The Road Ahead

Analyzing the truck-freight landscape in Mexico and the companies that drive it forward.

In 2010, there were close to 21,000 businesses providing freight-trucking services in Mexico.

Fast forward to 2023, and the number of businesses has grown by a staggering 85% to over 39,000 companies. The aggregate vehicle fleet now exceeds one million units—more than double the number reported in 2010—with 61% of the vehicles owned by over 5,000 medium and large companies (i.e., those with more than 30 vehicles in their operation).

It is worth noting that there are over 160,000 owner-operator businesses (i.e., those with fewer than 5 vehicles) operating within the country. In aggregate, these “single-truck operators” had a vehicle fleet of over 300,000 units at the end of 2023.

According to regulatory data, the cargo vehicle fleet in the country experienced most of its growth during 2019, the year in which the number of units first surpassed the one million mark. Despite some deceleration, growth has not stalled, with fleet figures expanding by 6% year-over-year in 2023—equating to almost 80,000 units added during the year, the second-highest increase in a span of 14 years.

It’s important to note that the cargo vehicle fleet is evenly distributed across two different types of vehicles: motor units (i.e., those with an engine, such as trucks and tractors) and towage units (such as trailers, semi-trailers, and the like).

In total, the number of motor and towage units closed 2023 at 670,000 and 660,000 vehicles, respectively.

In today’s Margin article, we analyze the truck-freight landscape in Mexico, exploring which business are acquiring the most vehicles in recent years, as well as giving some perspective on the industry’s growth as a whole.

