SPEI

The explosive growth of Mexico's main electronic payment system.

During the first 11 months of 2024, total SPEI transactions in Mexico soared to an impressive 4.5 billion operations. This translates to a staggering average of over 156 transactions per second—an increase of 38% compared to 2023 and seven times the volume recorded in 2019.

Historically, December has accounted for approximately 10% of the annual transaction volume over the past three years. If this trend holds, 2024 is on track to surpass 5 billion operations within a single year—a fivefold increase compared to 2020.

Adjusting for the missing December data, this could amount to over $325 trillion pesos in transfers. To put this massive figure into perspective:

It is 83 times—yes, eighty-three times—the total value traded in the cash equities market of the Mexican Stock Exchange (BMV).

It’s almost 10 times Mexico’s GDP (as of 2024).

The daily volume processed is roughly the same as WALMEX’s 2023 annual revenues.

According to the central bank, this translates to an average of approximately $65,000 pesos per transfer—a figure that is 66% lower than in 2020.

Reflecting on the evolution of the SPEI network and its integration into daily life, it’s remarkable to consider that in 2010, the average SPEI transfer was close to $1.8 million pesos.

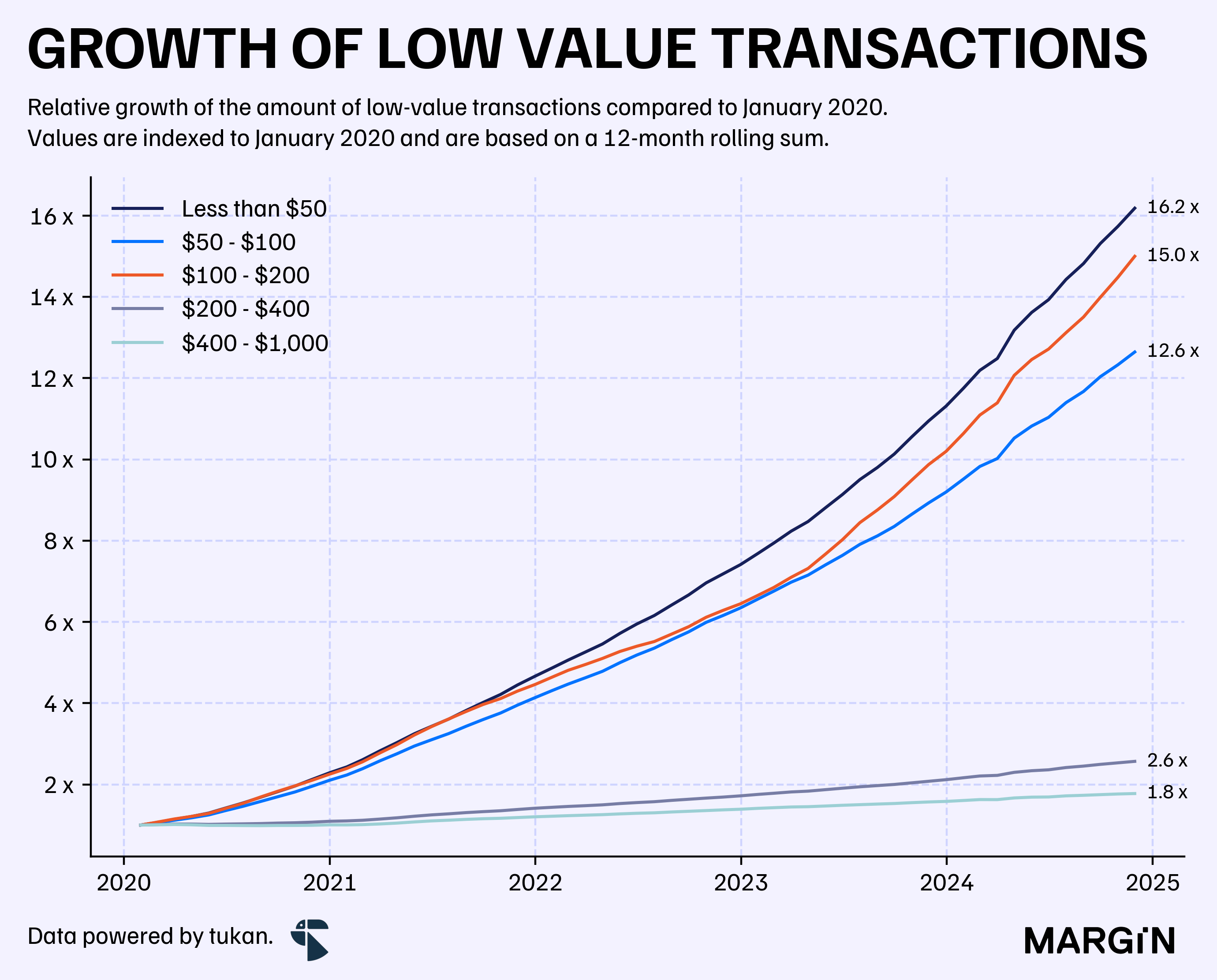

The previous figures showcases the important increase of “retail” transactions in the system. In fact, just during the first 11 months of 2024, there were more than 327 million transactions in the country below the $50 peso threshold — implying $8.9 billion pesos of transactional value for this type of operations.

A clearer picture of the retail adoption of this product is reflected in the following chart were we can see how the volume of transactions has multiplied itself, in some cases, by more than 10 times.

The chart above highlights, among other insights, that the number of transactions with a transfer value between $100 and $200 pesos has surged 16-fold since the start of 2020—an extraordinary average annual growth rate of 78%.

For illustrative purposes, there were approximately 21 yearly transactions per capita below the $1,000 peso threshold in 2024, and just over 30 transactions per capita when considering all transactions in the country.

While these figures are impressive compared to previous years, they still fall significantly short of Brazil’s PIX system, launched at the end of 2020. According to BCB data, PIX achieved over 300 transactions per Brazilian—a figure nearly 10 times higher than SPEI.

According to the Brazilian central bank, at least 72% of Brazilians have paid at least once using PIX.

In a sense, this gives light into just how massive SPEI (or any other digital payment system) could become for Mexico if it gains the level of success PIX achieved in Brazil.

On the other end of the spectrum are high-value transactions.

