Under the Radar

A look at banking accessibility within Mexico's informal economy.

Mexico’s informality rate closed July of this year at 54.5% — a figure 120 basis points lower than the previous year.

Despite efforts to reduce informality in the country, we found that a staggering 762 municipalities in Mexico still had over 90% of their total workforce employed in the informal economy in 2023. Out of these, 183 had a total population of over 10,000 people.

In total, these 762 municipalities are home to close to 6 million people; the majority of them concentrated across the states of Oaxaca, Chiapas and Guerrero.

Interestingly, the number of regions almost fully dependent on the informal economy haven’t changed much over the past seven years. According to INEGI estimates, in 2017 there were 774 municipalities with informality rates surpassing 90%; just 12 more than the current figures.

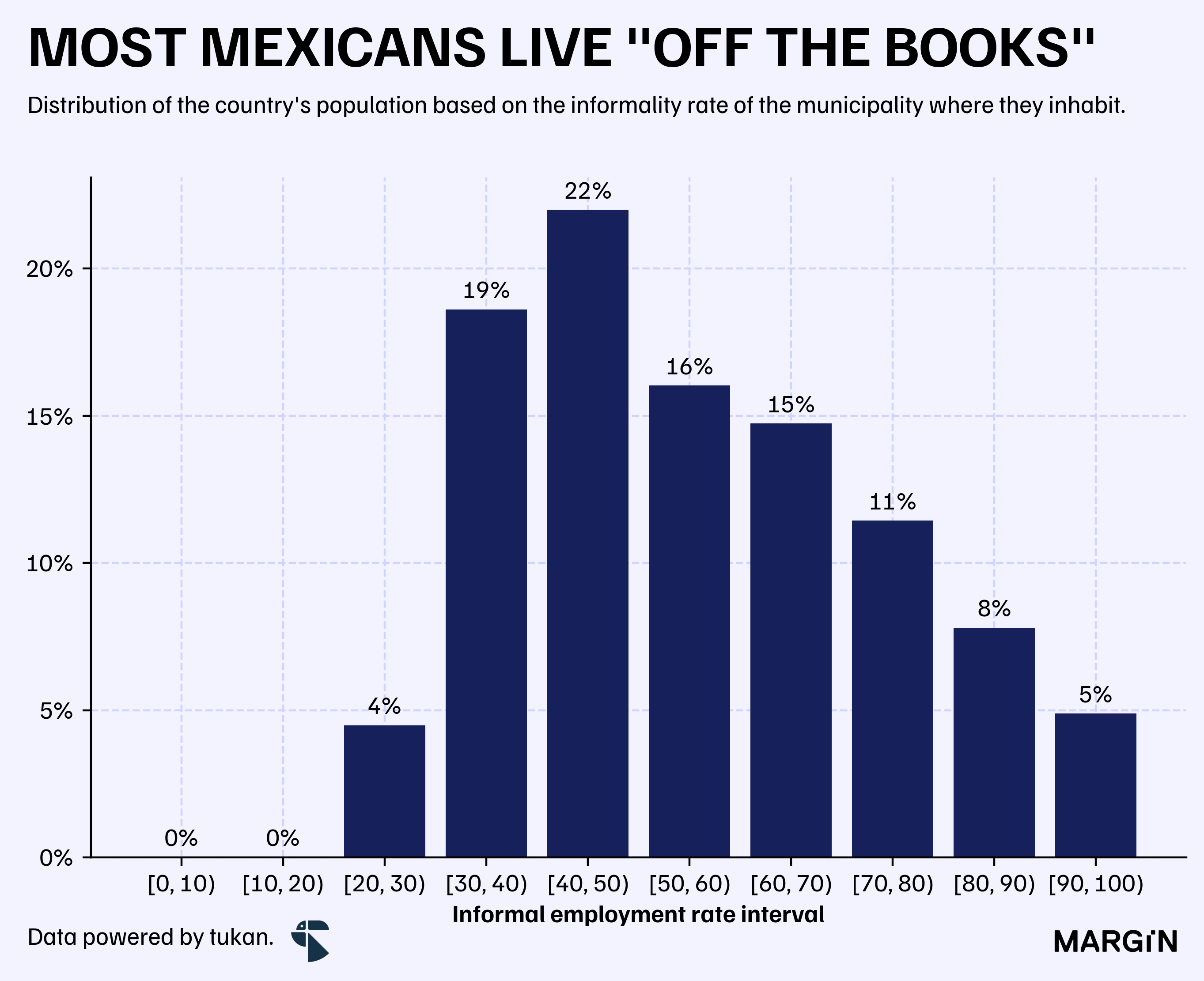

As of the latest estimates, we found that there isn’t a single municipality in the country with an informality rate below 20%.

Despite most of the population living in regions where the off-the-books economy hovers close to the national average of 50%, close to 23% of the population resides in areas where the informality rate exceeds 70%.

How does this relate to banking accessibility and financial inclusion?