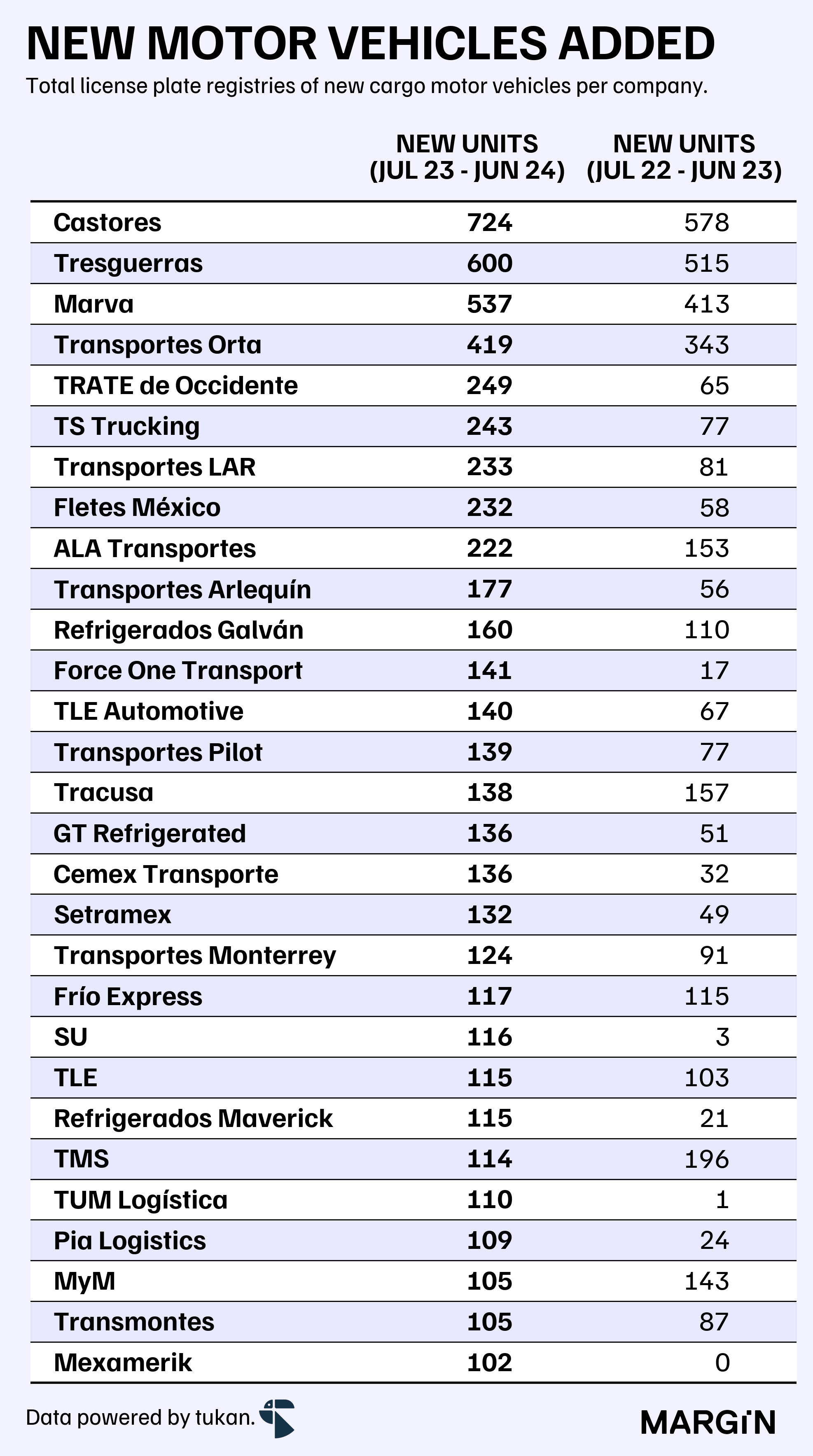

Focusing solely on motor units, SCT data reveals that cargo operators registered over 23,000 brand-new vehicles in 2023, representing a 56% year-over-year increase. Furthermore, close to 12,000 new vehicles were registered during the first six months of 2024, setting a record for a first semester since the SCT began publishing data.

Over the past 12 months1, more than 3,200 companies have invested in at least one new motor vehicle for their operations. Among these, 400 companies registered over 10 units, and 29 companies acquired more than 100 units.

The following table lists the 29 companies that registered over 100 units between July 2023 and June 2024.

