High Margins

Uncovering the most profitable service industries in Mexico.

According to the latest census from INEGI, non-financial service-related companies in Mexico generated an operating profit1 of over MXN $1.3 trillion during 2018, implying an operating margin of approximately 32% for businesses within this sector.

The non-financial service industry in Mexico constitutes over 36% of the country's GDP and employs more than ~40% of the total workforce, underscoring its significance in the nation’s economic model.

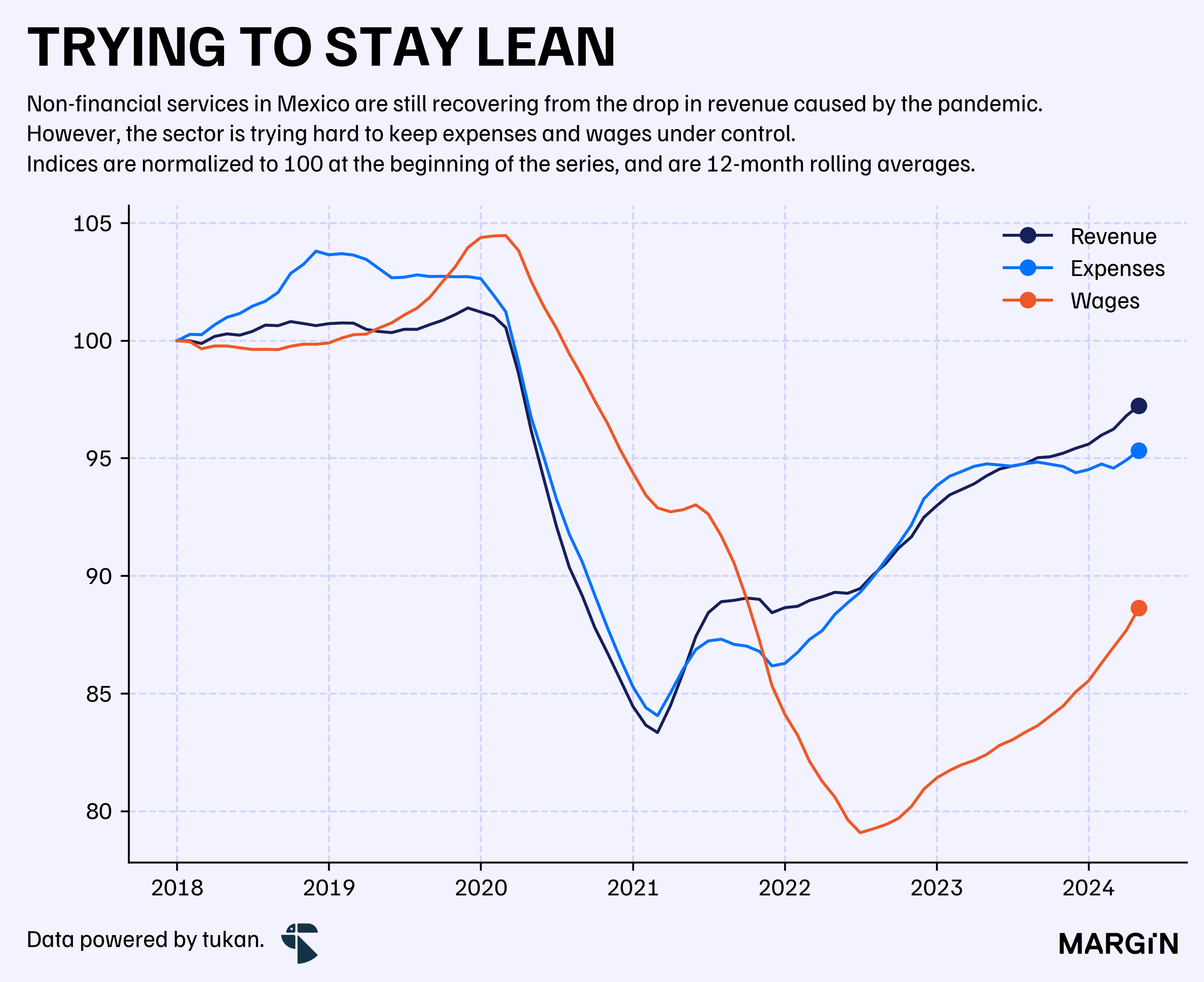

However, most service-related industries have experienced contractions in their overall income when compared to 2018. Out of the 58 industries tracked by INEGI on a monthly basis, only half have recovered to their pre-pandemic levels.