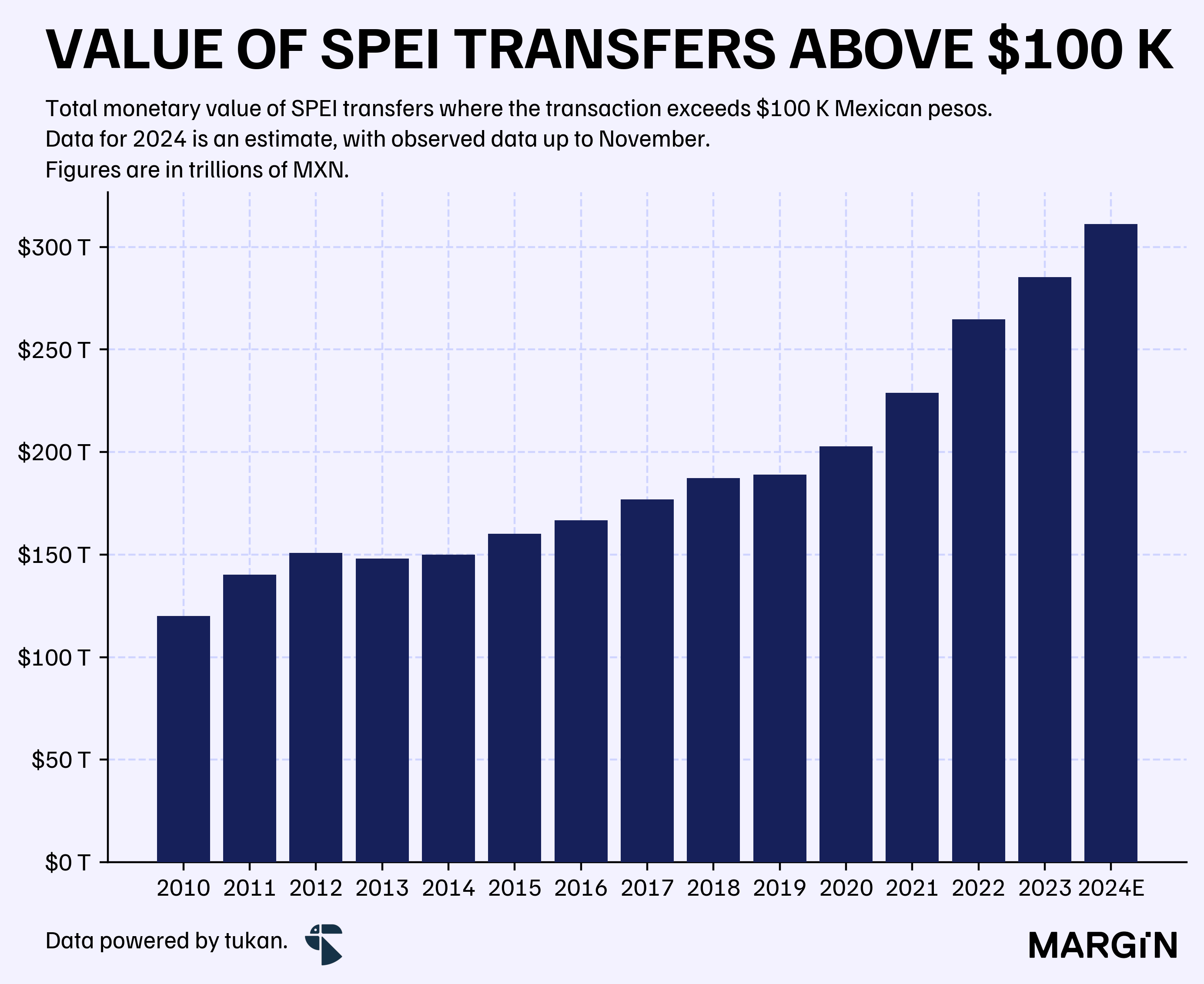

According to Banxico, the monetary value of transactions exceeding the $100,000 peso threshold has grown at a 5-year CAGR of 10%, increasing from $190 trillion pesos in 2019 to an estimated $311 trillion pesos in 2024.