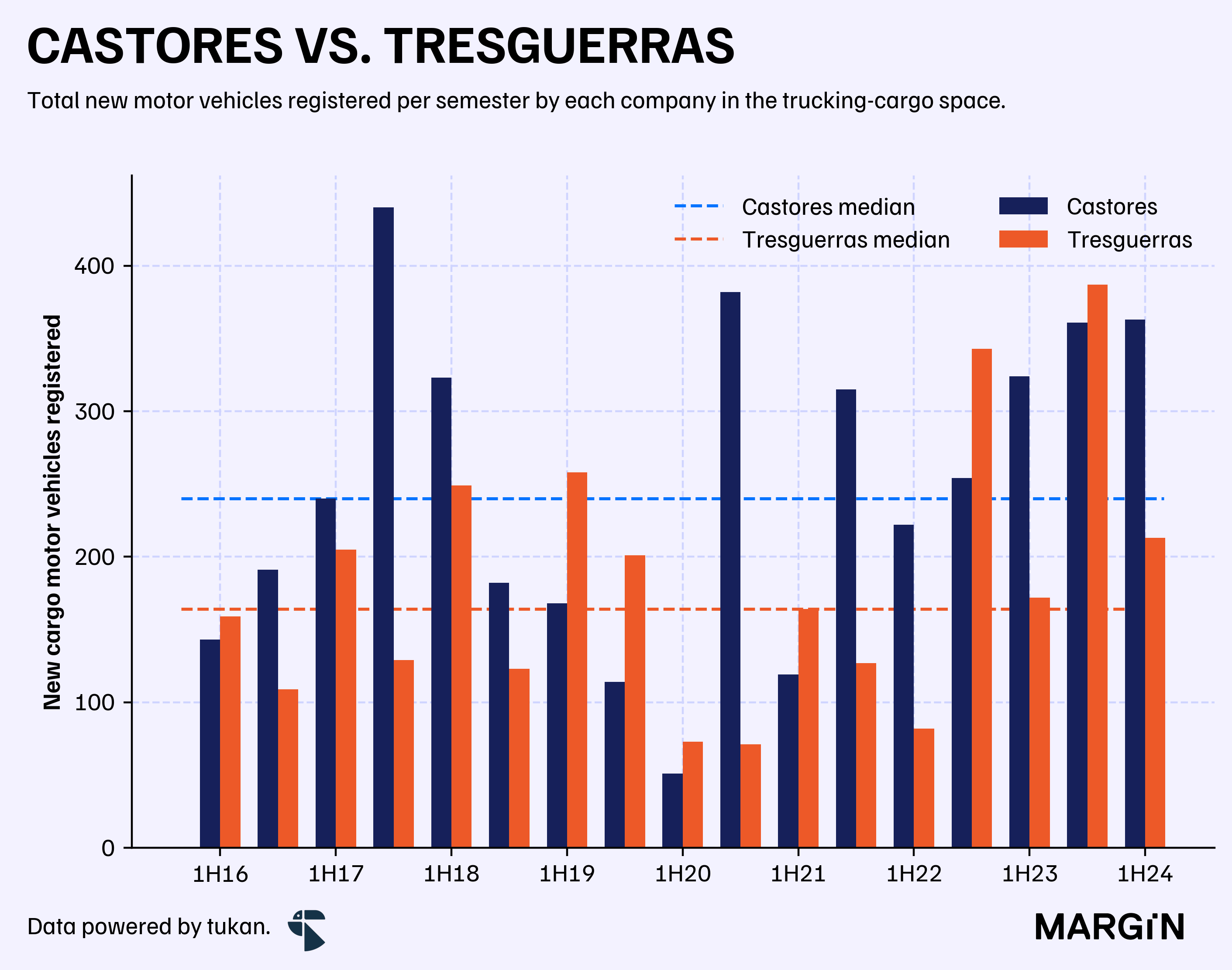

Zooming into the data for Grupo Castores and Tresguerras, two of the major players in the space, we can see that vehicle purchases (or registrations) have been considerably above the median for both companies since the second half of 2022.

