Trading Places

Unveiling the geographic transformation of Mexico’s economic growth.

Mexican economic output has historically been driven by four key states: Mexico City (15% of total GDP), State of Mexico (9%), Nuevo León (8%), and Jalisco (7%). However, data suggests that the country could be set for important shifts in the geographic composition of its economic development.

In today’s post, we present key insights across three topics that we consider could influence the economic landscape of the country from a geographic standpoint in the years to come.

Executive summary

Every single state that makes up “el Bajío” has increased its share on the country’s total economic output. Between 2003 and 2022, the region reported a CAGR on its real-GDP of above 2.3% — 91 basis points above the rest of the Mexican economy, and contributed close to 34% of the country’s economic growth in the past ten years; despite accounting for just 22% of total GDP during the same period (on average).

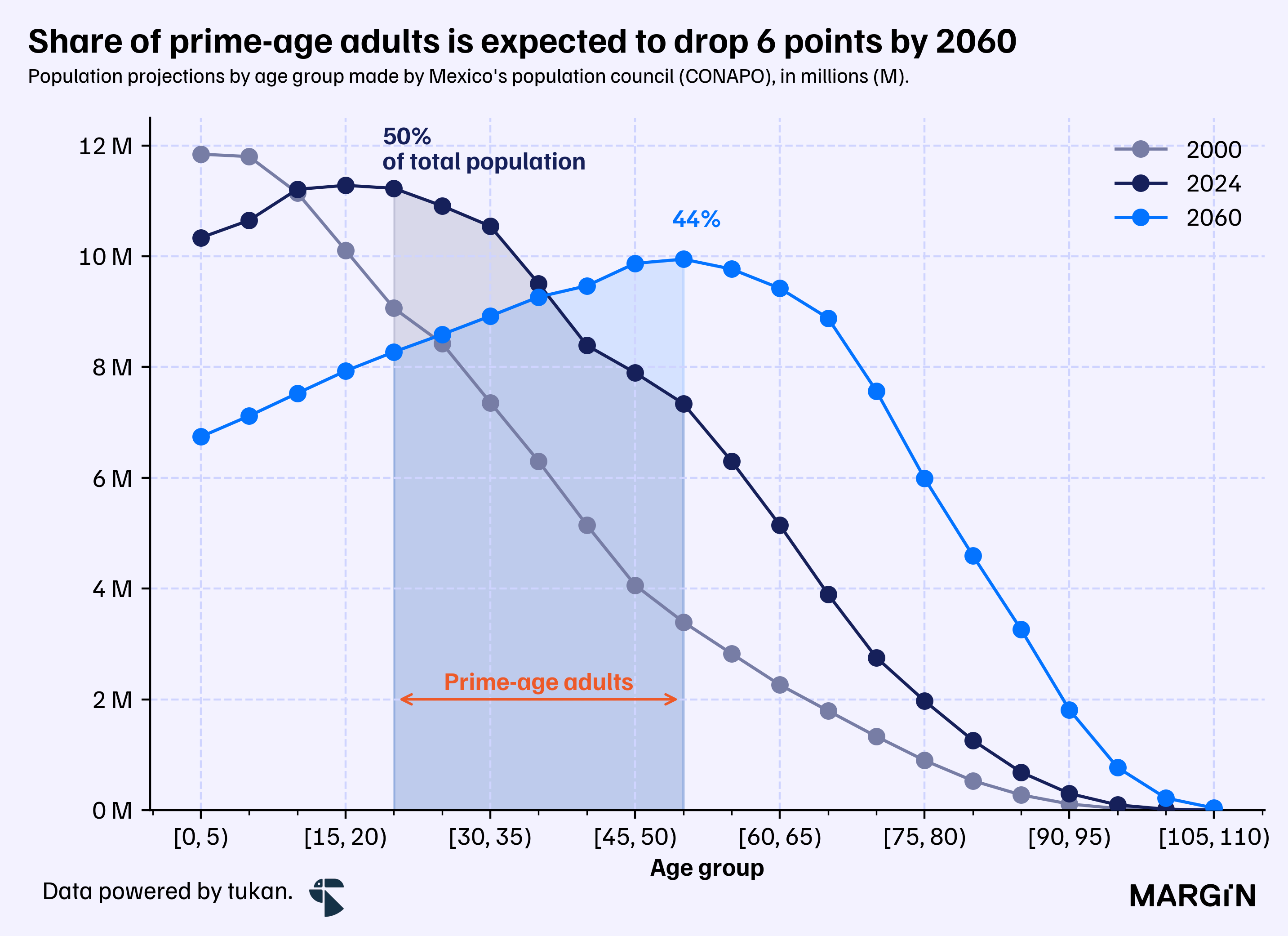

Demographics may play a key role on labor supply. According to CONAPO, Mexico (as a whole) is set to face serious consequences on the aging of it’s population — per the institution’s projections, only 44% of the country’s total population will be considered prime-age working adults1 by the end of 2060 (vs. 50% as of “today”). This could result in increased economic development for states and regions where the share of prime-age adults considerably surpasses the country’s average, such as: Baja California Sur, Quintana Roo and Querétaro.