Note that INEGI presents all indices adjusted by inflation, so the growth figures presented in this article are all expressed in “real terms”.

This situation has forced Mexican service businesses to significantly reduce total costs — and in particular — wages to its employees. As of 2024, total wages and operating expenditures are down 15% and 8% from their peaks in 2020 and 2018, respectively, dropping below income levels and thereby improving overall operating margins for companies.

In today’s article, we take a dive into the census database and extrapolate our findings with recent economic surveys to uncover which service industries are becoming the most efficient and high-margin in the country.

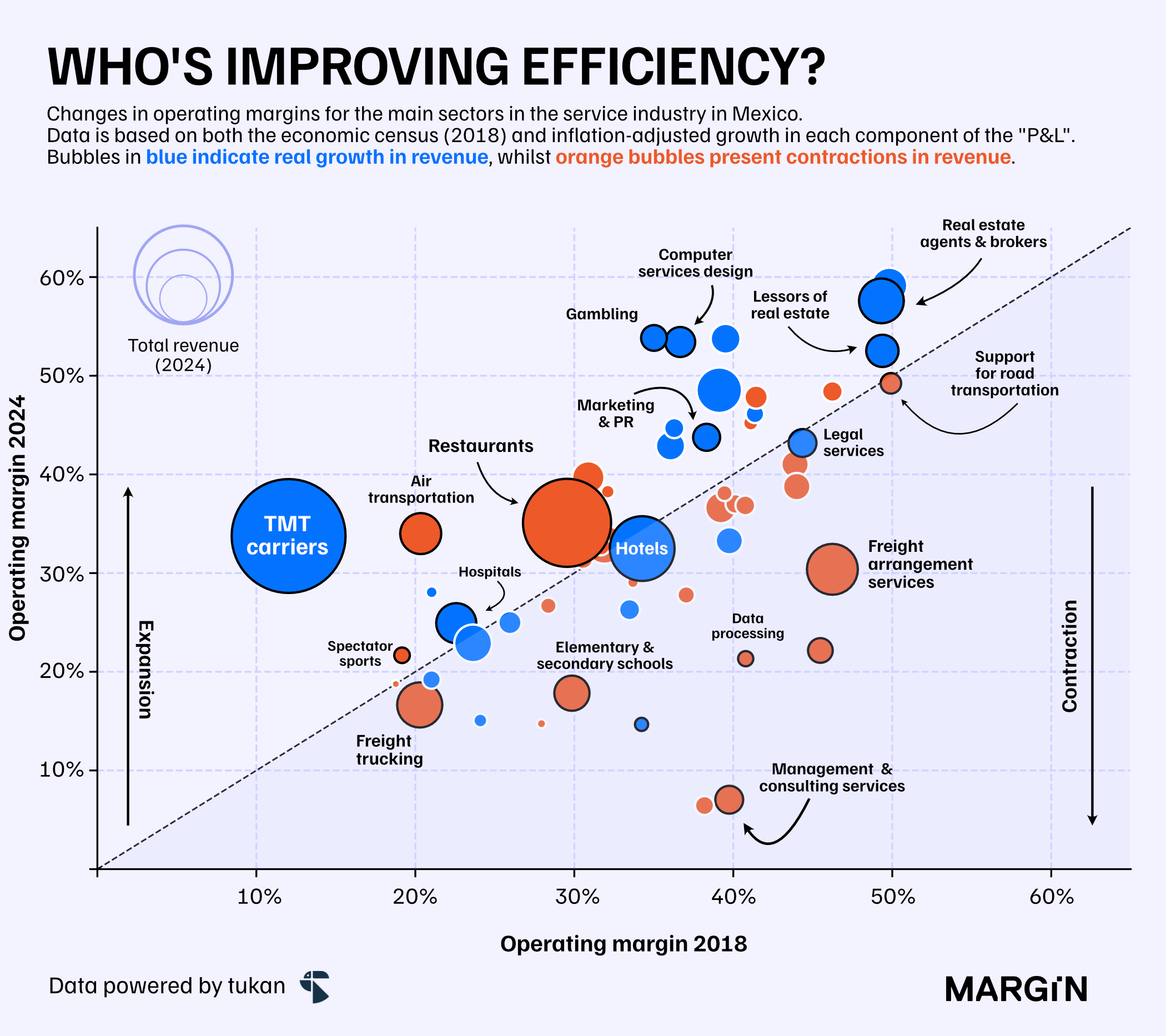

Based on INEGI data, we estimate that operating margins improved by approximately 380 basis points over the past six years and could see further upticks in efficiency as economic activity within the industry continues to recover from the shock caused by the pandemic.

