Ties

Exploring Mexico's investment and trade relationship with the US.

With Donald Trump’s return to the presidency, a shift in the country’s foreign economic policy is anticipated. Aside from the continued threats of tariffs targeting the Mexican and Canadian governments, we expect our northern neighbors to adopt greater protectionist measures and reduce their dependency on foreign goods, particularly those from China.

Given the country’s massive influence on the global economy, we decided to examine the United States’ key trade and investment partners to provide context on Mexico’s economic relationship with its northern neighbor and the dependence of the U.S. on Mexico as an economic ally.

According to UNCTAD’s World Investment Report, the United States remains the largest source of foreign direct investment (FDI) globally. In 2023, U.S. companies invested over USD $360 billion abroad.

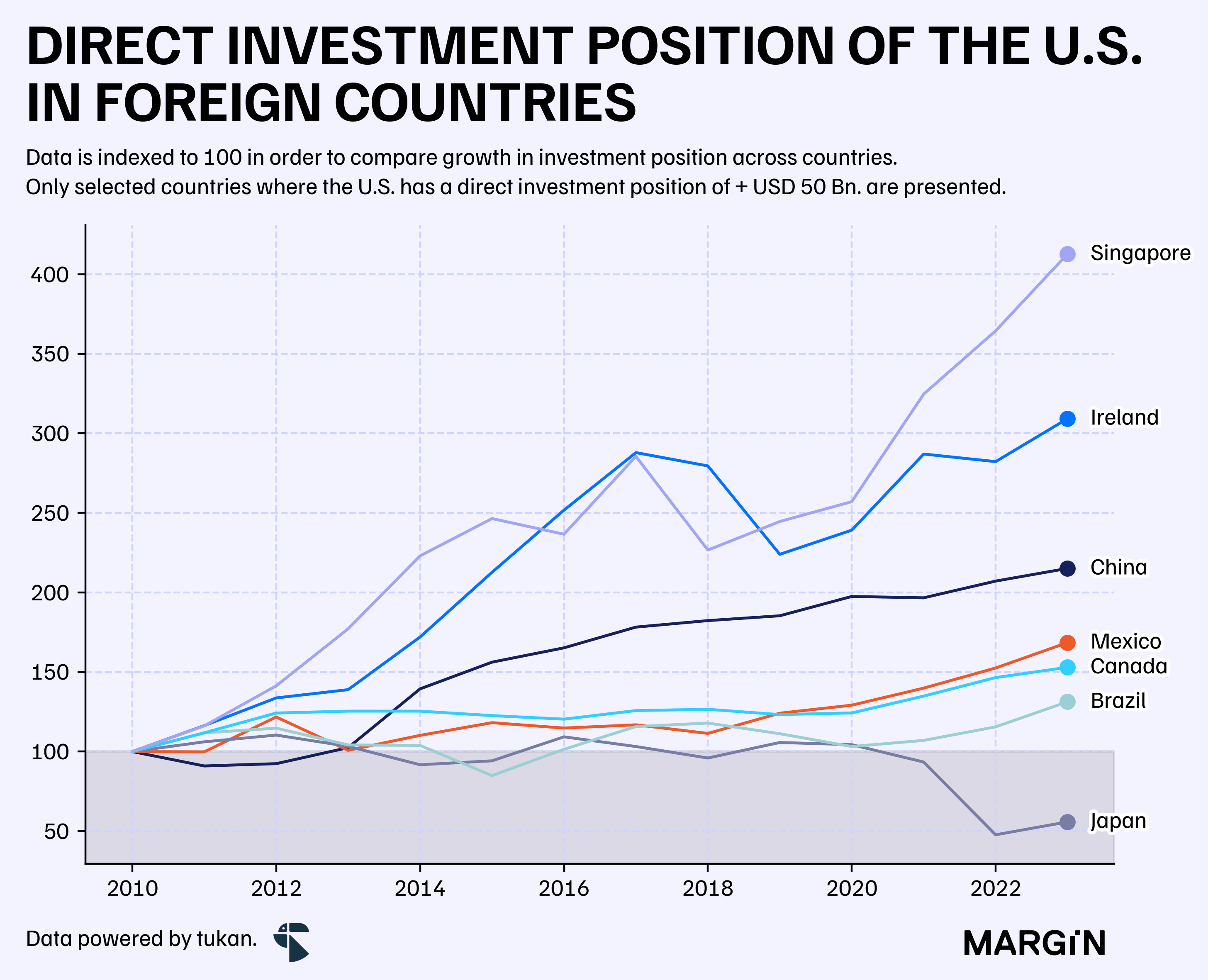

The top investment destinations last year were Singapore, the Netherlands, Bermuda, and Ireland, collectively accounting for over 40% of total FDI outflows. As of 2023, Mexico ranked as the 11th largest recipient of U.S. capital injections, a drop of two positions when compared to 2019.

Despite this decline in ranking, Mexico remains the top investment destination for U.S. businesses in Latin America, capturing 3% of total outflows during 2023.

Since 2010, the United States’ investment position in Mexico has grown at a compound annual growth rate (CAGR) of 4%, a pace consistent with broader market trends. However, in the past five years, investments in Mexico have accelerated compared to earlier periods. According to BEA data, the 5-year CAGR from 2018 to 2023 reached 8.6%, significantly outpacing the 2% growth observed between 2013 and 2018.

When comparing the growth in the investment position versus other countries, we can see Mexico being favored over our Canadian peers. But significantly lagging the pace of investments into Chinese markets.

However, what does the data tell us when we narrow it down to certain key industries such as manufacturing? And how much does the U.S. depend on imports from Mexico across key industries?