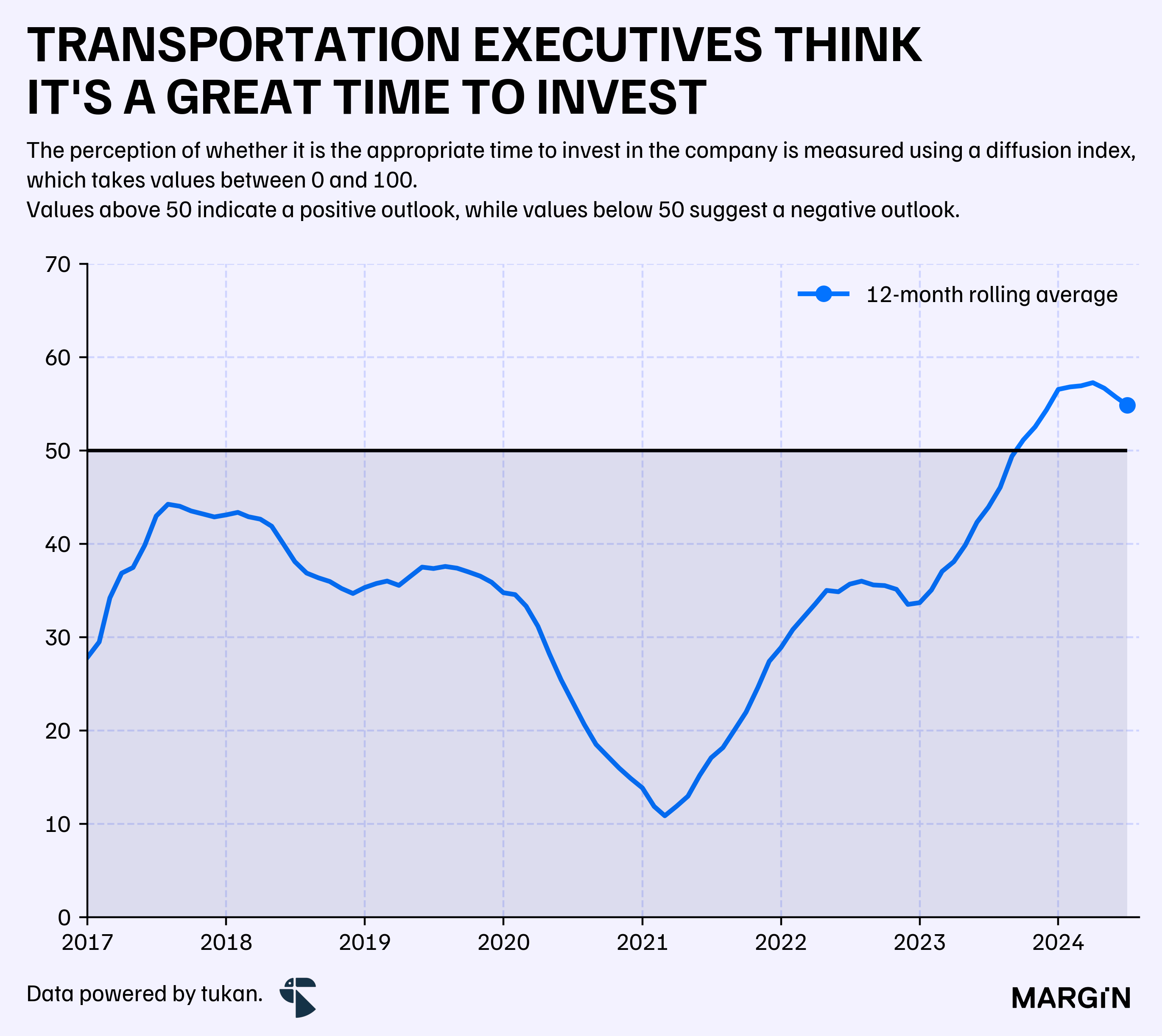

This coincides with INEGI’s business expectations survey, where executives in the transportation industry appear quite optimistic about the economic environment.

According to the INEGI survey, and when adjusted for seasonality, the index related to “investment timing” has never been higher for the industry—surpassing the threshold of positivity for the first time since the institute began publishing data for this sector2.