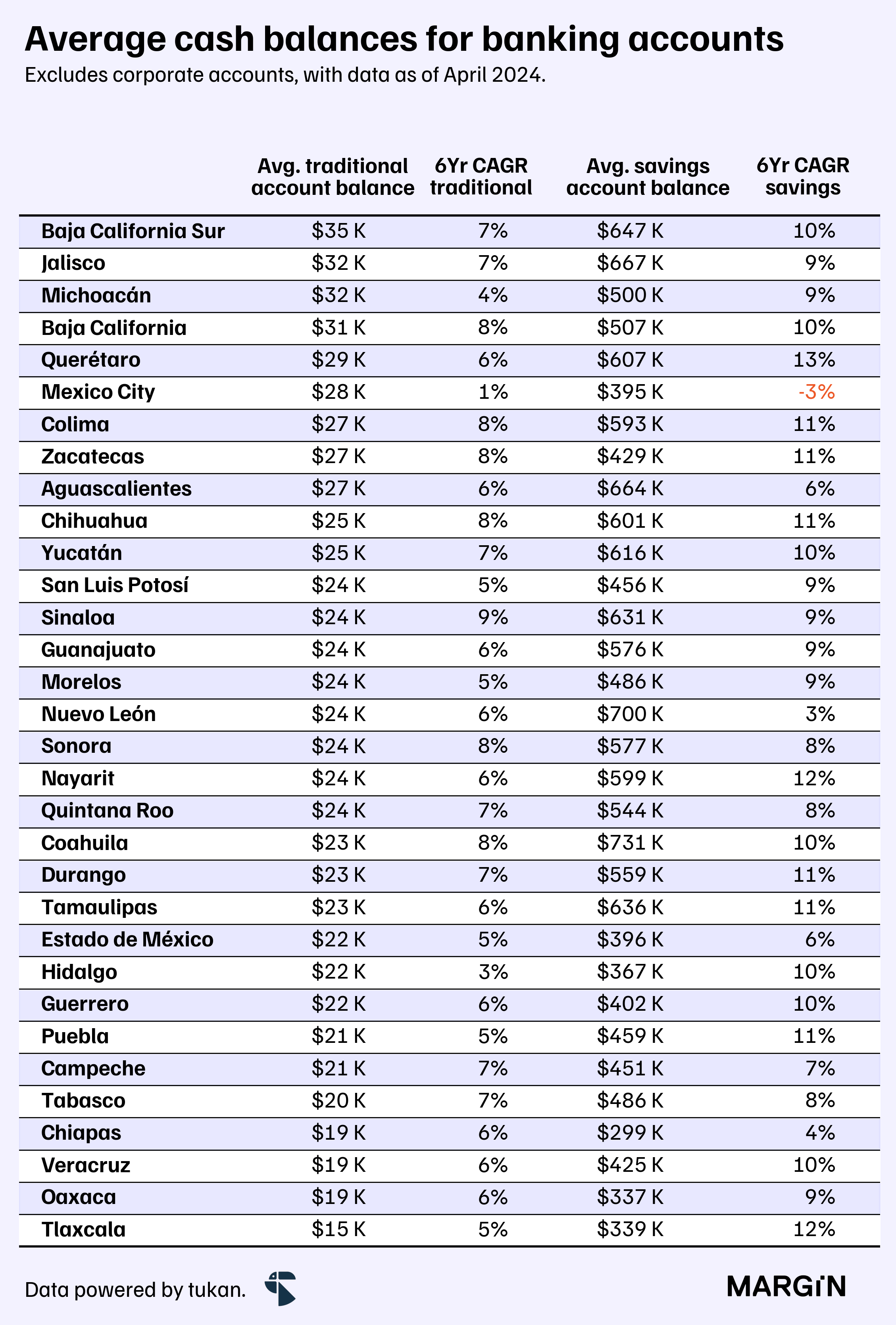

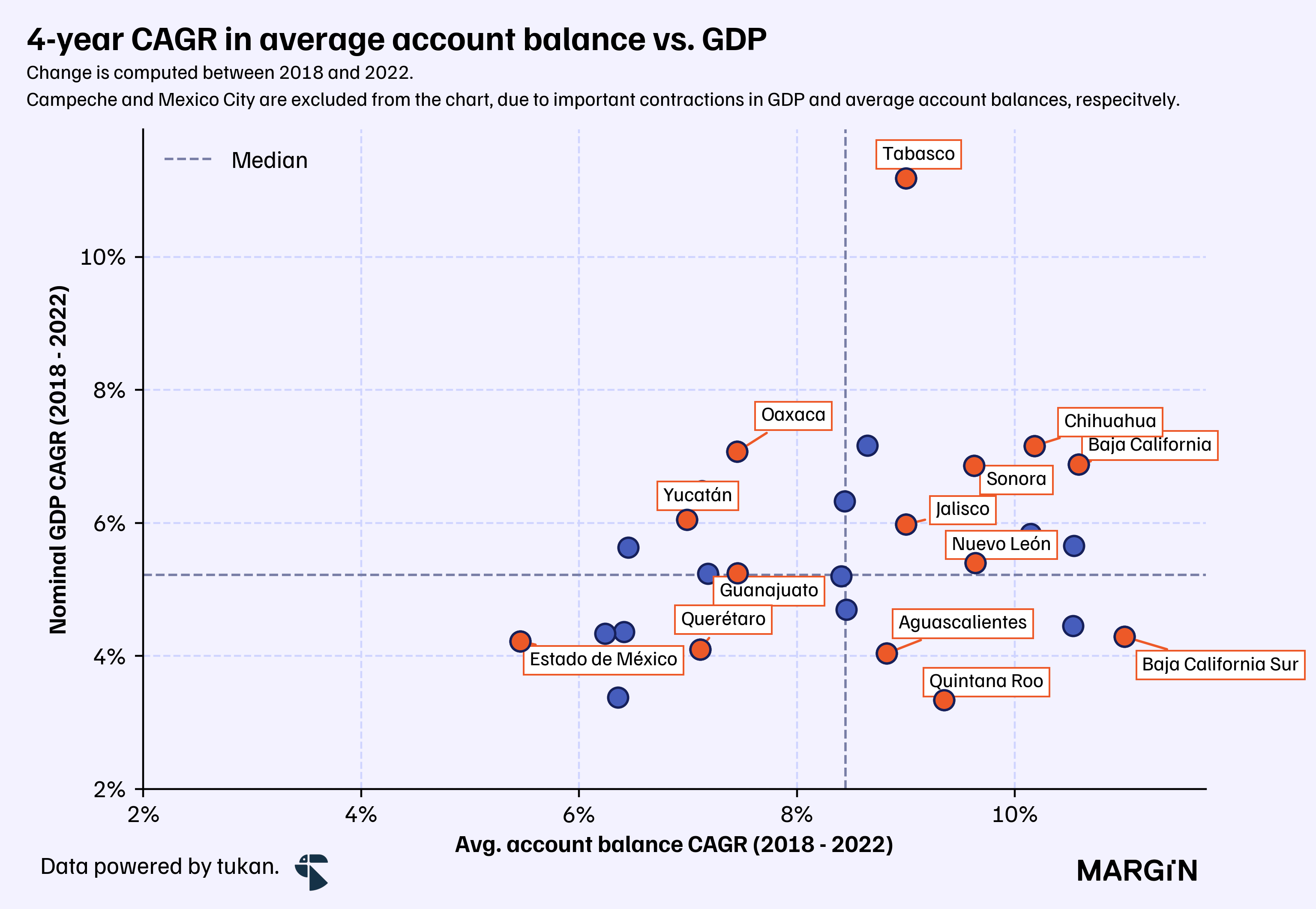

Change in average cash balances per banking account could be a proxy for growth. Based on CNBV data, the average banking account in Mexico (excluding corporates) had an average balance of MXN $24 thousand as of April 2024, implying a 6-year CAGR of 4% (a rate close to the country’s average inflation). Out of the 16 states with an above median CAGR on their average cash balances, only 5 recorded an economic growth below the country’s median.

The rise of “the Bajío” region

According to INEGI’s data, the seven states that make up “the Bajío” region increased their share in the country’s total economic output to 22% by the end of 2022, up from 19% in 2003.

The Bajío region is made up from: Aguascalientes, Guanajuato, Jalisco, Michoacán, Querétaro, San Luis Potosí, and Zacatecas.

However, the economic success of central Mexico is not limited to its increased influence on the country’s GDP. For instance, prior to 2019, labor productivity in the region significantly lagged behind the rest of the country across key industries. This gap has not only been closed in recent years, but the region now surpasses the average productivity indices reported by the remaining states, according to the latest INEGI data.

On top of the premium and rise in productivity within the region, “el Bajío” also boasts competitive labor force costs in manufacturing when compared to other states — with weighted-average salary per hour in the industry being estimated at about 3% lower than the national average.

