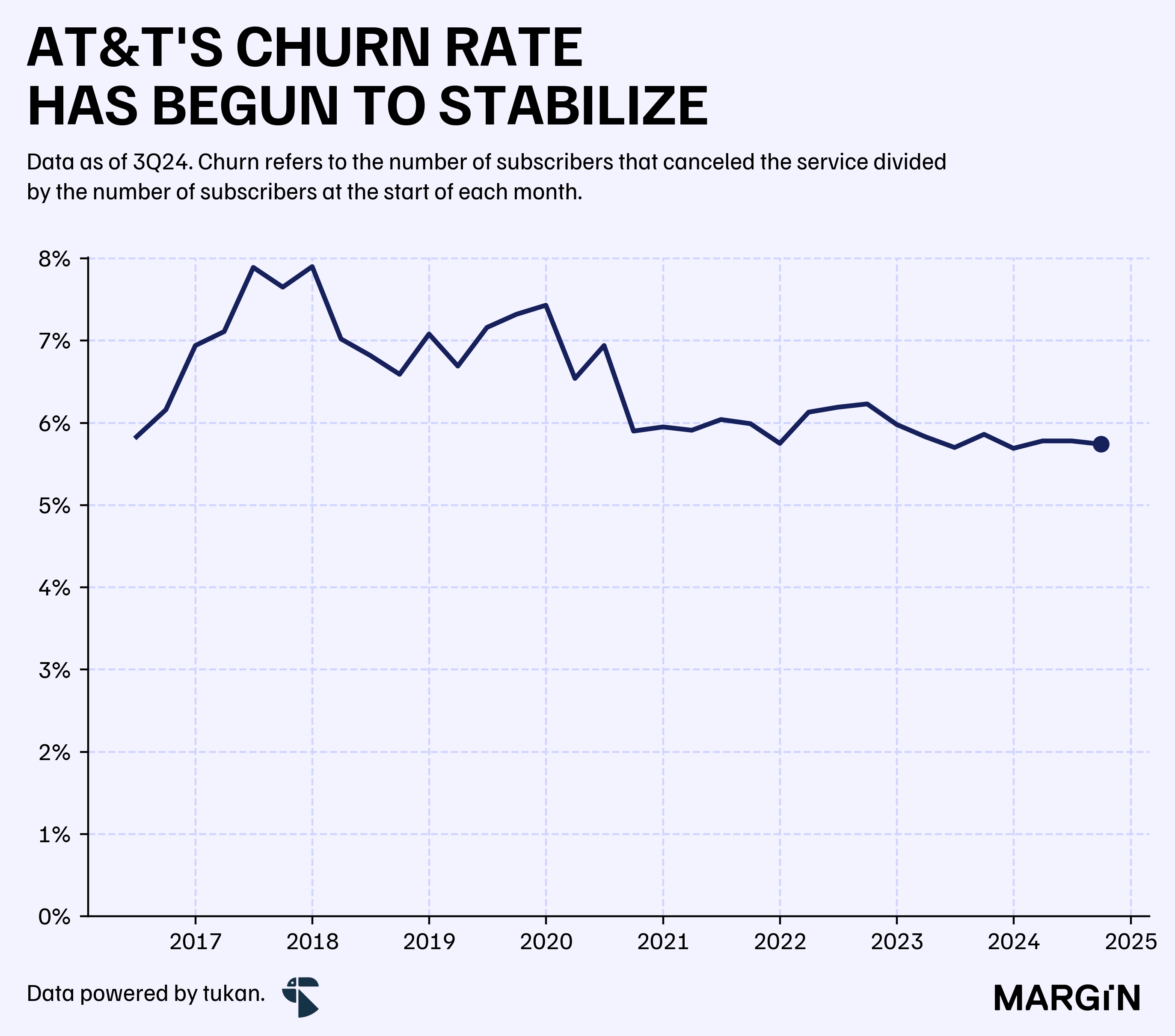

On top of this, the company has managed to stabilize customer churn in recent quarters, finally managing to break the +6% barrier in 2023. However, there’s still much room for improvement for this KPI, given that América Móvil has consistently kept churn rates well below 5%.

Mexican wireless operations for América Móvil reported a churn rate of just 3.2% at the end of 3Q24 — a ratio 2.5 percentage points lower than AT&T.

This overall improvement for the company’s operations in Mexico has coincided with the change in management in 2021, year in which Mónica Aspe was reassured her role as CEO. Position she won after managing the company for a little over a year under an interim role.

On such a challenging space, where the incumbent player has practically dominated the market for decades, signs of improvement on AT&T’s operations should be regarded as a positive sign for consumers and the competitive landscape in the telecom market.