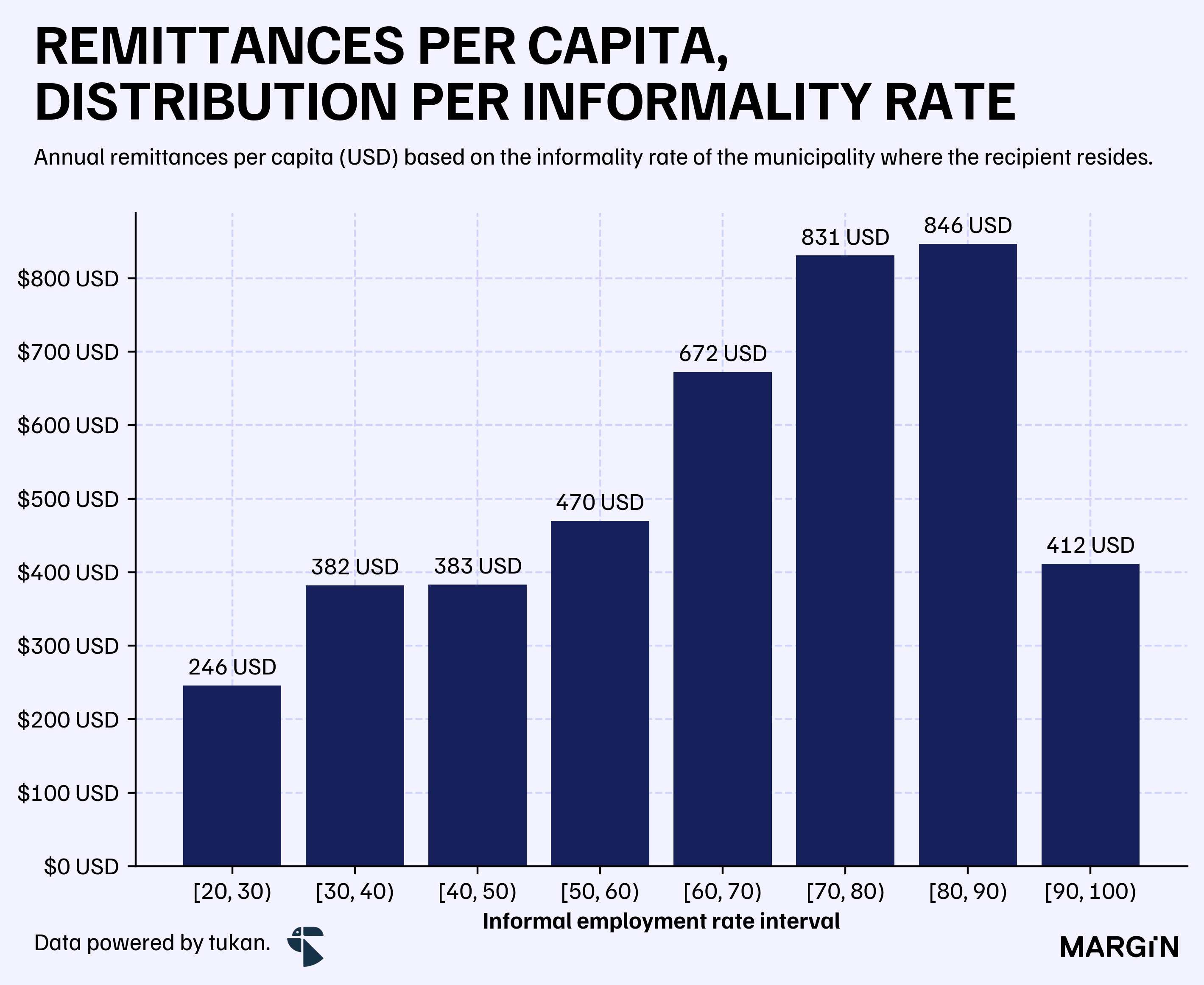

According to Banxico data, remittance inflows per capita were 43% higher for municipalities with +70% informality rates than the national average. This translated into an impressive total share of remittance inflows of over 35% for these areas, despite them only covering 23% of the country’s total population.

