The 20K Club

The numbers behind the Mexican listed companies with over 20 thousand employees.

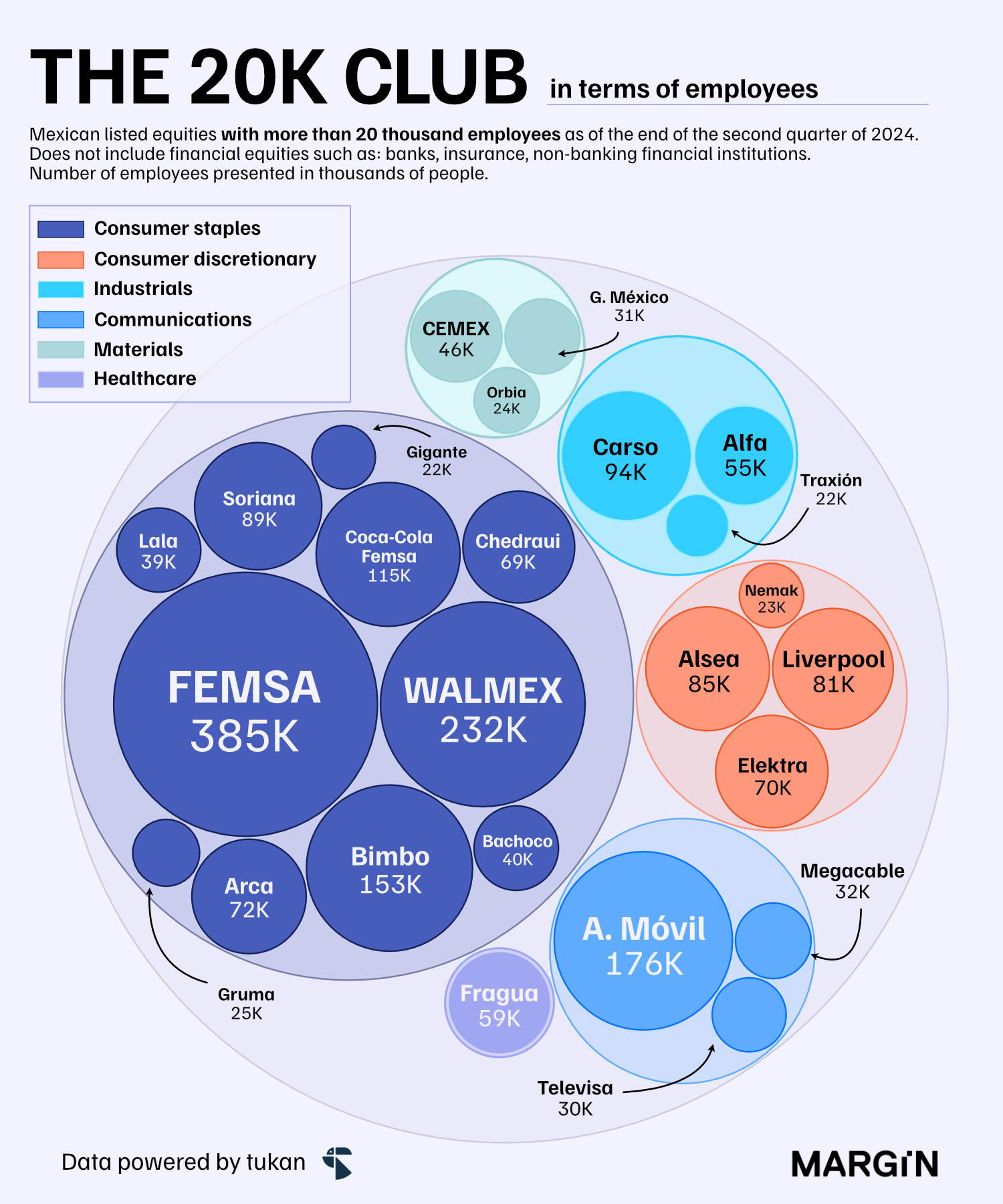

According to the most recent filings from the Mexican Stock Exchange (BMV), 25 listed companies reported employing a workforce of over twenty thousand people. In total, these businesses employ just over 2 million individuals and hold almost three quarters of the market’s total assets—a figure just shy of $7.6 trillion pesos.

To put this data into context, only two states in Mexico—Mexico City and Jalisco—have a higher formal employment figure than the combined headcount of these 25 companies.

Based on the latest data from the Mexican Social Security Institute, FEMSA alone has more people on their payroll than the entire formal workforce of 14 states in the country, including: Aguascalientes, Durango and Guerrero.

How do these giants differ from the rest of the market? Read on to find out.

Please note that in this article we do not include (or analyze) financial institutions such as: Banorte, Quálitas, Inbursa, BanBajío, etc.

We also maintain Lala and Bachoco despite their recent delisting from the market for informational purposes.