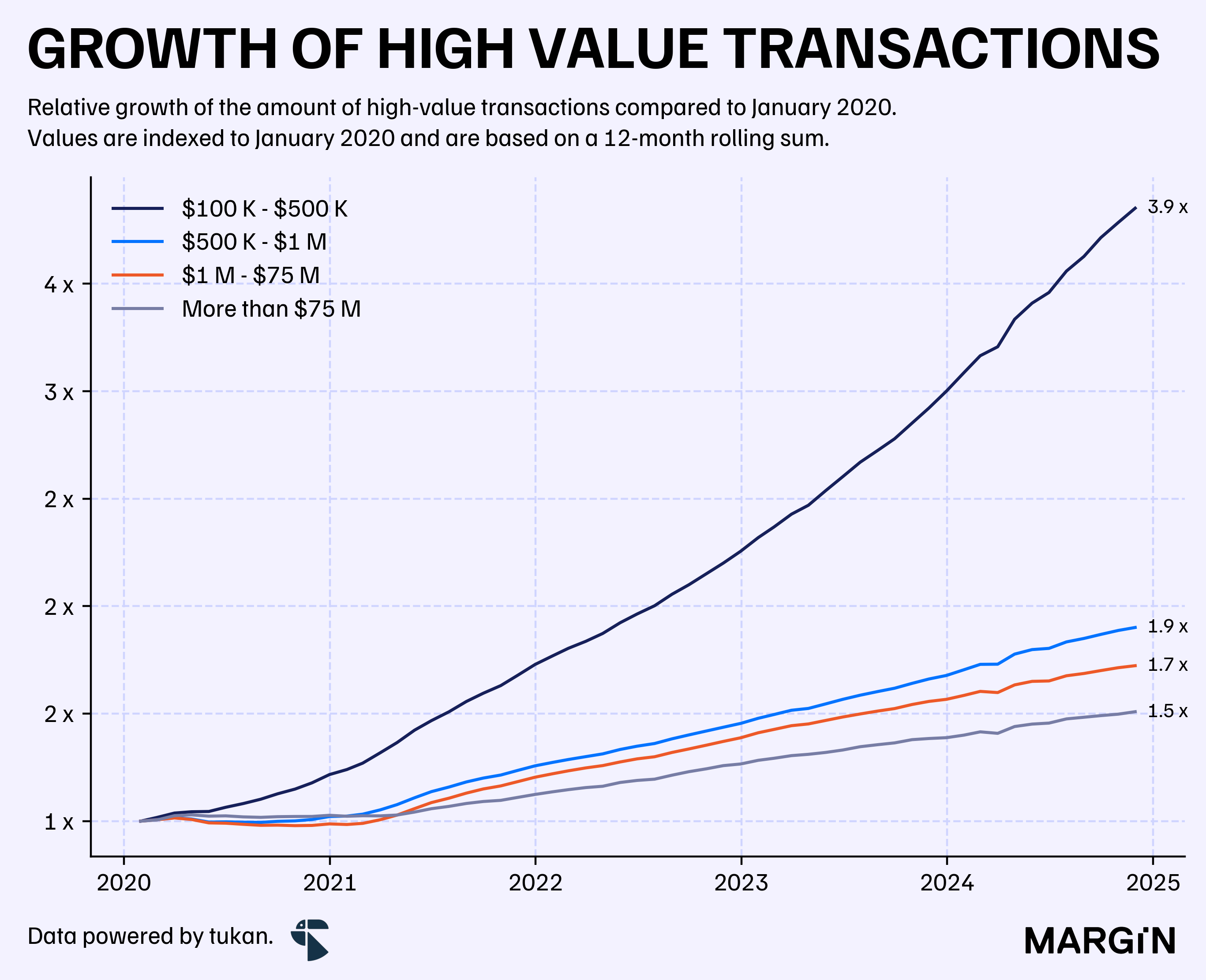

Although these high-value transfers are not growing as rapidly as the “retail” side of the equation, they still exhibit significant growth. For instance, transactions exceeding $75 million pesos are now 50% higher than in 2020, while transfers between $100,000 and $500,000 pesos have nearly quadrupled in volume over the past four years.

As of 2023, Banxico reported over 80 institutions participating in the SPEI network.

While the names and market shares of individual participants are not disclosed, the anonymized data published by the regulator offers some intriguing insights.

For example, the largest player by volume processed just over 28% of total transfers, yet accounted for only 12% of the total monetary value. On the other hand, another participant handled an impressive 35% of the total monetary value in 2023, despite processing just 36,000 transactions, according to Banxico.

Unlike Brazil’s PIX system, which was specifically designed to handle low- to medium-value transfers, SPEI has evolved into a payment network serving both the retail and corporate markets in Mexico.

Banxico’s efforts to establish a dedicated system for low- to medium-value operations have not gained traction. CoDi, a QR-based payment system built on SPEI’s infrastructure, rarely exceeded 20,000 daily transactions, a stark contrast to PIX’s widespread adoption.

This dual role of SPEI, serving both high-value corporate needs and low-value retail transactions, positions it uniquely within the global payments landscape.

Whether SPEI can reach the scale of PIX and truly unify Mexico’s payment ecosystem remains to be seen, but its current trajectory suggests a future where it could continue to play transformative role in the country’s financial infrastructure.