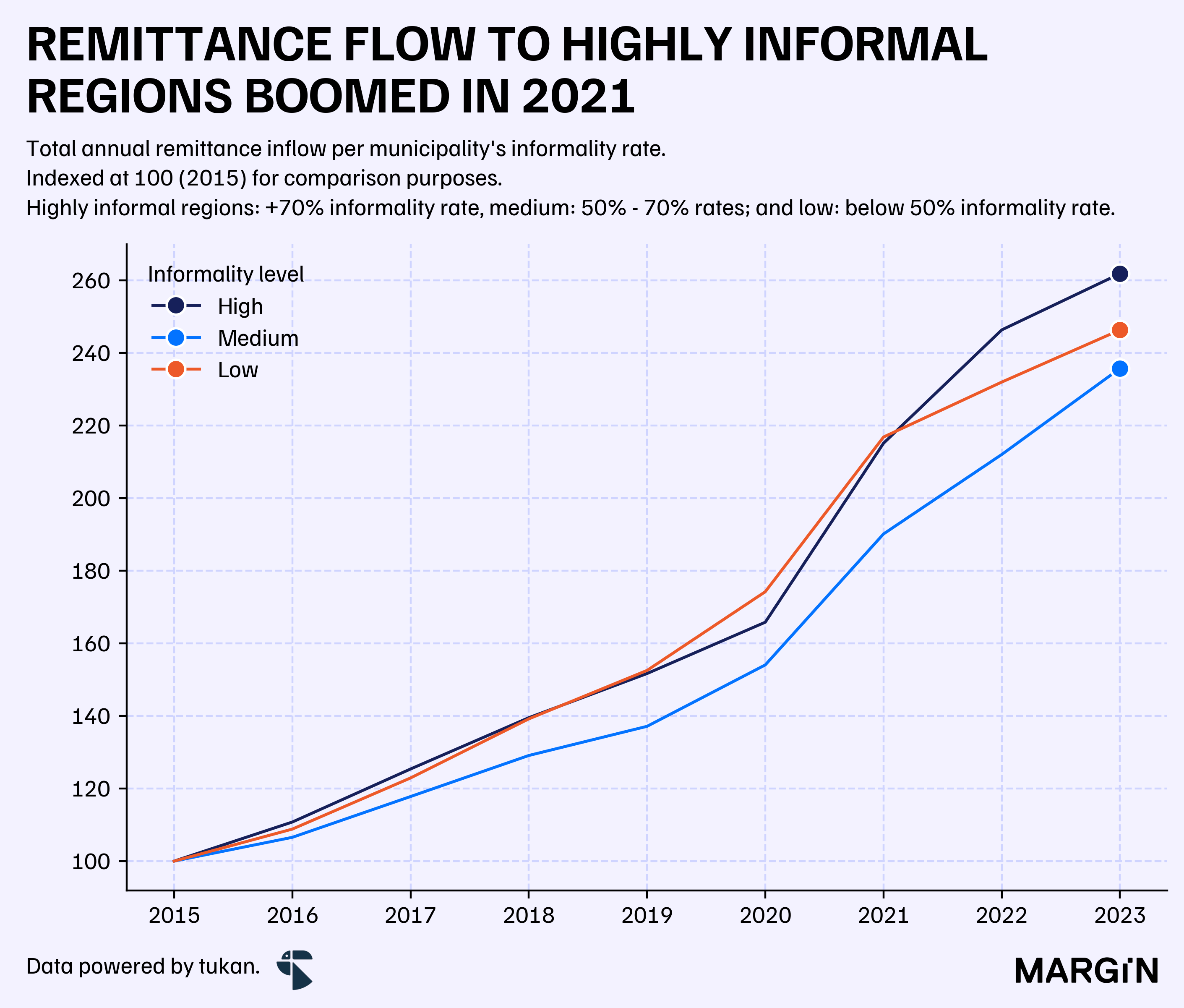

Not only do municipalities with higher informality rates experience a larger remittance inflow per capita than other parts of the country, but they’ve also been growing at an unprecedented pace. For example, high-informality regions (i.e., those with informality rates over 70%) have seen remittance flows increase at a 12.7% CAGR over the past eight years, whereas average-informality municipalities (i.e., those with rates between 50% and 70%) have grown at a CAGR of 11.3%. Low-informality regions, on the other hand, reported a CAGR of 11.9% during the same period.

Interestingly, most of the growth for highly informal regions occurred in 2021, when the total amount of USD sent to these Mexican families increased by 30% compared to the previous year.

For context, 23% of the population resides in highly informal regions; 31% in “medium” non-formal economy rates and the remaining 46% in municipalities with low informality.