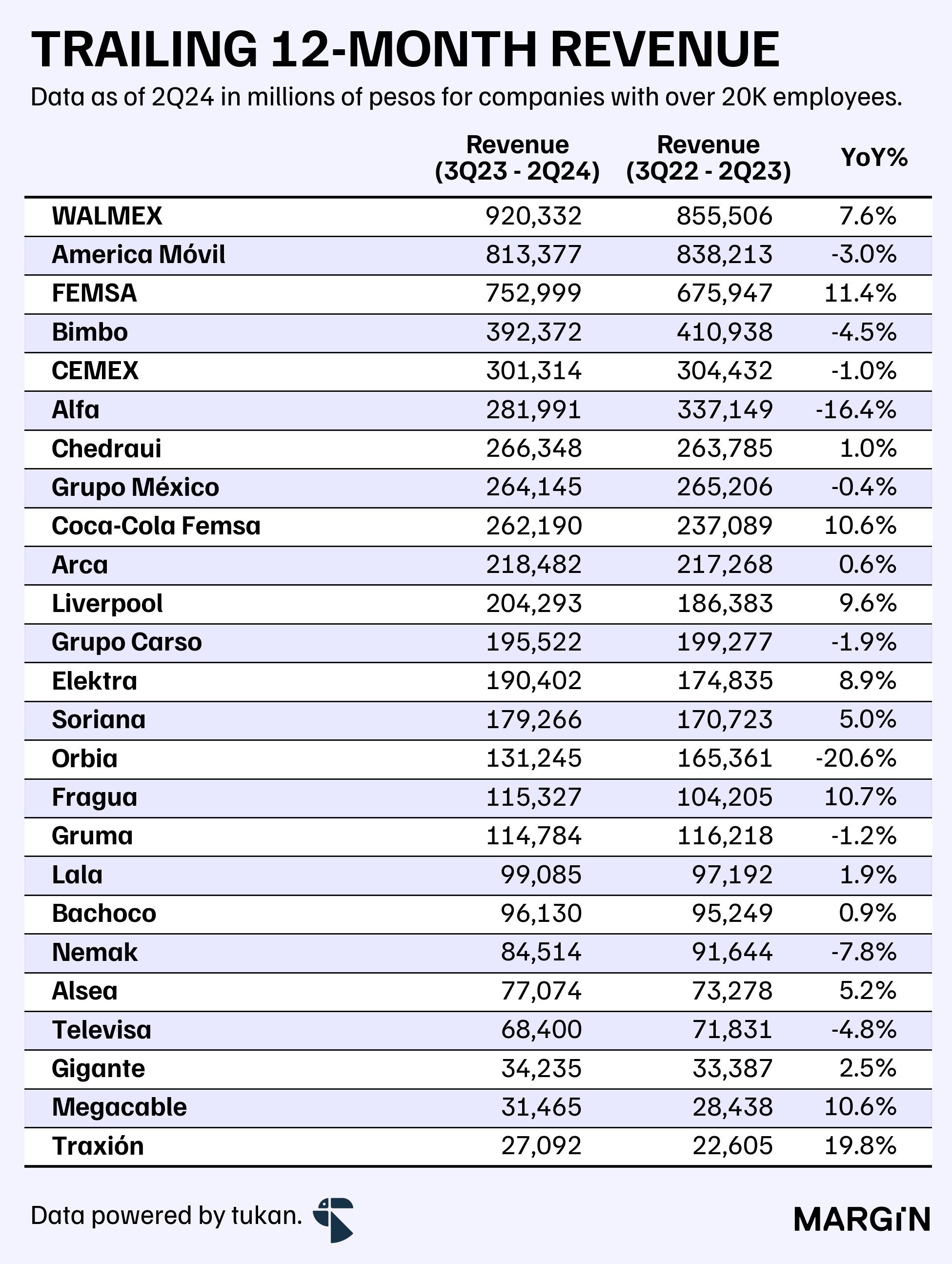

According to data from company filings, these 25 businesses reported revenues exceeding $6.1 trillion pesos during the past 12 months, implying a YoY increase of 1% for their top-line. The rest of the listed companies registered a revenue figure of $1.2 trillion pesos, contracting 6% versus the previous year.