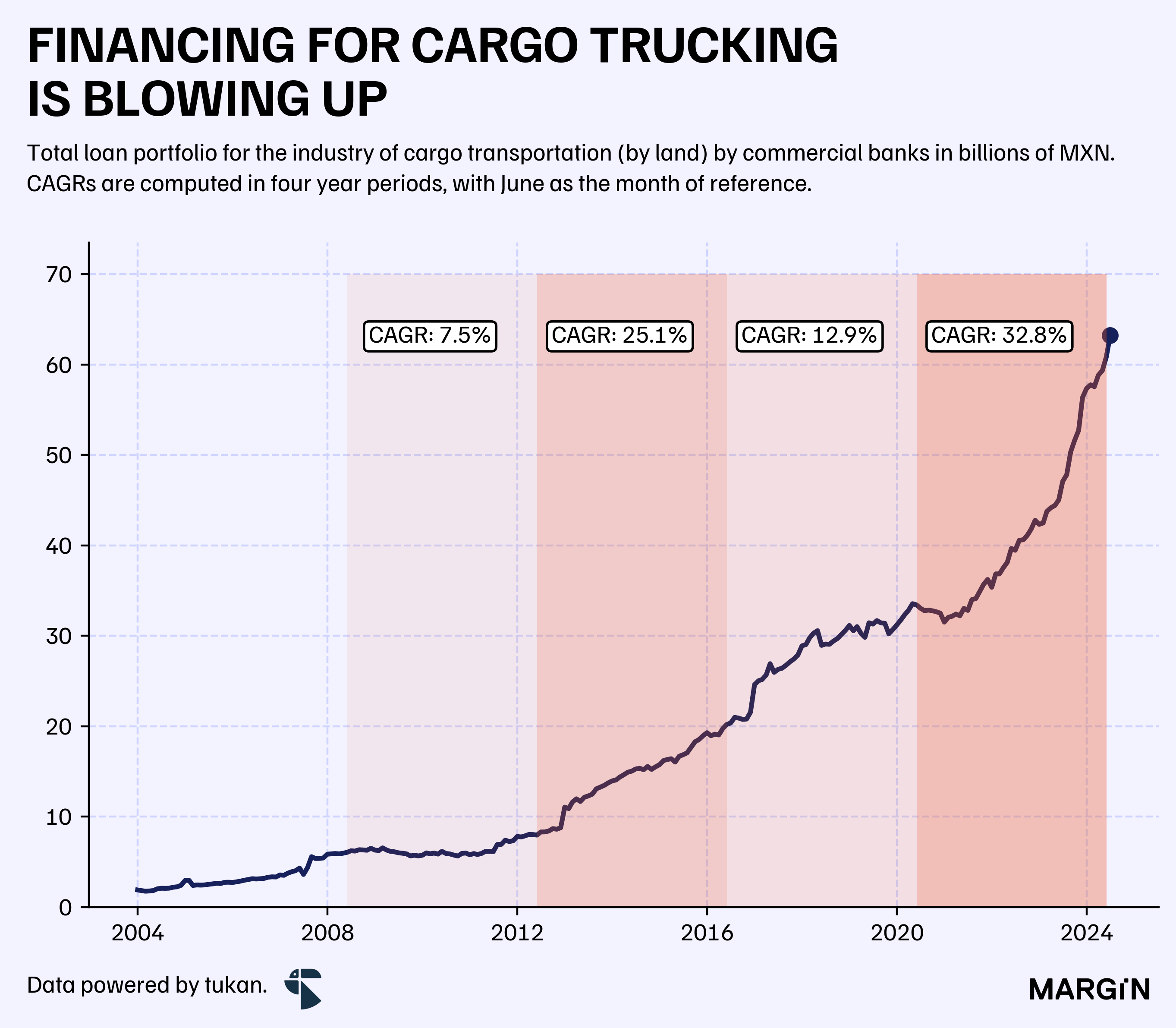

Interestingly, trucking company executives are not the only ones optimistic about the industry. According to Banxico data, the total loan portfolio from commercial banks to land-cargo transportation surpassed $60 billion MXN this year and boasted a 4-year CAGR of 33% at the end of June.

However, not everything is necessarily positive within the truck-freight landscape. According to INEGI data, 2023 was a challenging year for the industry, with revenue indices dropping by an average of 9% YoY.

That being said, data from May this year shows the trucking industry getting back on track, as revenue indices spiked by 17% YoY, albeit from a lower comparable base.

Historically, land-transported cargo has always had the upper hand in foreign trade operations from Mexico. Nevertheless, recent data shows that the rolling 12-month total value of shipments in export operations by land has grown at a 4-year CAGR of 11%, compared to 9% for other transportation methods.

All in, the value of foreign trade operations by land exceeded $656 billion USD during 2023 and are closing the first five months of this year at a total value of shipments of $282 billion USD — 5% more than last year.