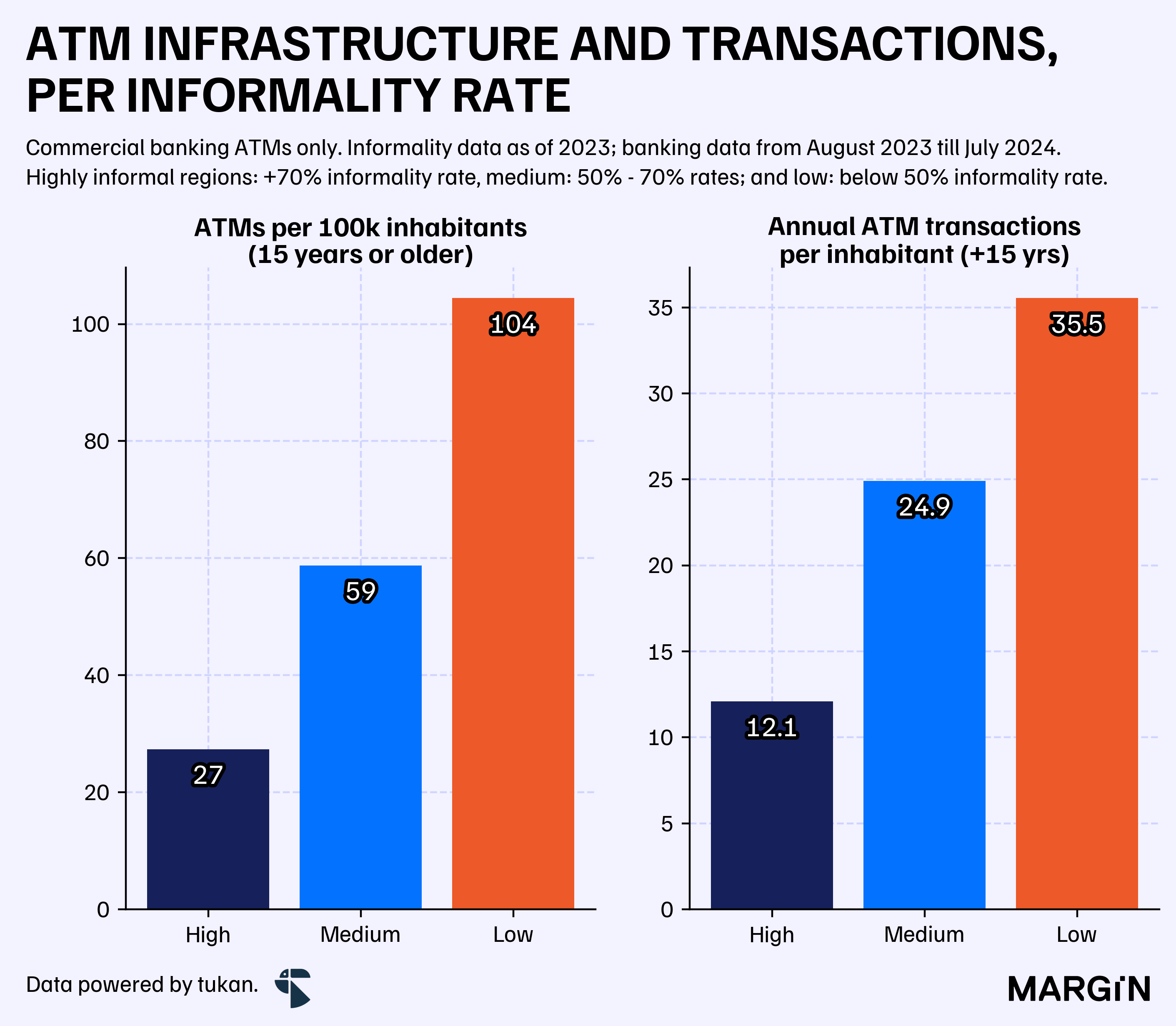

Although there’s no official data to fully support this, we believe that most transfers and financial transactions within predominantly informal areas likely occur outside of traditional banking channels. According to CNBV data, there were just 27 commercial bank ATMs per 100,000 people in these municipalities on aggregate, a figure 63% lower than the national average.1

As expected, this scarcity of ATMs could contribute to lower banking penetration within these regions. To illustrate this, take a look at the following chart, which shows that there were just 12 ATM transactions per capita per year in highly informal regions. Conversely, areas with low informality reported close to 36 transactions per inhabitant per year at their ATMs, equating to just under 3 visits per month.

Curiously, data from CNBV shows that despite these regions having much lower access to banking infrastructure and penetration, those involved in the financial system exhibit a much higher demand for cash than in other parts of the country. This is likely due to the cash-based nature of their local economy. Over the past 12 months, ATMs located in highly informal regions experienced 20% higher usage per ATM compared to other areas.