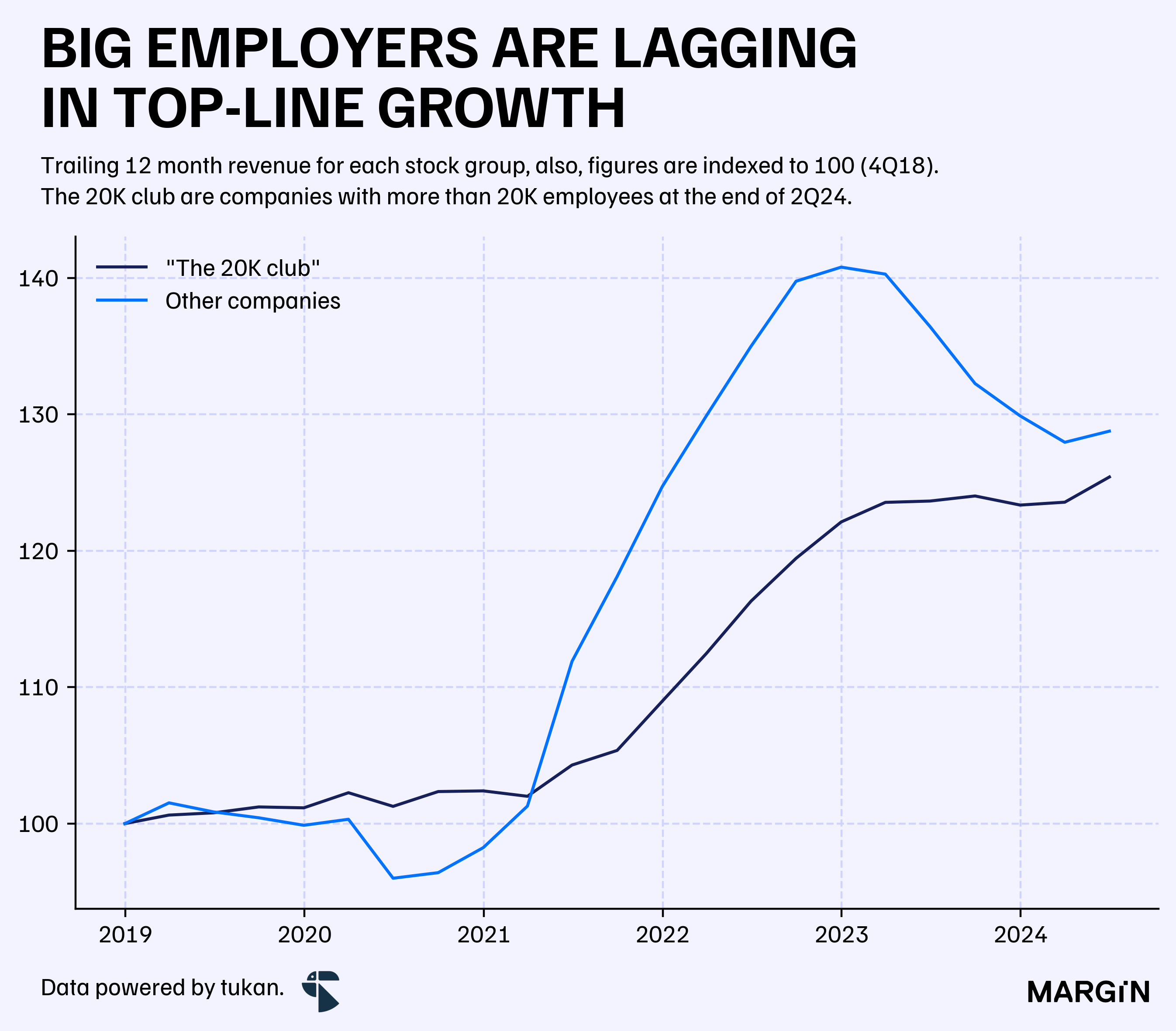

In aggregate, “the 20K club” has been growing at a CAGR of 4.5% over the past 5 years (2019 - 2023), a figure 85 basis points lower than the rest of the market.

