Cautious

There's too much expectation behind foreign direct investment. Could it be slowing down?

Foreign direct investment (FDI) flows into Mexico surpassed USD $35 billion during the first three quarters of 2024, a figure 1.4% higher than the same period last year, keeping the indicator near record highs.

In recent years, FDI has been widely regarded by analysts and businesses as a clear signal of nearshoring trends taking shape in Mexico. It has also become a centerpiece in the government’s narrative of economic success, often touted as proof of the country’s growing attractiveness to international investors.

While it’s true that FDI into Mexico has been showing encouraging dynamics, we believe that recent datapoints reveal enough reasons to approach this optimism with caution.

According to data from Banxico, new investments — i.e. fresh capital into the country — accounted for just 5.7% of total FDI flows during the first three quarters of the year. A ratio, by far, the lowest ever seen since the central bank publishes it’s data.

On the other hand, reinvested earnings by foreign companies reached a record high of 86% — up 13 percentage points when compared to last year.

As with any economic indicator, relying too heavily on a specific component of FDI is not always ideal, especially if this dependence stretches over long periods of time.

In a healthy investment environment, you’d expect a good balance of FDI flows, with contributions from both new investments and reinvested earnings. This balance reflects the ability to attract fresh foreign capital while keeping previous investments sustainable.

According to Banxico data, Mexico has managed to maintain a fairly balanced distribution of FDI flows over the past 10 years. However, the significant drop in new investments over the last two years is worrying and could signal a potential shift, particularly given the current political uncertainty.

The recent slowdown in new investments could face additional pressure, as expected flows from public announcements collected by the Secretaría de Economía are projected to total USD $64 billion for 2024. While this is an impressive figure, it represents a 26% decline compared to the previous year.

Moreover, in 2024, aggregate investment figures from public announcements have surpassed the USD $10 billion threshold only twice in the first three quarters. By comparison, this milestone was reached four times during the first nine months of 2023.

Also, it’s important to keep in mind that public announcements are just expected investments which don’t always materialize; or may take years to come into fruition.

While this may seem like a pessimistic view, we believe the greatest risk of a slowdown in foreign capital injections isn’t the easing of FDI itself, but the failure to meet the high expectations that the country as a whole has assigned to this trend.

If those expectations fall short, could they leave some businesses in a vulnerable position?

For more on this, we recommend you revisit our deep dive into the trucking sector in Mexico and their role in the nearshoring boom.