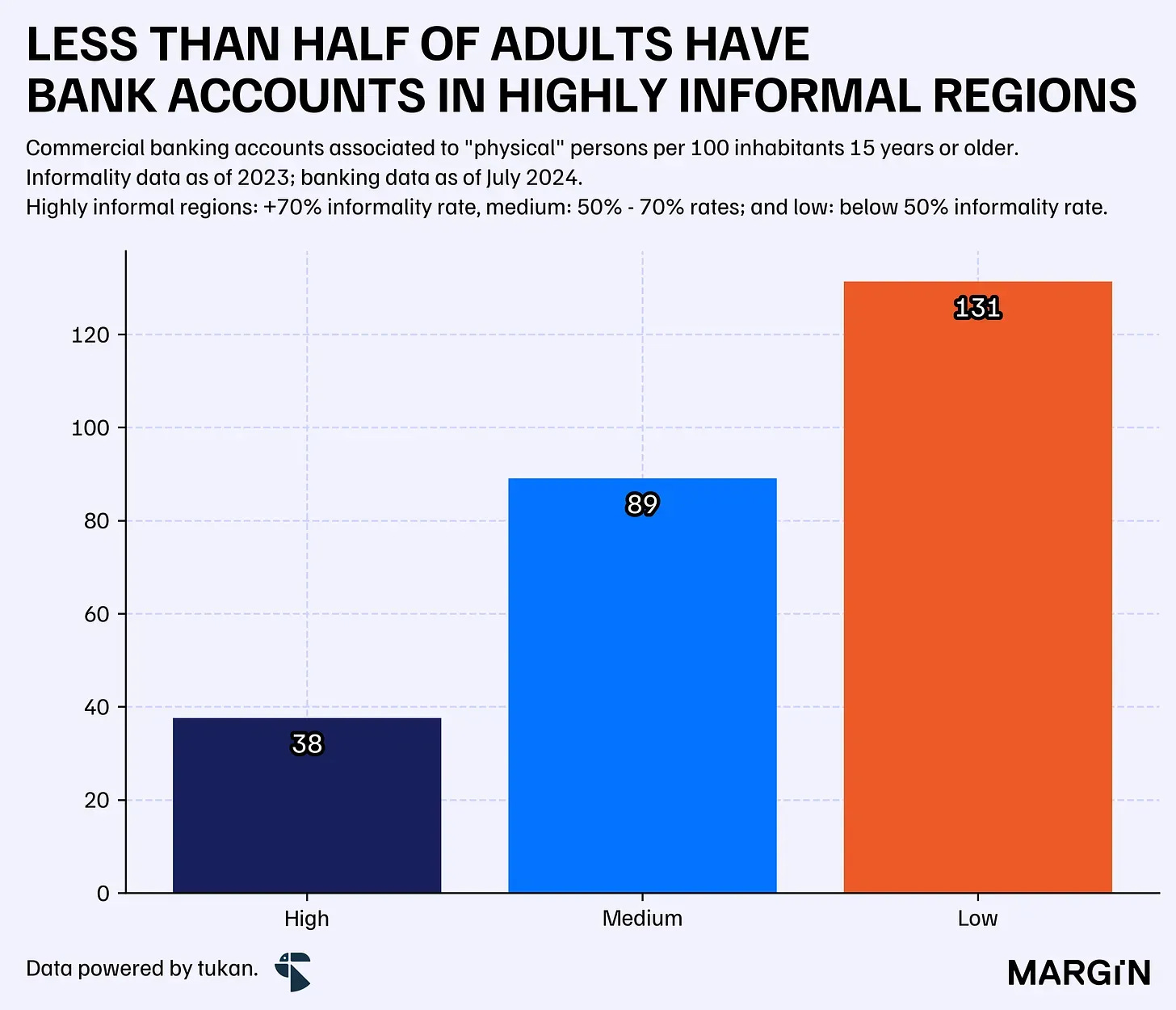

Similarly, we found that highly informal regions exhibited a 57% lower bank account per capita rate compared to “medium” informal areas in Mexico. This highlights how the non-formal economy continues to be a major bottleneck in achieving financial inclusion.

According to the latest CNBV figures, close to 40% of all non-corporate bank accounts in the country were payroll accounts. One that is usually thought of as the first financial product for consumers; and one completely out of reach for Mexicans working “off-the-books”.

However, not all is gloom and doom from a financial inclusion perspective. According to CNBV data, the number of accounts per capita in municipalities with informality rates over 70% increased by more than 14% compared to 2020, implying an absolute growth of over one million new bank accounts in those areas.

“Average” municipalities posted even better results, with the number of active bank accounts increasing by 22% during the same period.

Not surprisingly, average account balances were lower in municipalities with a higher share of non-formal jobs—34% lower than in areas with low informality rates.

To close off, let's examine bank loans and the contrast in banking loan exposures across different informality levels.