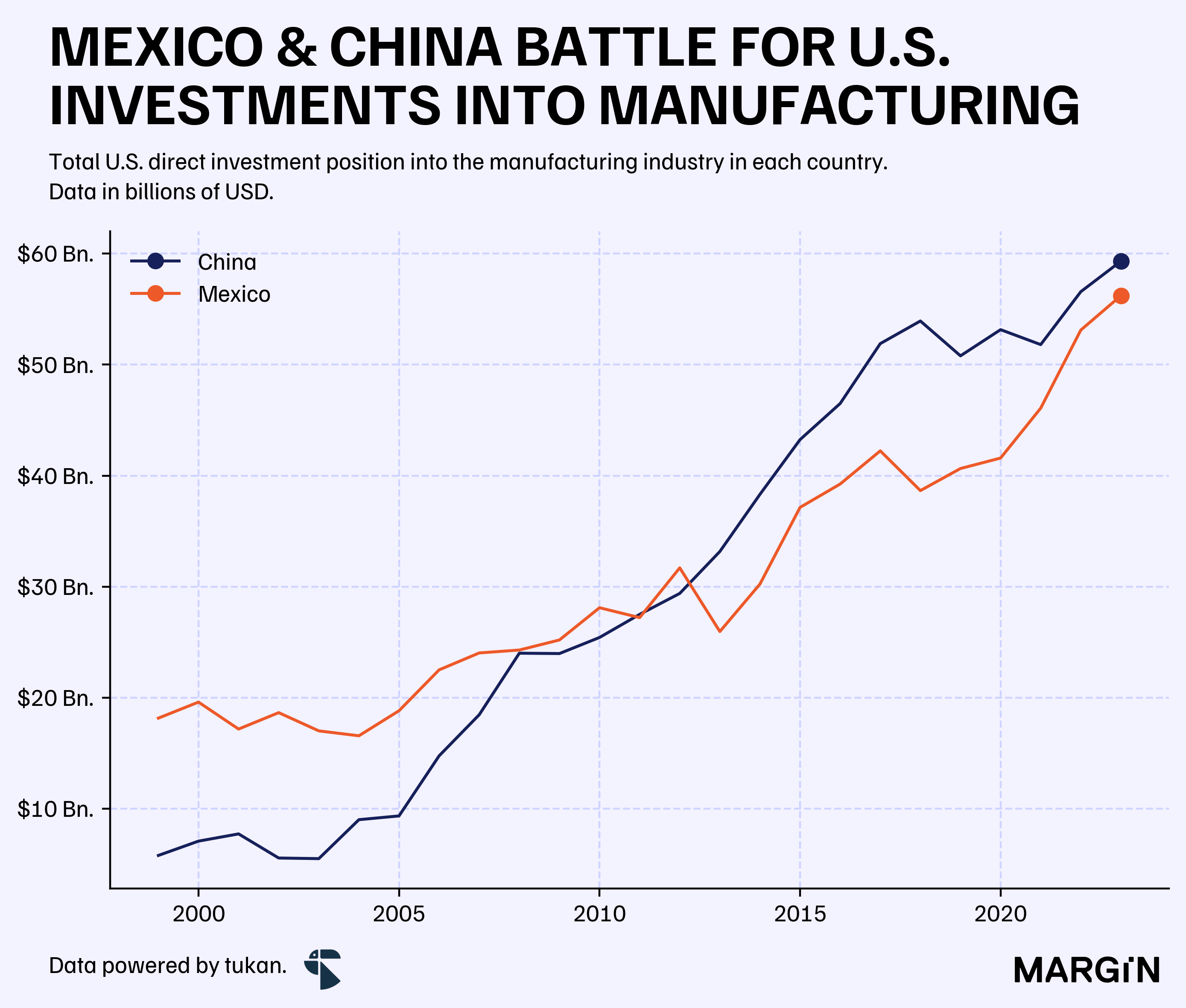

Based on data from the Bureau of Economic Analysis, the United States’ investment position in Mexico’s manufacturing sector accounted for 5% of the country's total investment in the space—a figure that has remained practically unchanged since the economic agency began publishing this data.

In contrast, investment positions in China’s manufacturing sector have gradually caught up to Mexico. Over the past 20 years, the share of American investments in Chinese manufacturing has risen from 1.5% in 2003 to over 5.9% as of 2023.