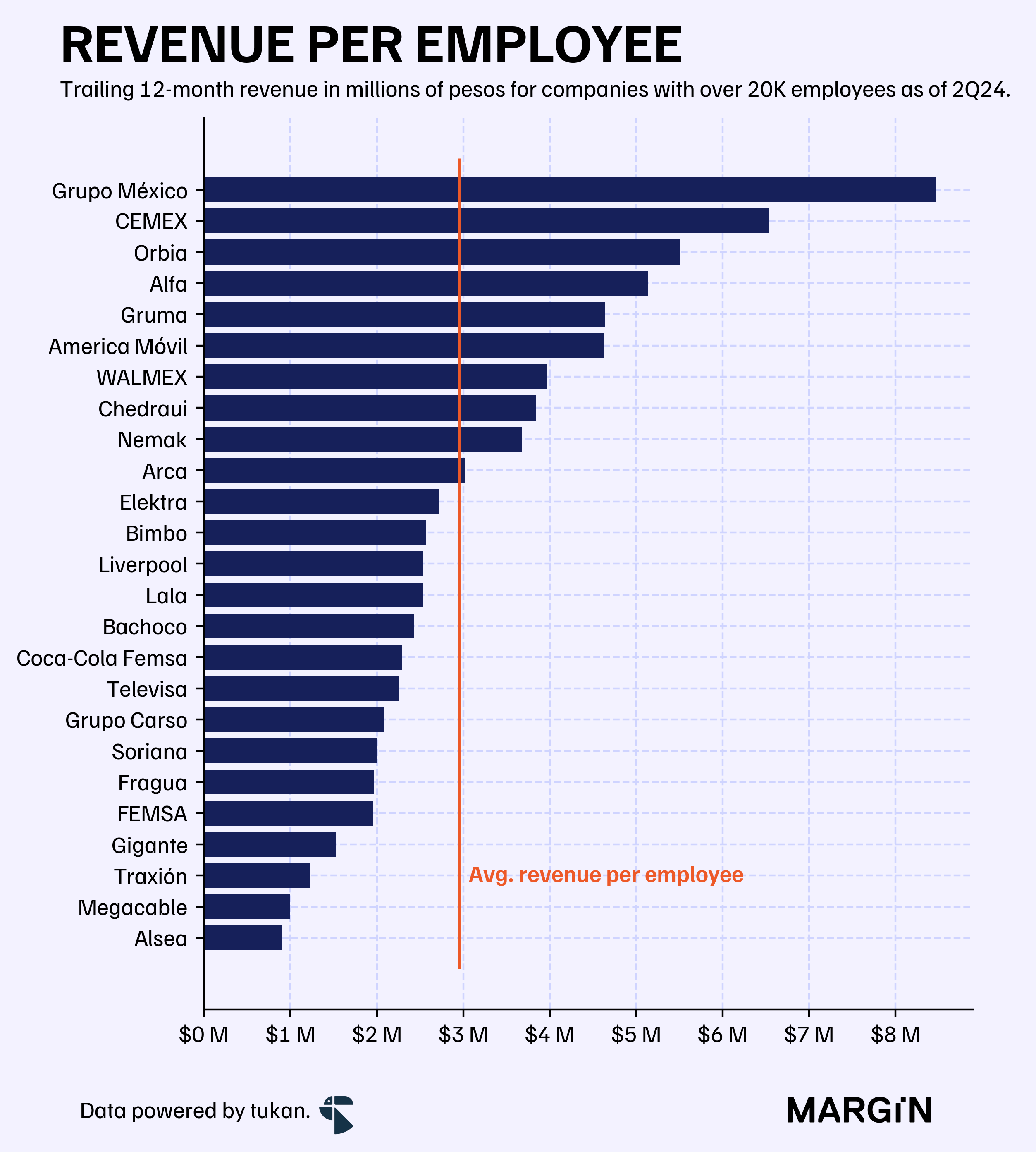

In terms of revenue per employee, the average for these companies was of about $3 million pesos per headcount — a figure 36% lower than the rest of the Mexican market, and one which has been increasing at a modest CAGR of 2% during the past 5 years.