After Telefónica Movistar returned the last of it’s spectrum to the country’s regulator, AT&T remains the only pure mobile network operator in the country willing to compete against Telcel.

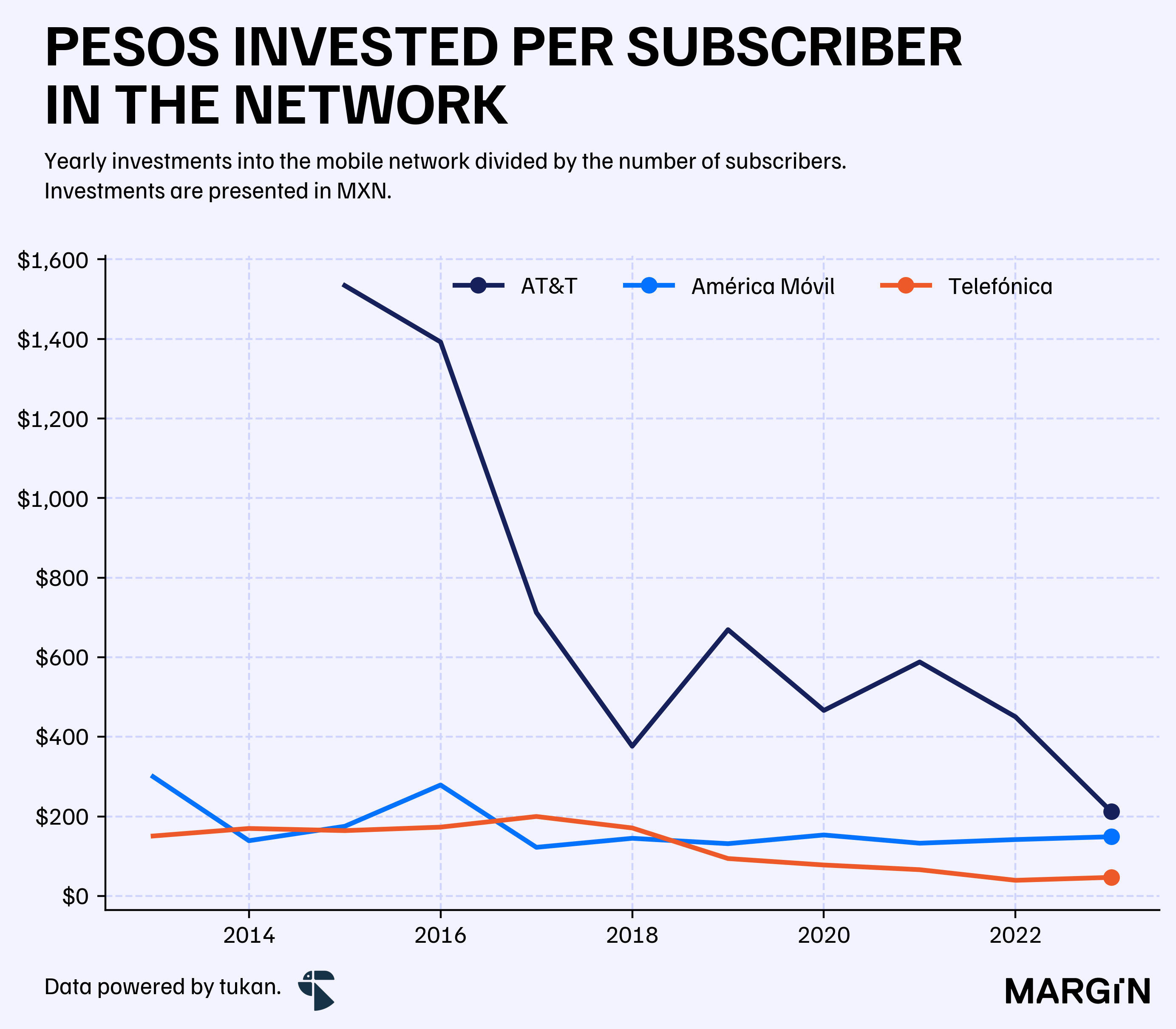

The numbers, in terms of investment into the network per subscriber required to set up and grow the operation speak for themselves. After an obvious high capital intensive period when the company had to set up shop, AT&T has continued to invest more than 40% per subscriber than it’s counterparts.

Will we continue to see the company willing to compete and invest in such a tight space?

Despite the clear improvement in the company’s operations in Mexico, the reality is that this business segment remains marginal in the company’s operations. Whether the executive team still sees Mexico as a priority and are willing to make significant investments to compete against such a tough opponent remains to be seen.