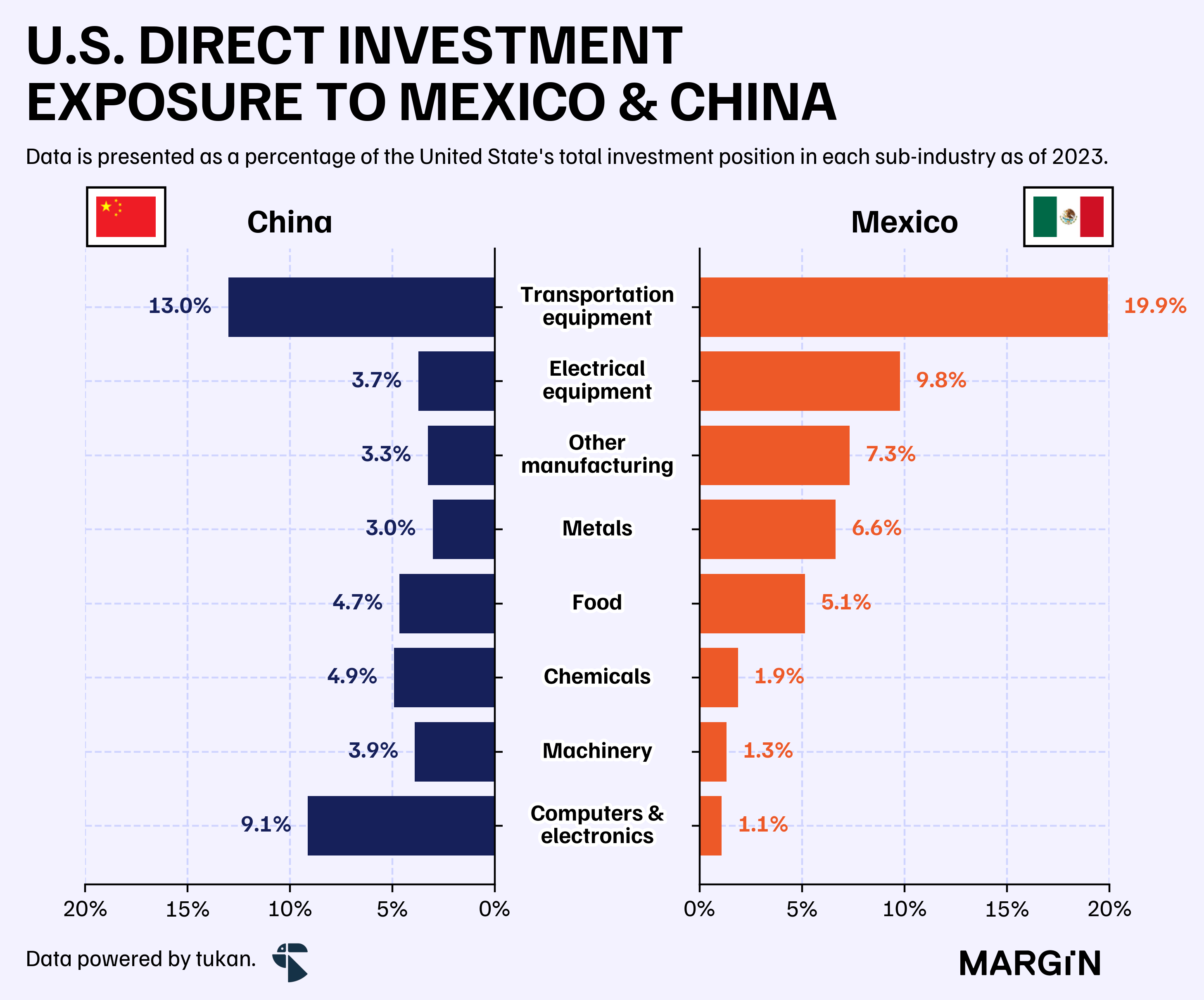

Despite China surpassing Mexico in 2013, the Latin American country has been gradually regaining ground and now holds an impressive “share of wallet” from U.S. investments in key industries such as transportation equipment, electrical equipment, and food manufacturing.

As of 2023, Mexico surpassed China in terms of total U.S. investment position across most manufacturing subindustries.

However, China still commands significantly more American capital in computer and related manufacturing—an industry that accounts for over 19% of total U.S. direct investment in manufacturing.

This is particularly interesting when considering Mexico’s significance as a source of imports across these categories.