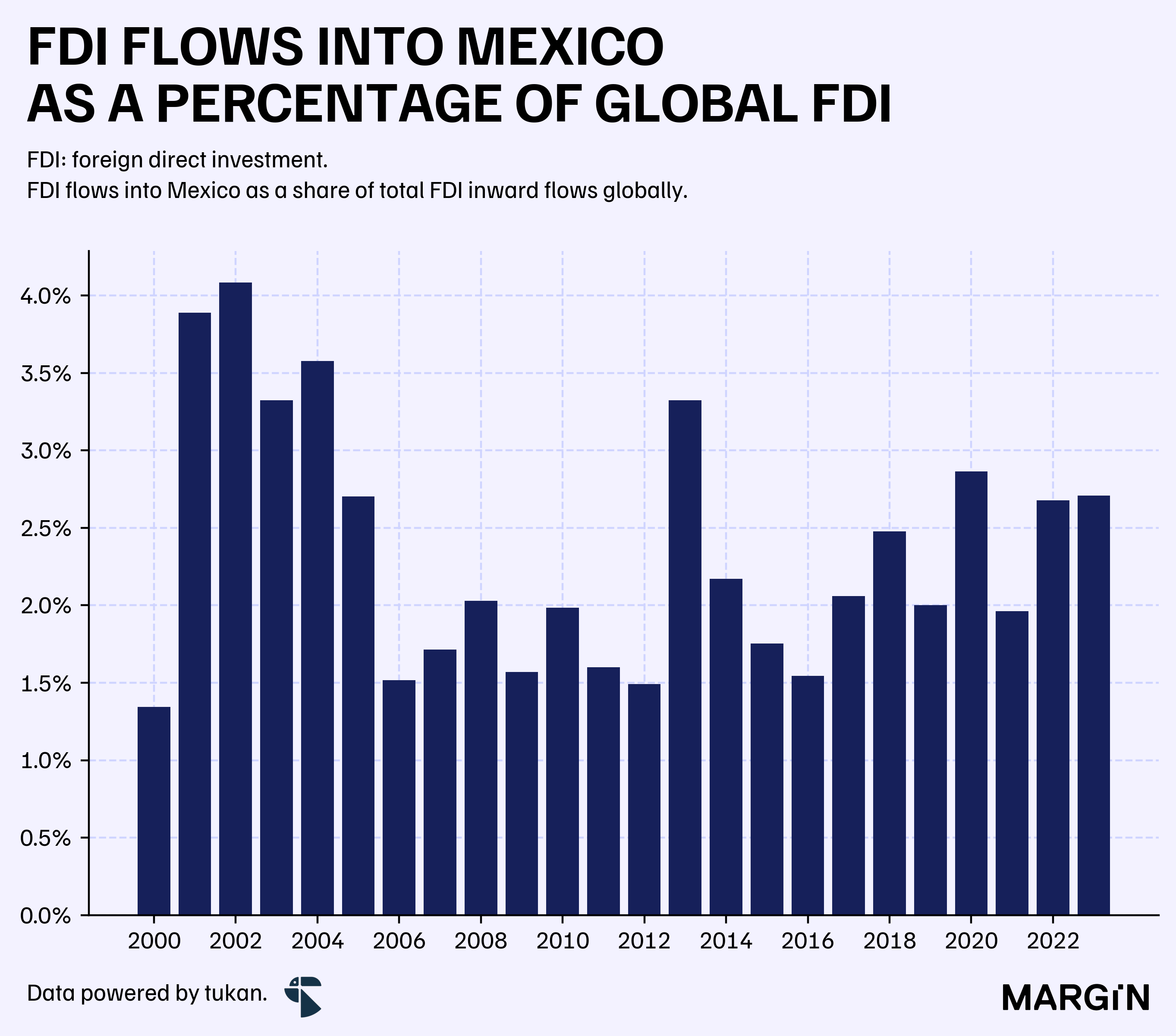

Global data published by UNCTAD shows that Mexico has been a resilient player in the FDI space, though it hasn’t necessarily outperformed other major economies.

On a global comparative basis, Mexican FDI gained between 25 and 50 basis points of “market share” in the global economy over the past four years.