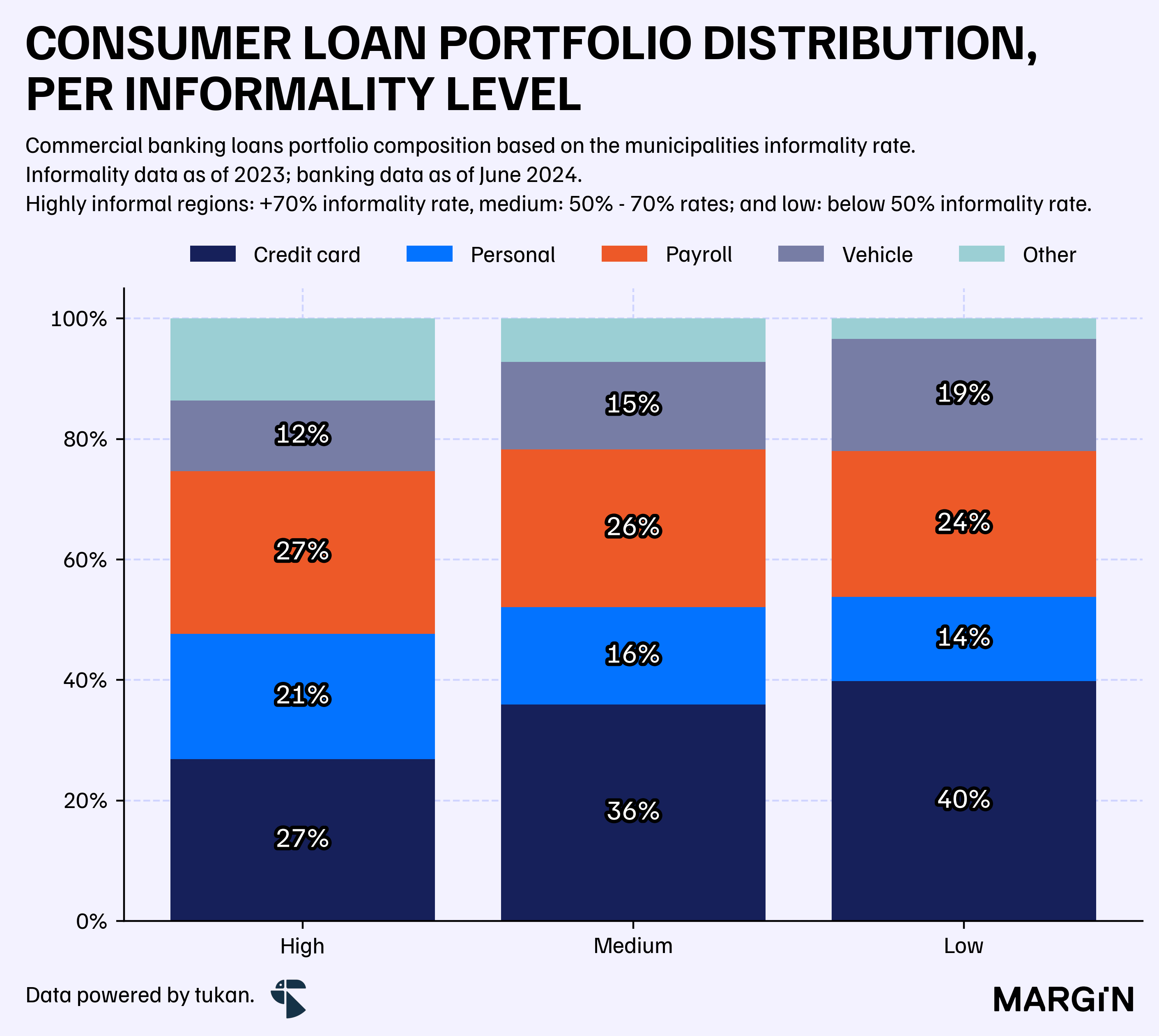

According to the latest regulatory data, consumer loan portfolios varied significantly across these regions. In highly non-formal municipalities, loan portfolios were predominantly composed of direct personal loans, whereas in other regions, credit card loans made up the majority.

Other notable disparities included the distribution of vehicle loans, which were over 3 percentage points lower as a portion of the total portfolio in these high-informality regions compared to “average” and low-informality municipalities. Additionally, there was a higher share of group loans in areas dominated by the non-formal economy.