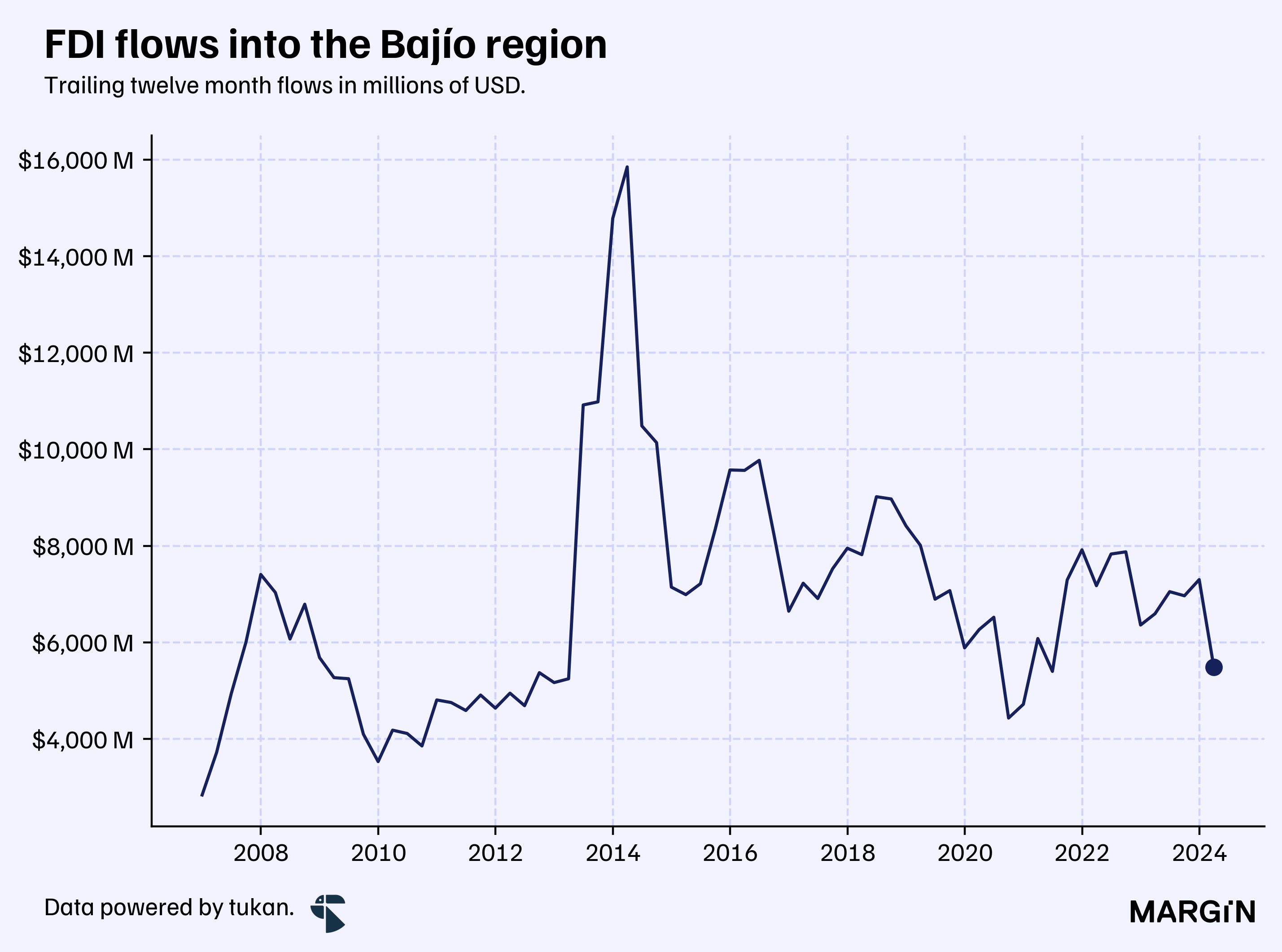

Despite these attractive figures, recent FDI into the region has not been as high as one might have hoped. According to data from the Secretaría de Economía, foreign investment flows into the region reached USD $7.3 billion in 2023 (+15% YoY) — a figure well below the levels observed prior to the pandemic.

Even though the region registered lackluster FDI (as a whole) during 2023, the states of Aguascalientes and Querétaro posted good results — with both of them closing the previous year close to record highs.