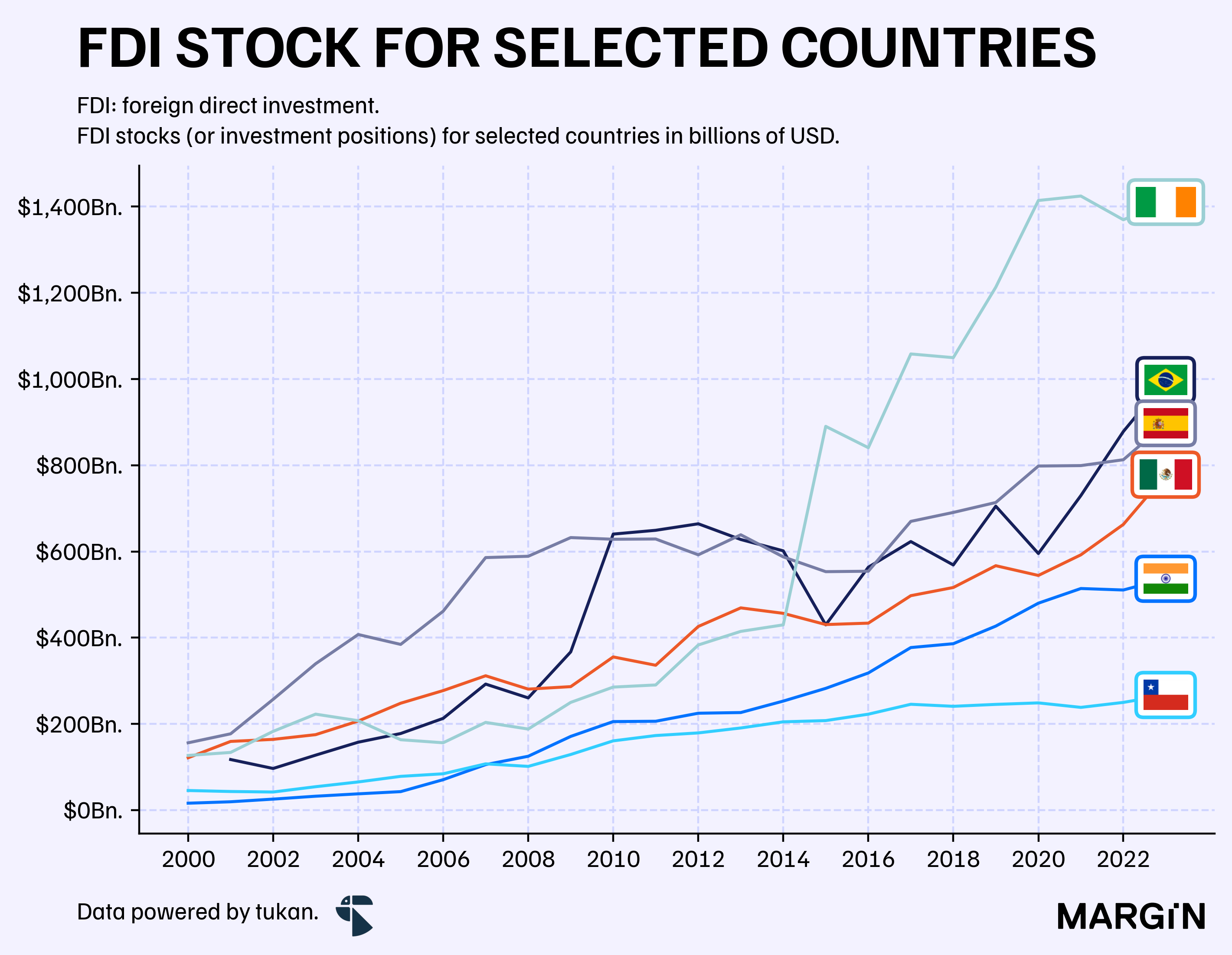

The increased share of capital flowing into Mexico has pushed FDI stocks (or investment positions) to over USD $770 billion as of 2023. This has narrowed the gap between Mexico and its closest competitors, Spain and Australia, but at the same time further widening the distance from Brazil, the top-ranked country in Latin America for this metric.

According to UNCTAD figures, Mexico has consistently held its position as the 17th highest-ranked country in the world in terms of FDI stock for over a decade.