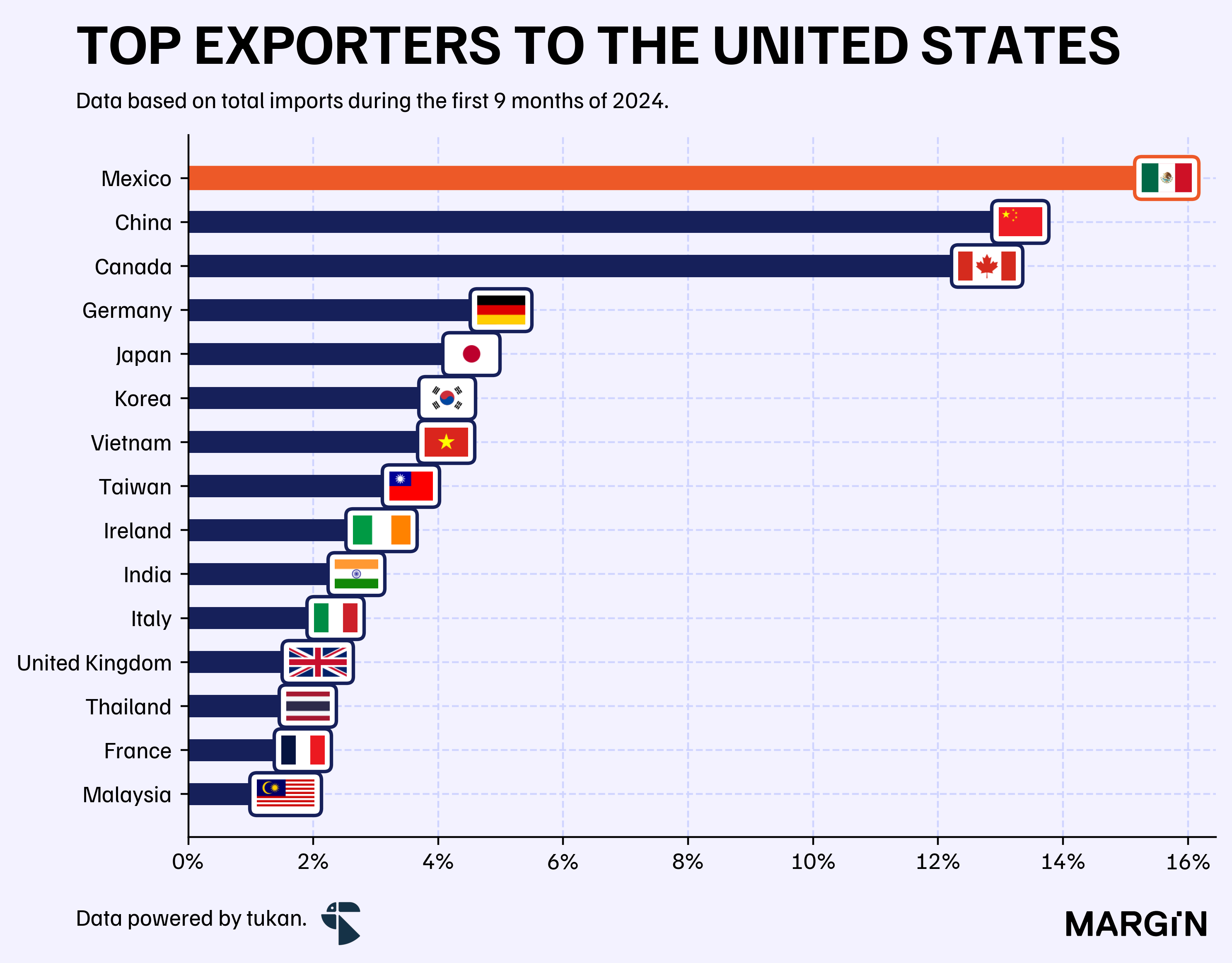

As you may know, Mexico recently surpassed China as the top supplier of goods to the United States, boasting a total import share of 15.6% as of 3Q24—2.3 percentage points higher than its Chinese counterpart.