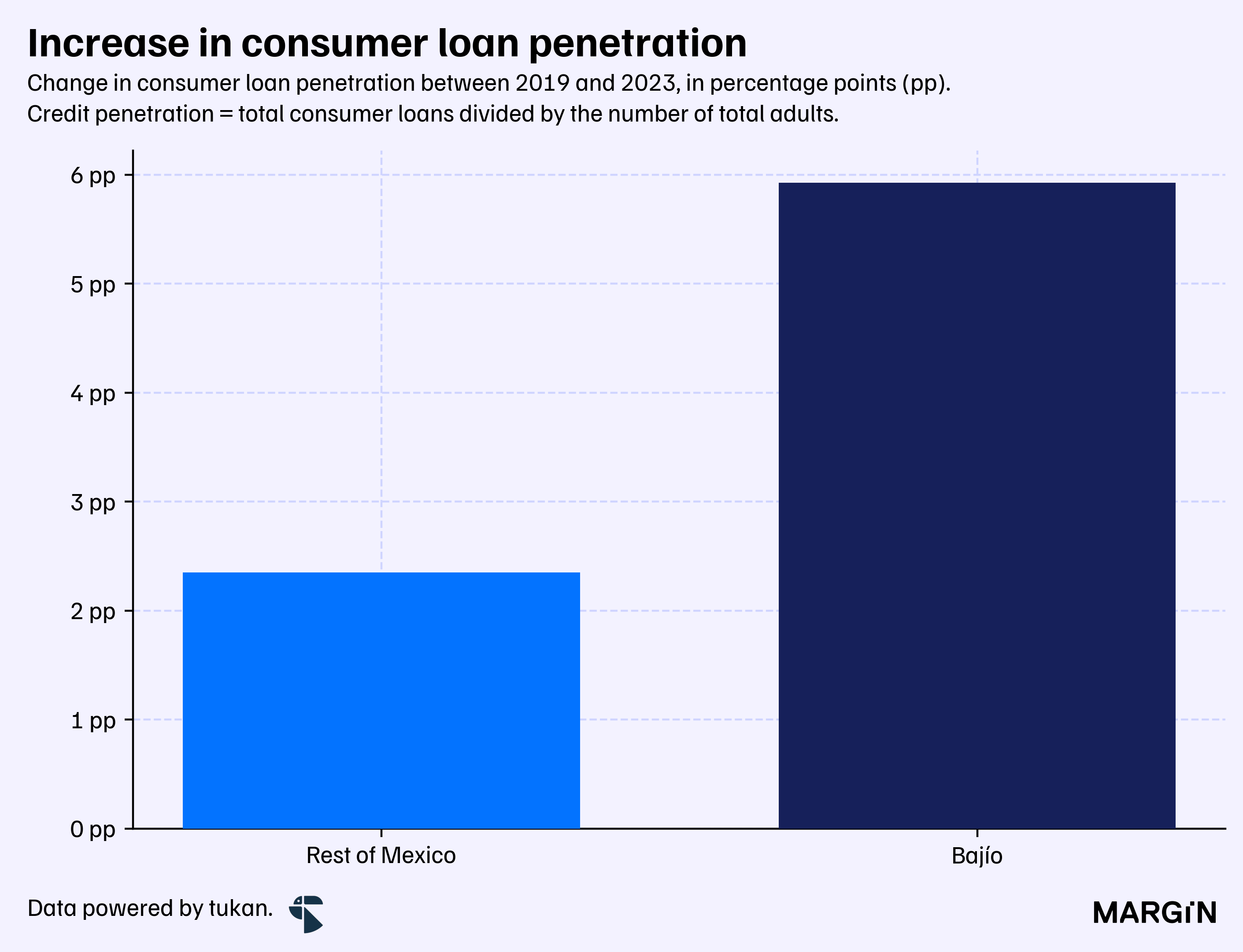

On the other hand, lower informality rates and increased credit penetration highlight the economic development of the region. Notably, only two of the seven states (Michoacán and Zacatecas) posted higher labor informality rates than the national average.

With a lower share of informal workforce, credit penetration has increased, raising the number of consumer loans from commercial banks to 65 per one hundred adults by the end of 2023, up from 59 at the end of 2019.

During the past four years, the total number of consumer loans from commercial banks increased by 17% (vs. +9% for the rest of the country) to close the year 2023 at over 12.7 million loan contracts within the region.