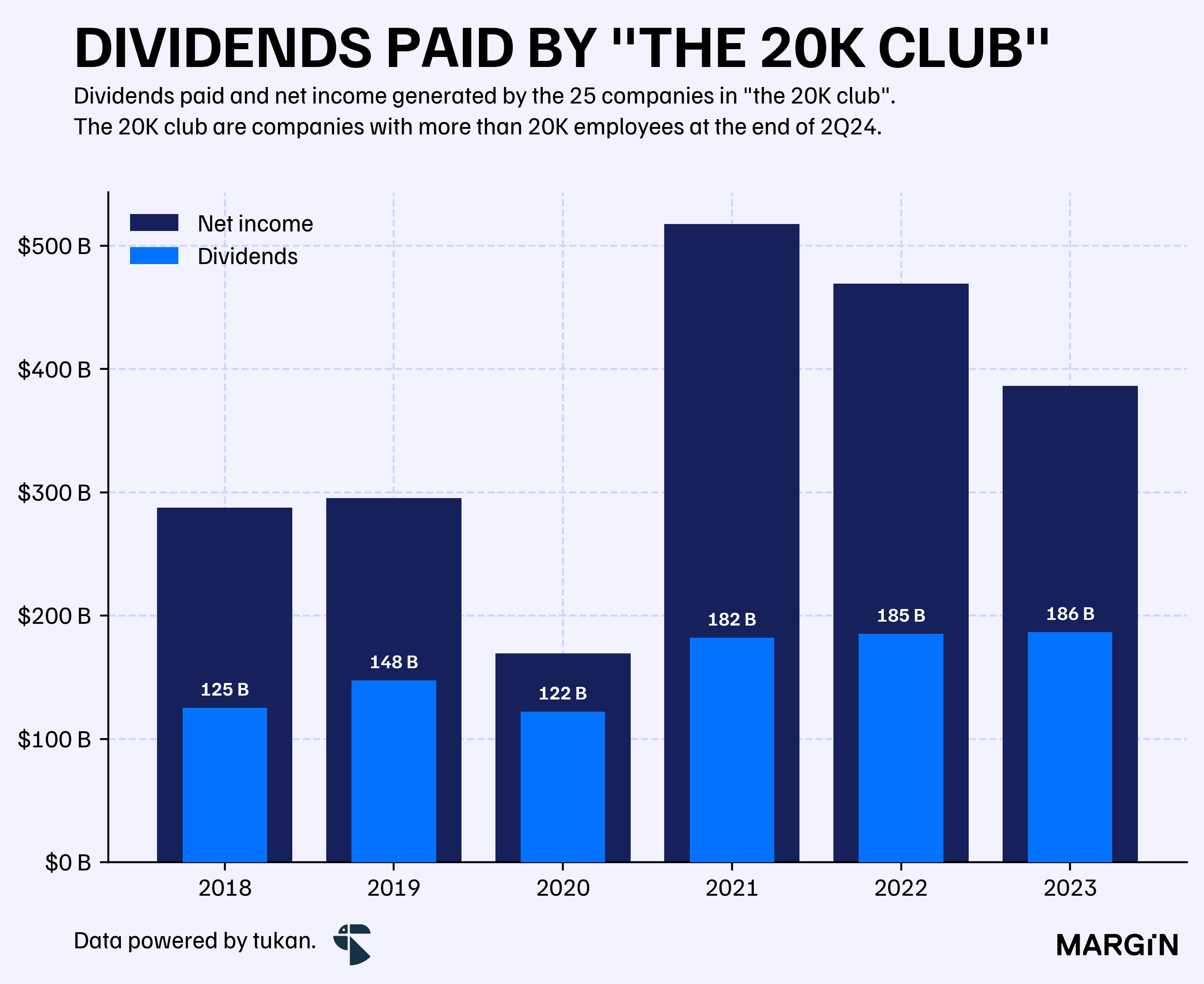

Interestingly, these stocks are more prone to distributing dividends to their investors than the rest of the market. In 2023, 20 out of the 25 companies in this group paid dividends, compared to less than half of the remaining businesses.

In total, dividends from these companies amounted to more than $186 billion pesos in 2023—equivalent to 48% of the group’s total profits during that same year (including those that didn’t pay dividends).