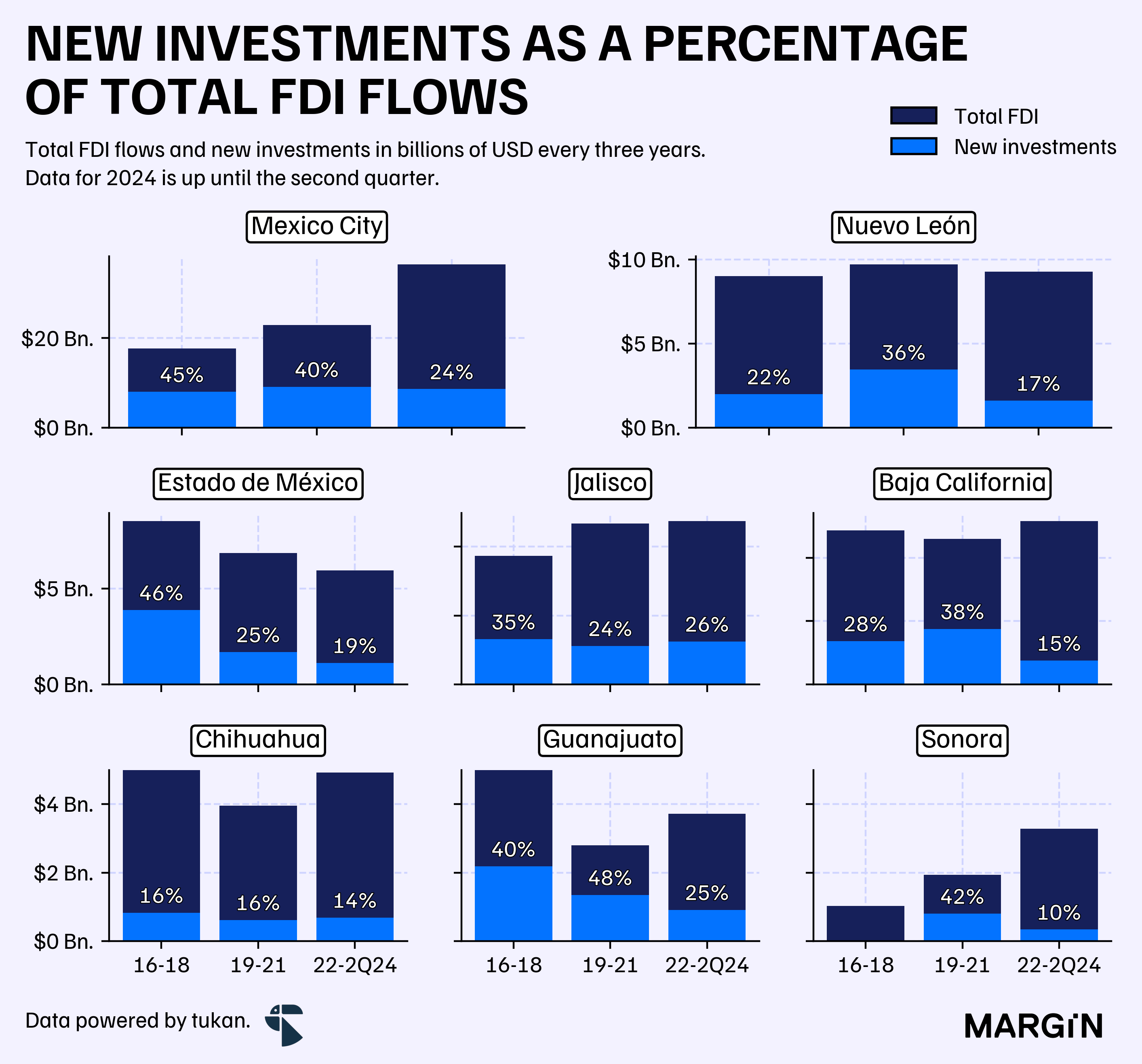

At a local level, the top nine states with the highest share of FDI flows exhibit a similar trend in their declining ability to attract fresh foreign capital.

With the exception of Sonora and Jalisco, new investments as a percentage of total invested capital have declined across these regions when comparing flows from 2022 onwards with those from 2016 to 2018.

The drop in the share of new investments is particularly notable in Mexico City, Estado de México, and Guanajuato, where it has fallen from over 40% to no more than 25%.

Please note that the previous chart aggregates data in three year periods, and the latest one (2022 - 2024) has two quarters fewer in the sample; which is why total FDI flows are lower than for previous periods.

Overall, Mexico has proven to be a strong destination for foreign capital in recent years. Whether this momentum can continue into 2024 and fulfill the promise of nearshoring under a Trump presidency and heightened political uncertainty in Mexico remains to be seen.

Early warning signs of stagnation are already emerging in the latest 2024 data points, making the data from the next few quarters crucial in gauging investor appetite for opportunities in Mexico.