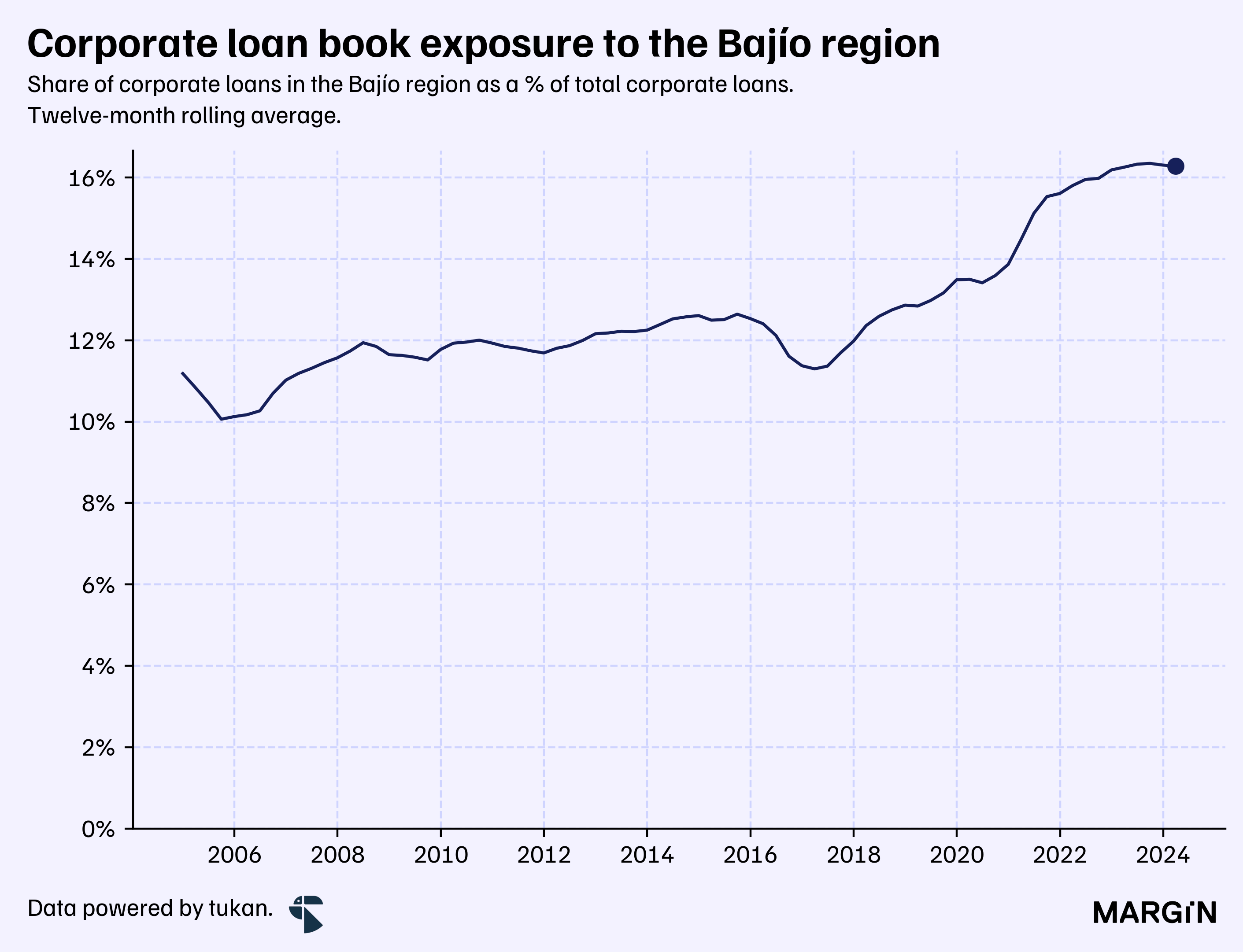

On top of this, Mexican bank’s corporate loan books had never been as exposed to “el Bajío” as they have been in recent quarters, at 16% of the total loan book.

Follow the young

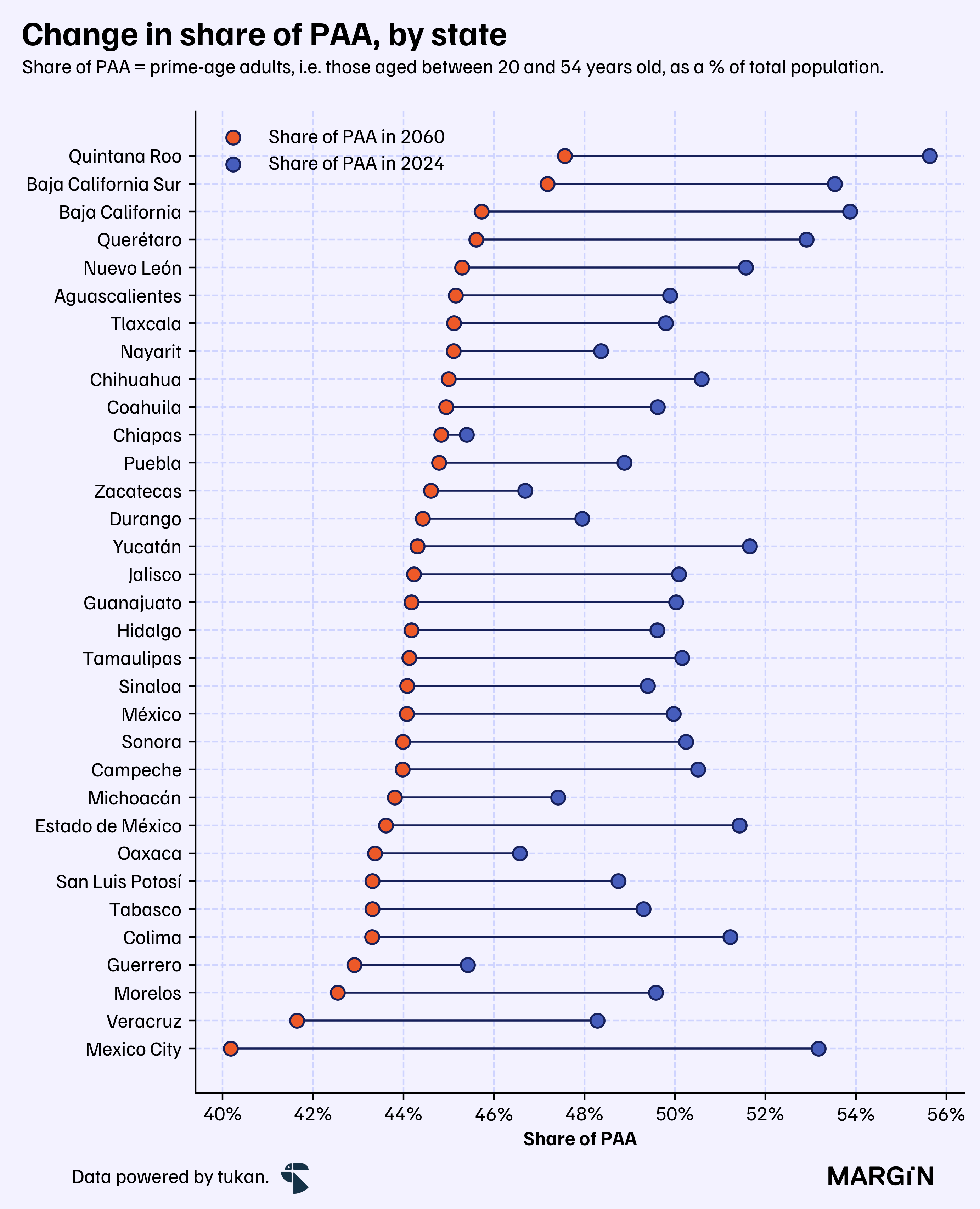

According to projections by the Mexican population council (CONAPO), prime-age adults as a percentage of the total population peaked at a staggering 50% in 2024. However, this rate is expected to decline to around 44% by 2060 — 6 percentage points below current levels and similar to those observed in the year 2000, but with a much lower share of children and young adults.