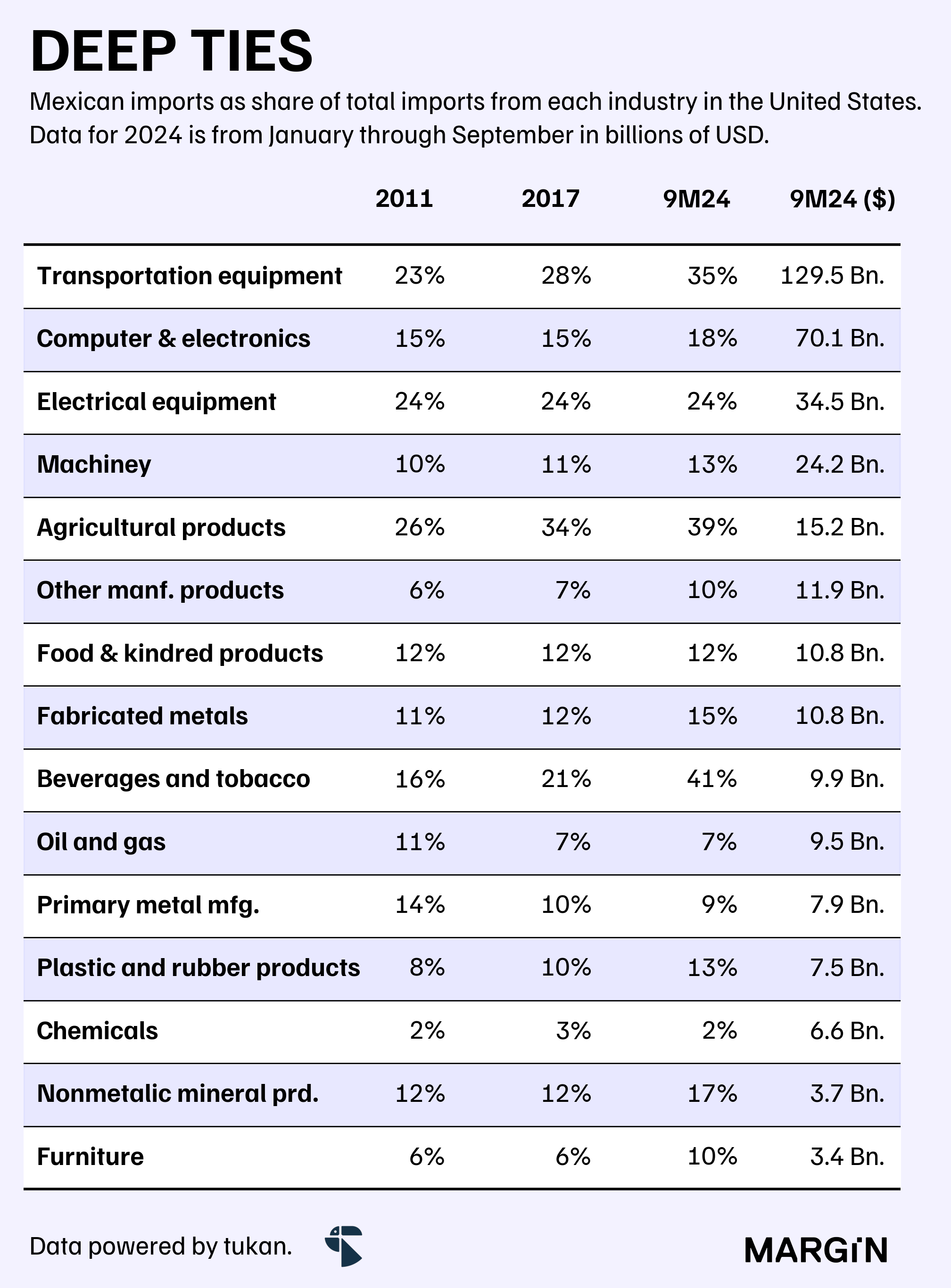

However, what stands out most from the U.S. Census data are Mexico’s import share figures across key categories. For instance, as of 3Q24, Mexico accounted for over 35% of U.S. imports in the transportation equipment sector and more than 40% in agricultural, beverage, and tobacco products. Meanwhile, electrical equipment imports from Mexico represented 24% of the total, a strong foothold in a highly competitive space.

The previous table not only underscores Mexico’s growing importance as the United States’ main trading partner but also highlights the substantial shifts and deepening interdependence between these neighboring economies over recent decades.

Beverages and tobacco offer a compelling example. Imports from Mexico in this category have nearly reached USD $10 billion in the first three quarters of this year alone, driving the U.S.’s exposure to these goods from 16% to over 40% in just 13 years.

We believe Mexico has managed to build a considerable moat across key categories when it comes to the goods it’s been sending up north. Plus, as we mentioned earlier, U.S. corporations have steadily increased their stake in the country, with many having spent years setting up shop here.

Despite Trump’s confrontational rhetoric and potential threats, it seems Mexico might still have a few automóviles, camiones, cervezas, and aguacates up its sleeve.