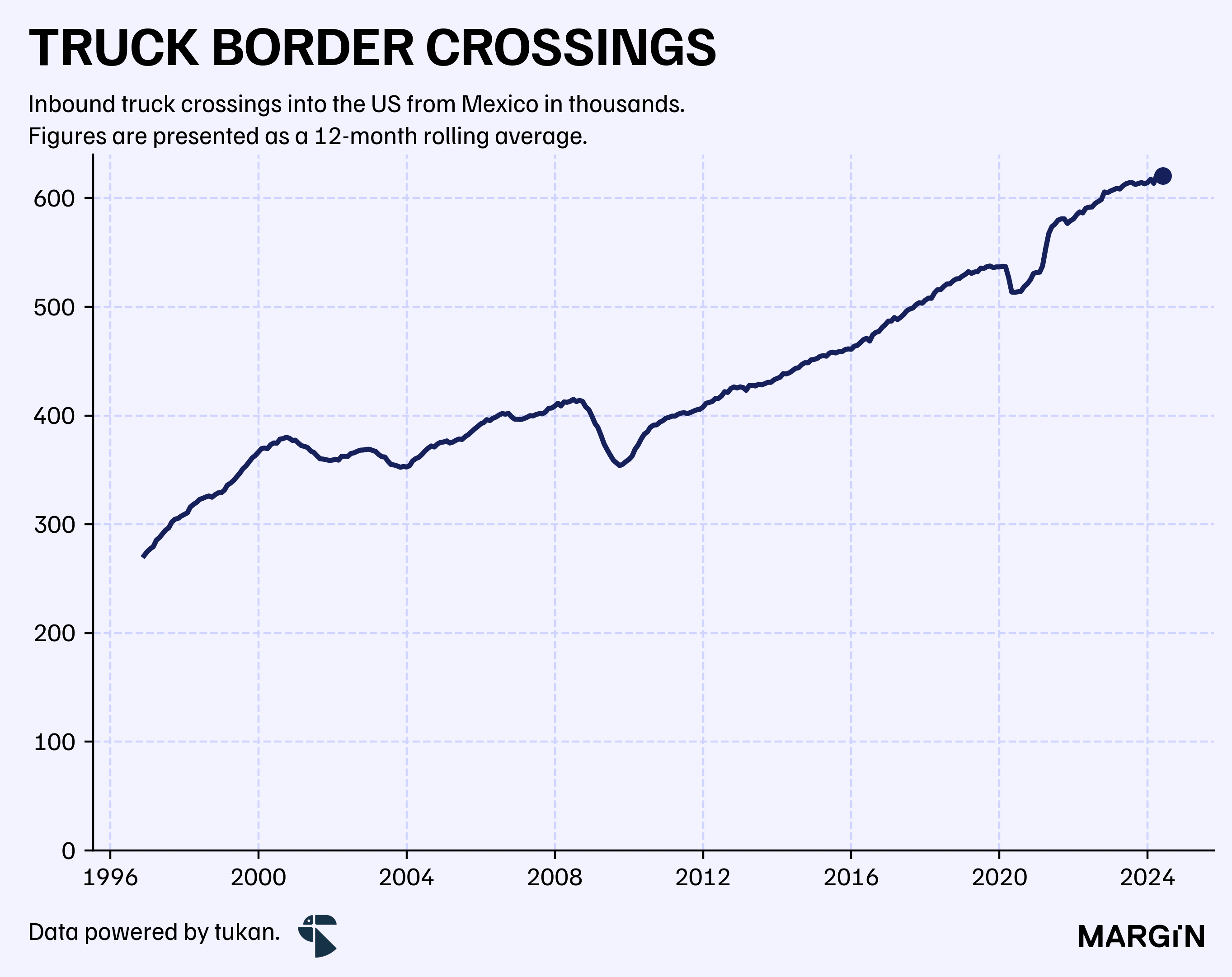

On the other hand, BTS data from the United States shows that truck border crossing during the first half of the year surpassed 3.8 crossings from Mexico into the US (+2% YoY). A figure that seems to have stabilized since the spike observed in 2021.

As supported by our latest piece, the freight-trucking industry seems to be investing heavily due to the hype around the nearshoring and internal logistics trend. However, margins seem to be contracting across the industry and despite posting a good revenue figure during May, it seems it might still take a while until we can have enough data to assess the outcome of these investments.

For now, one thing is clear. There is hope that this bet will payoff.

Refers to license plate registrations made between July 2023 and June 2024.

Business expectations are measured using a diffusion index, which takes values between 0 and 100. Values above 50 indicate a positive outlook, and viceversa.

Una consulta, ¿cuentan ustedes con bases de datos de las empresas transportistas en México, tanto de las grandes, medianas, y los hombres camión,, que manejaron en su artículo The Road Ahead?