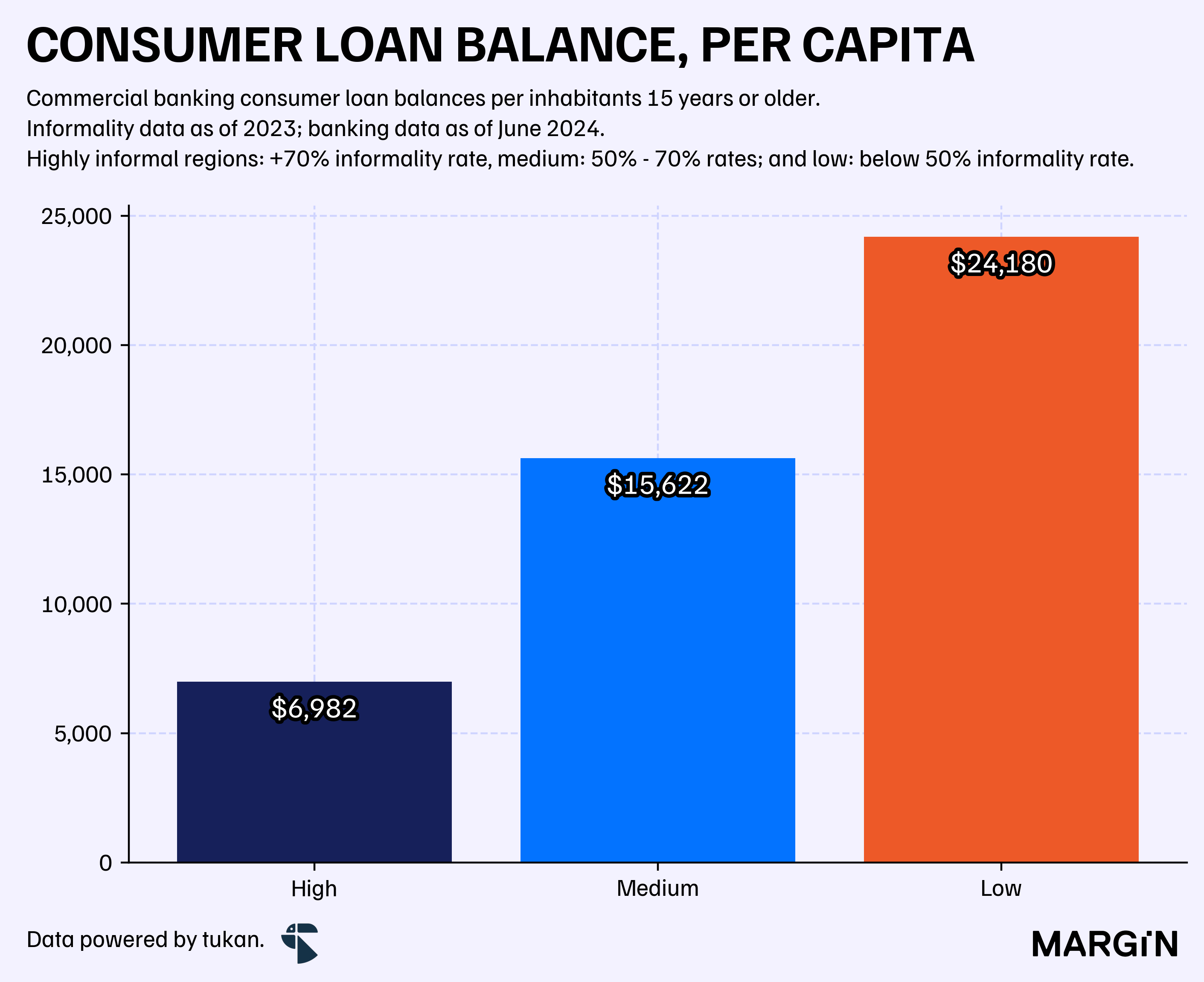

Unsurprisingly, loans per capita and portfolio exposure for banks was much lower in areas were most of the economy operated under the radar. According to CNBV, just 9% of the total loan portfolio was allocated to these municipalities; a staggering difference to the 63% allocated to municipalities with below-average informality ratios.

For reference, remember that highly informal regions hosted close to 23% of the population, and 43% resided in municipalities with low informality rates.

It’s no question that financial inclusion and labor informality go hand in hand. If the target is to increase accessibility to financial services, then targeting highly-informal municipalities seems as the best place to start; at least from a social standpoint.

However, can companies turn these regions dominated by cash and obscure economic landscapes into a profitable business venture? Will banks start taking risks into these geographies as the rest of the country overcrowds with competitors?

Here we consider 100,000 people 15 years or older.