According to INEGI and CONAPO, GDP per prime-age adult (PAA) closed at around MXN $456 K in 2022 — 55% higher than in 2012, but 2% lower when adjusted for inflation.

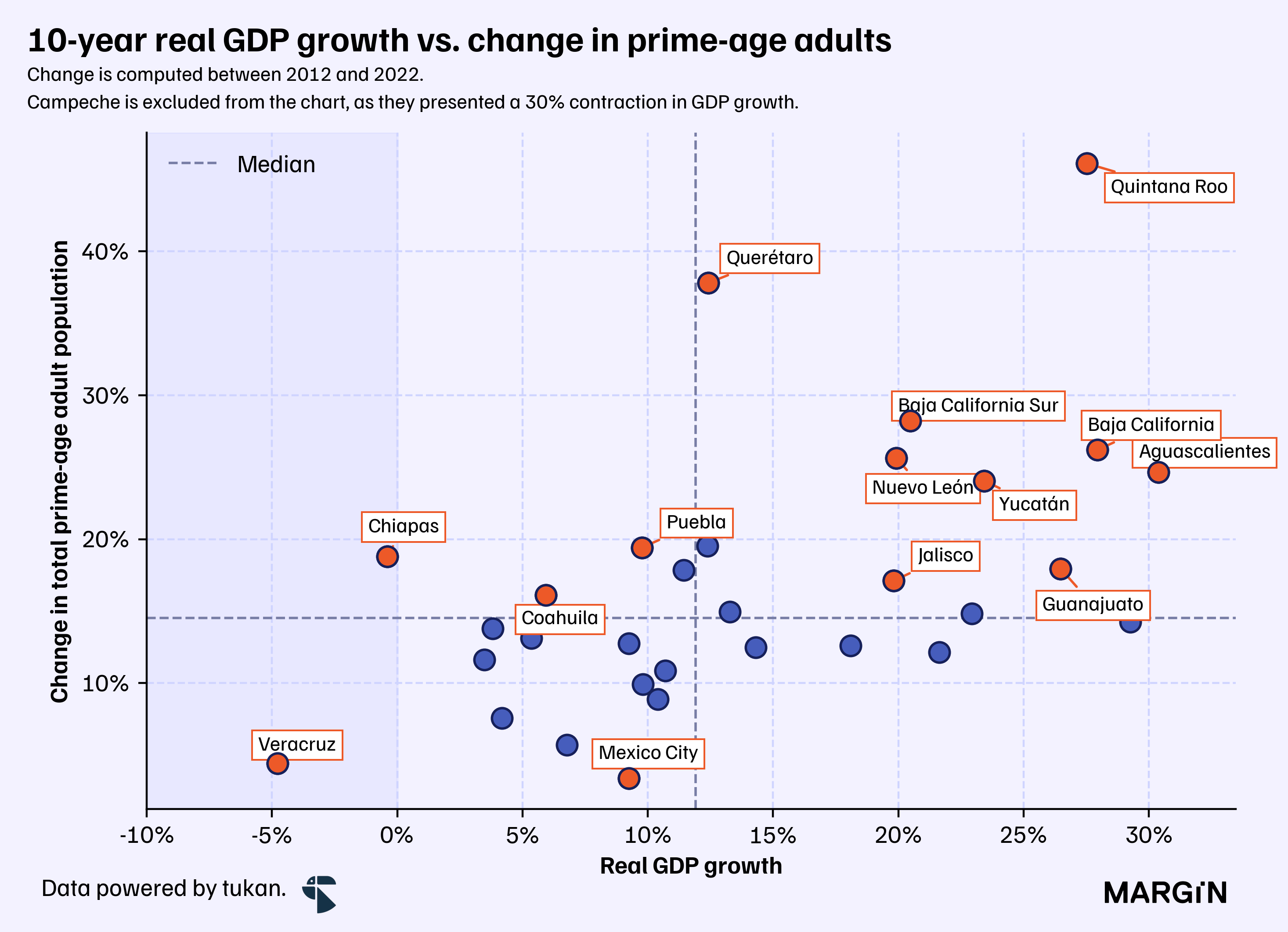

When examining each state individually, a relationship appears between real GDP growth and the growth of the prime-age adult population. Quintana Roo stands out as a notable example; the southern state saw its prime-age adult population increase by more than 40% and experienced real GDP growth of over 25% from 2012 to 2022.

Out of the 16 states that reported prime-age adult (PAA) growth above the national median, only four states — Tlaxcala, Puebla, Chiapas, and Coahuila — reported sub-par economic growth during the same period, i.e., below the median.

As PAA share in the total population is set to decline by about 6 points in the following 36 years, we explore which regions of the country are expected to report the least impactful changes on the young adult population.

The Mexican capital — which is responsible of around 15% of the country’s GDP, is expected to go from a PAA share of 53% to close to 40% in 2060.