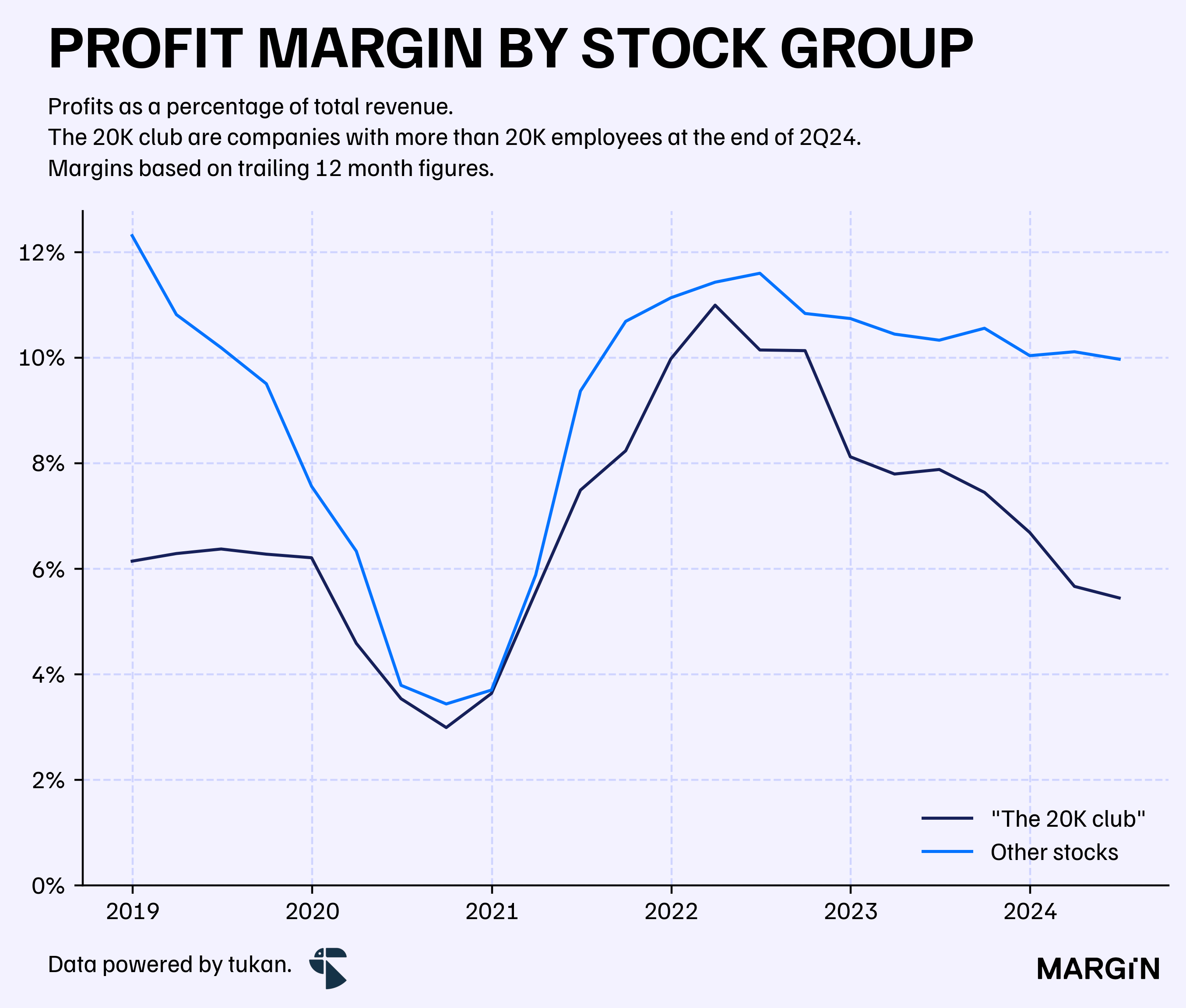

Naturally, these businesses are expected to be more mature, given the enormous headcount under their control. However, does this make them more “relatively” profitable than the rest?

Quite the opposite, since most of the companies operate in industries that are capital intensive, such as: retail, industrials, TMT and materials.

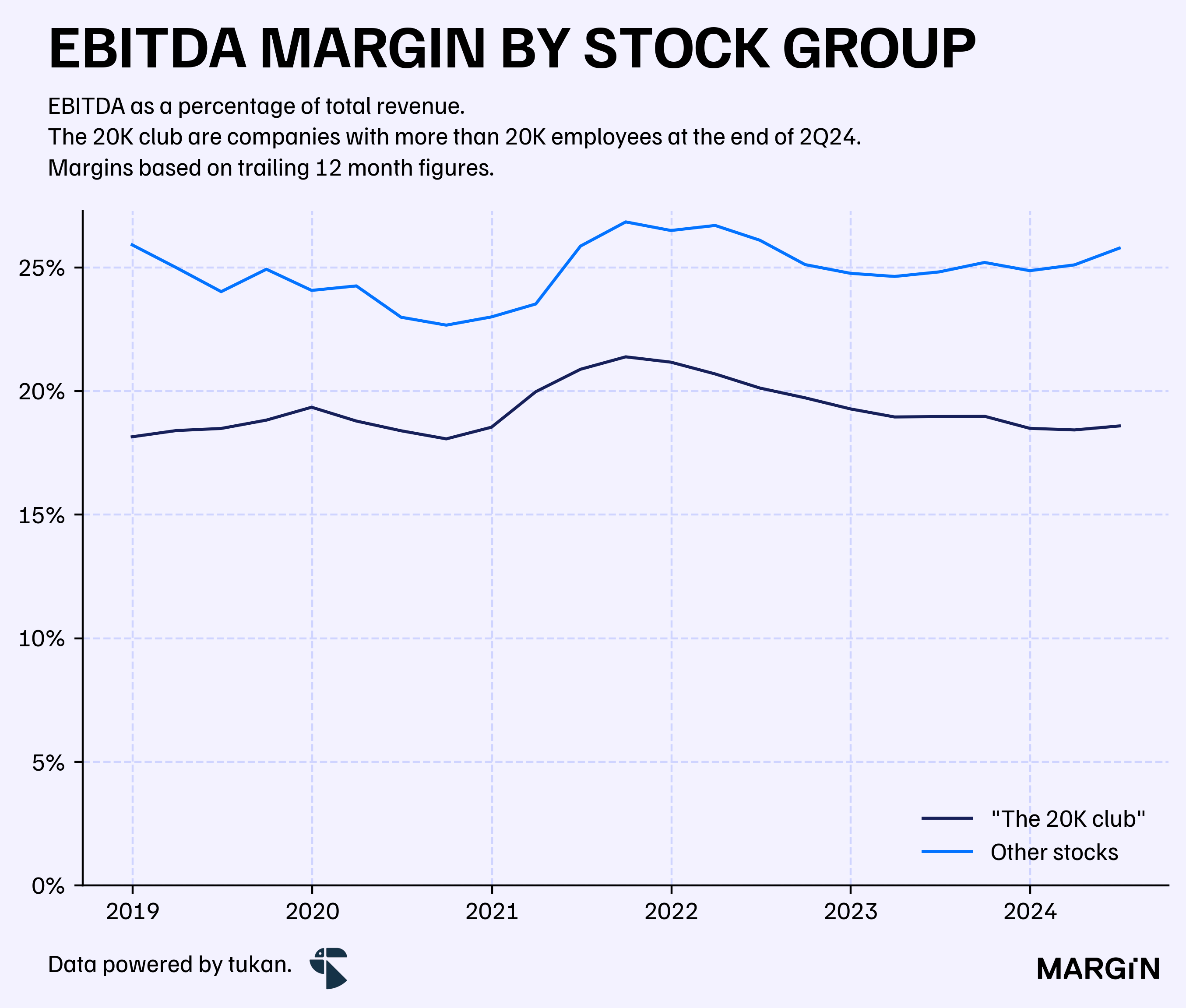

However, even when inspected through the lens of EBITDA margins. The “others” still have the upper hand in terms of profitability.

What does the market think about these stocks?

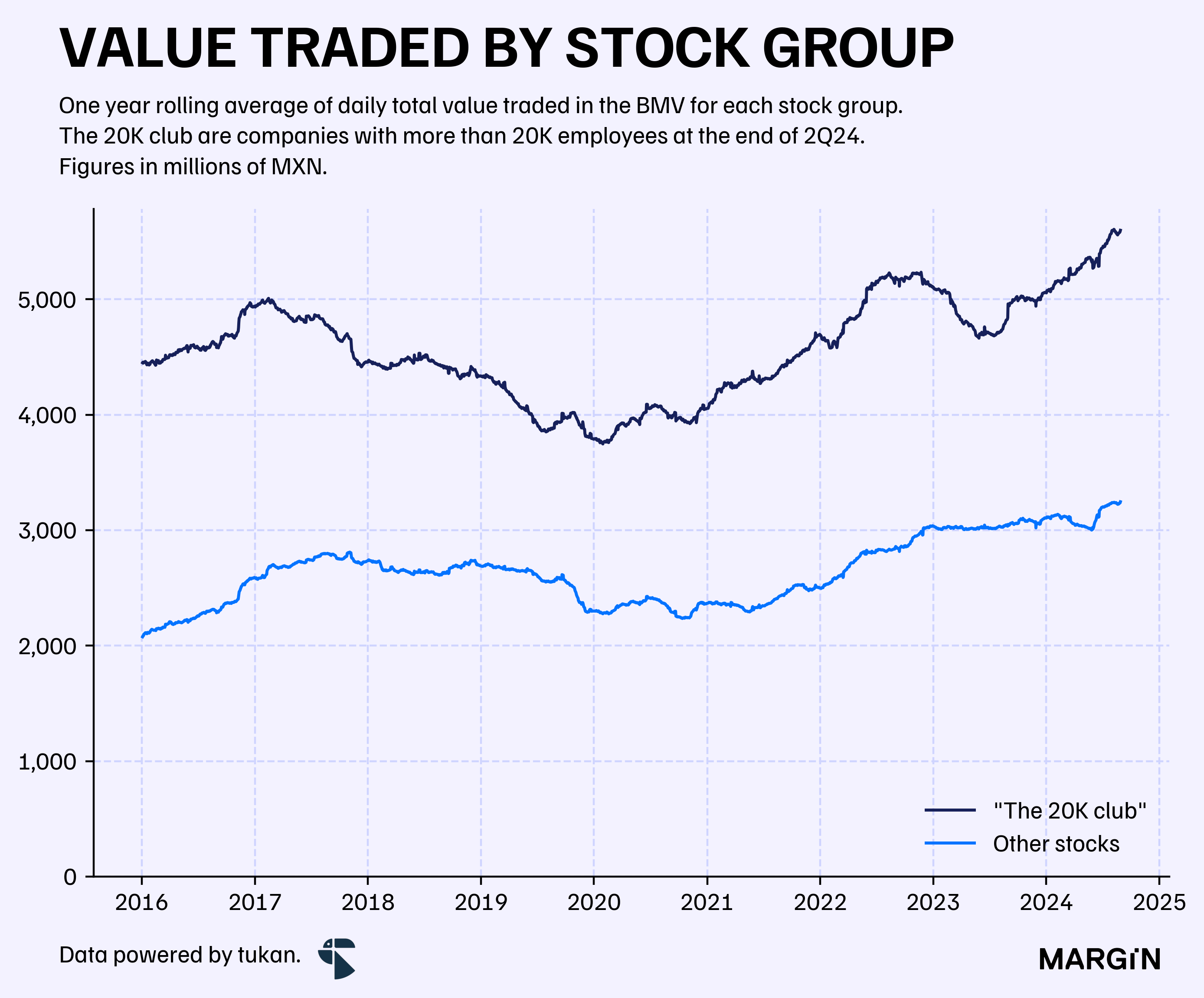

Based solely on trading data from the BMV, we can see that the aggregate of these stocks averaged a trading volume 72% higher than the rest of the market as of 2024. During 2016 the difference was more than double.