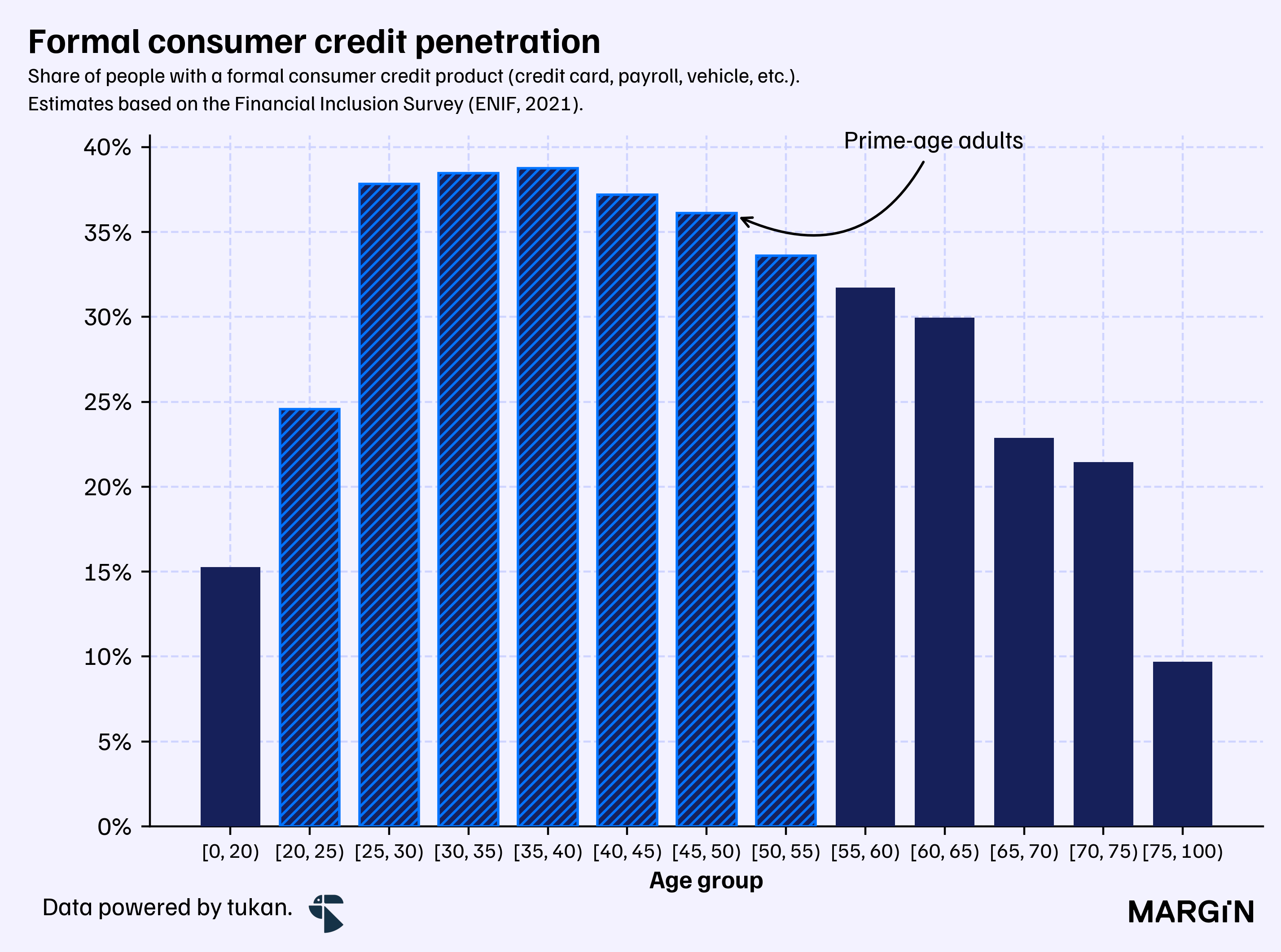

Besides impacting the labor force supply, the aging of the country’s population could also significantly affect consumer credit and spending. Estimates from INEGI’s Financial Inclusion Survey (ENIF, 2021) show that credit penetration hovered around 35% for adults aged between 20 and 54, compared to 22% for the rest of the adult population.

Cash in the bank

According to CNBV data, the average banking account (excluding corporates) in Mexico closed the month of April with a balance of around MXN $24 K — a figure that remained flat YoY.

Time deposit (or savings) accounts, on the other hand, recorded an average balance of MXN $560 K (+20% YoY).

Note however, that these last figures could be heavily skewed by accounts with large balances — i.e. the average balance of two accounts, one with $1 million, and the other with zero funds is $500 K.

As banking penetration continues to rise in the country, increase in average cash balances could shed light on those regions where there’s also been a rise in economic development. Out of the 16 states with an above median CAGR on their average cash balances, only 5 recorded an economic growth below the country’s median.

All in all, it’s hard to pinpoint exactly where the next economic hub will develop in the country, although the Bajío and Northern regions are making a strong case for themselves.

However, the deterioration in key performance indicators (KPIs) associated with economic growth for two of the country’s key states—Mexico City and the State of Mexico—combined with an aging population at rates considerably higher than the national average, opens up interesting opportunities for other states to increase their share and influence in the overall Mexican economy.

Adults aged between 20 and 54 years old.