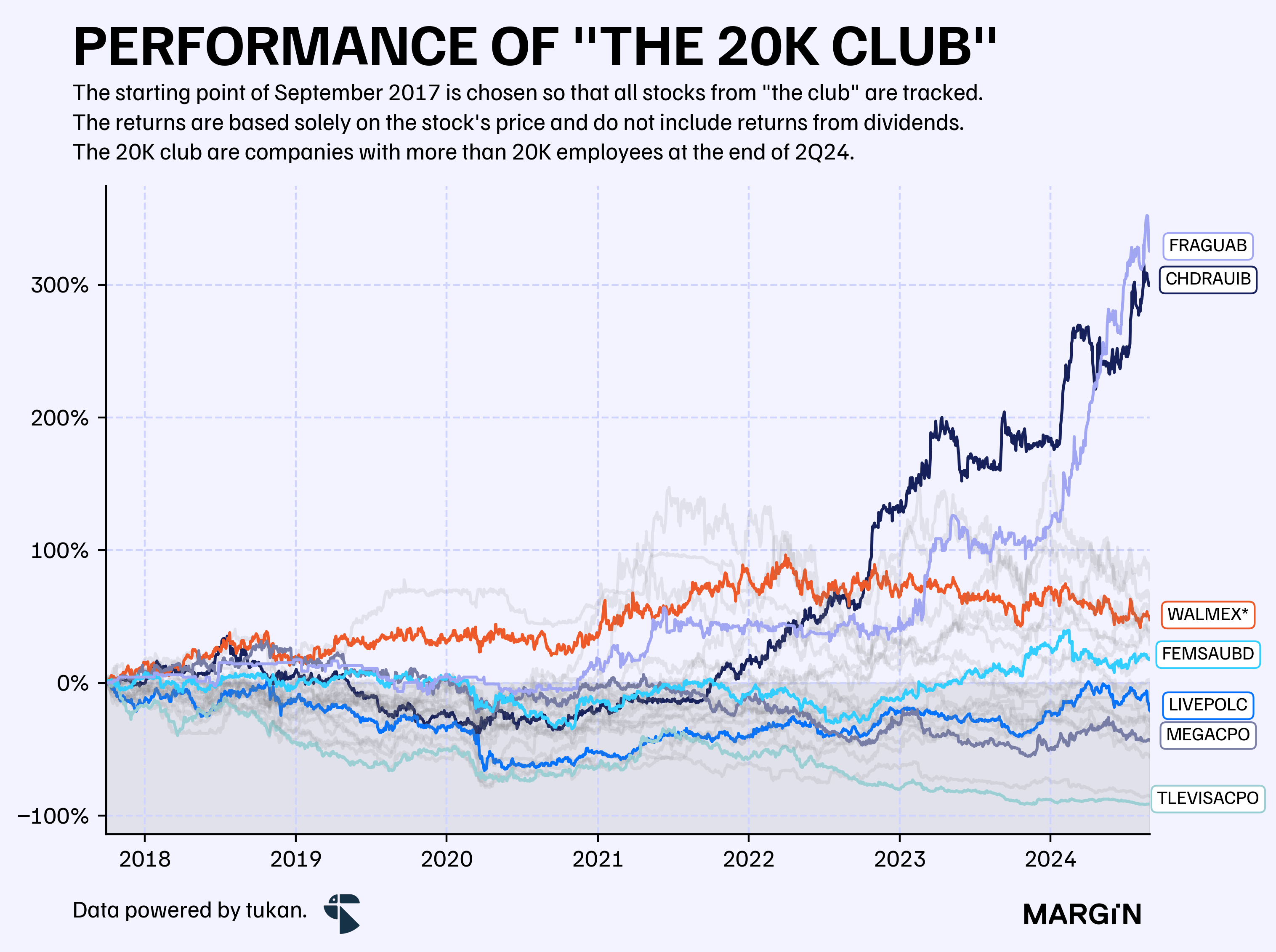

Since the end of September 2017, the Mexican IPC has remained practically flat, with less than a 5% return for the country’s main index. Out of the 25 companies that employed over 20 thousand people at the end of June, half outperformed the flagship index. Consequently, almost all of the underperformers (vs. the IPC) registered negative returns on their stock prices.

On the other hand, only two companies, Chedraui and Fragua (Farmacias Guadalajara), saw their stock prices quadruple during the same time frame.

Foreword

Our goal with Margin is to create a newsletter that provides weekly, differentiated, data-driven insights on what’s happening across the Latin American economic and business landscape.

As we continue to build this newsletter, we would love to hear your thoughts and feedback on our content. If there’s any industry or topic in particular that you would like us to explore, please let us know.

Feel free to reach out to me at miguel@tukanmx.com or leave a comment below with your thoughts and feedback.

Thank you for reading!