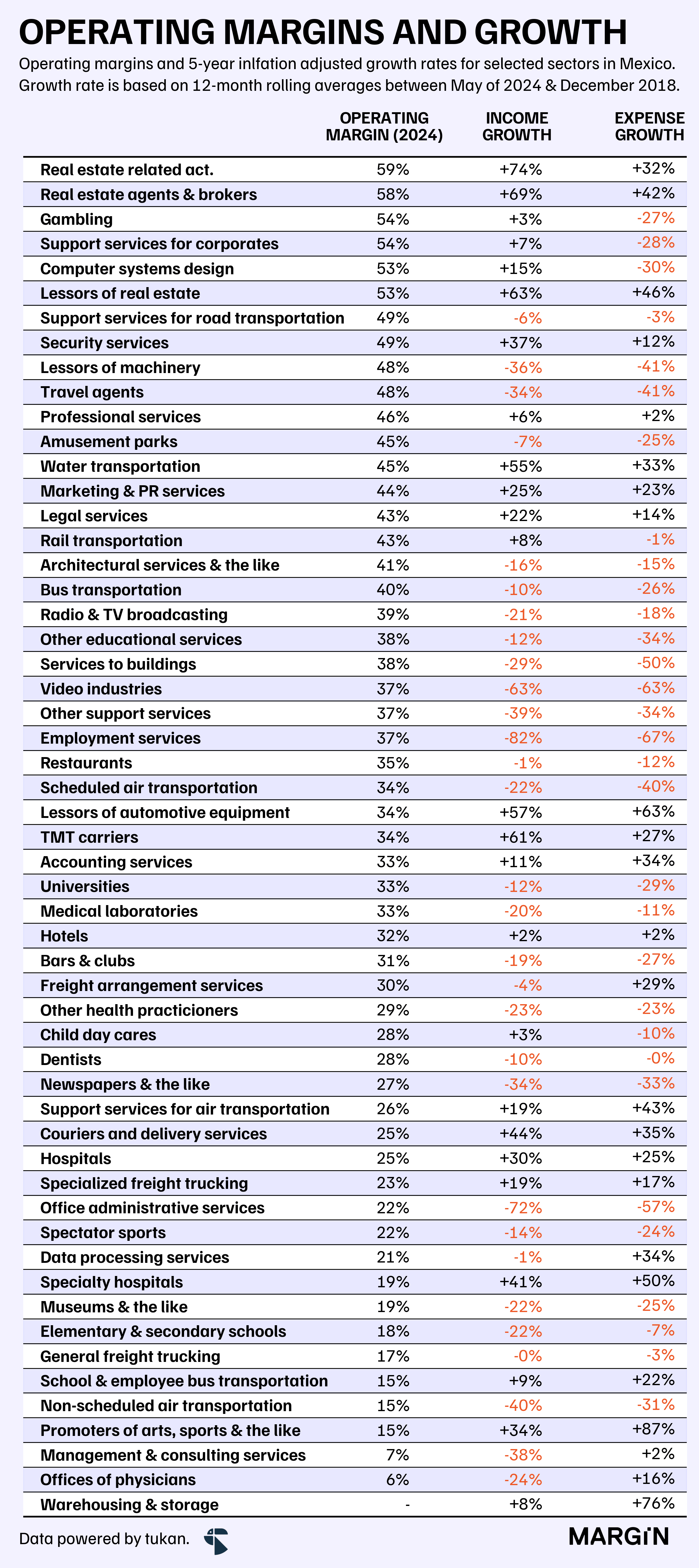

At an aggregate level, we identify TMT, gambling and computer services design (software) as some of the industries with the highest overall margin expansion within the country. In the following chart, we present 2018 vs 2024 operating margins for each of the 58 industries tracked by the Mexican Statistical Institute.

The previous chart sheds light on some important points. First, of the 25 industries that have reported margin expansions, almost half have also suffered contractions in their revenue. Conversely, only 11 out of the 33 sectors with margin contractions have seen improvements in their top line.

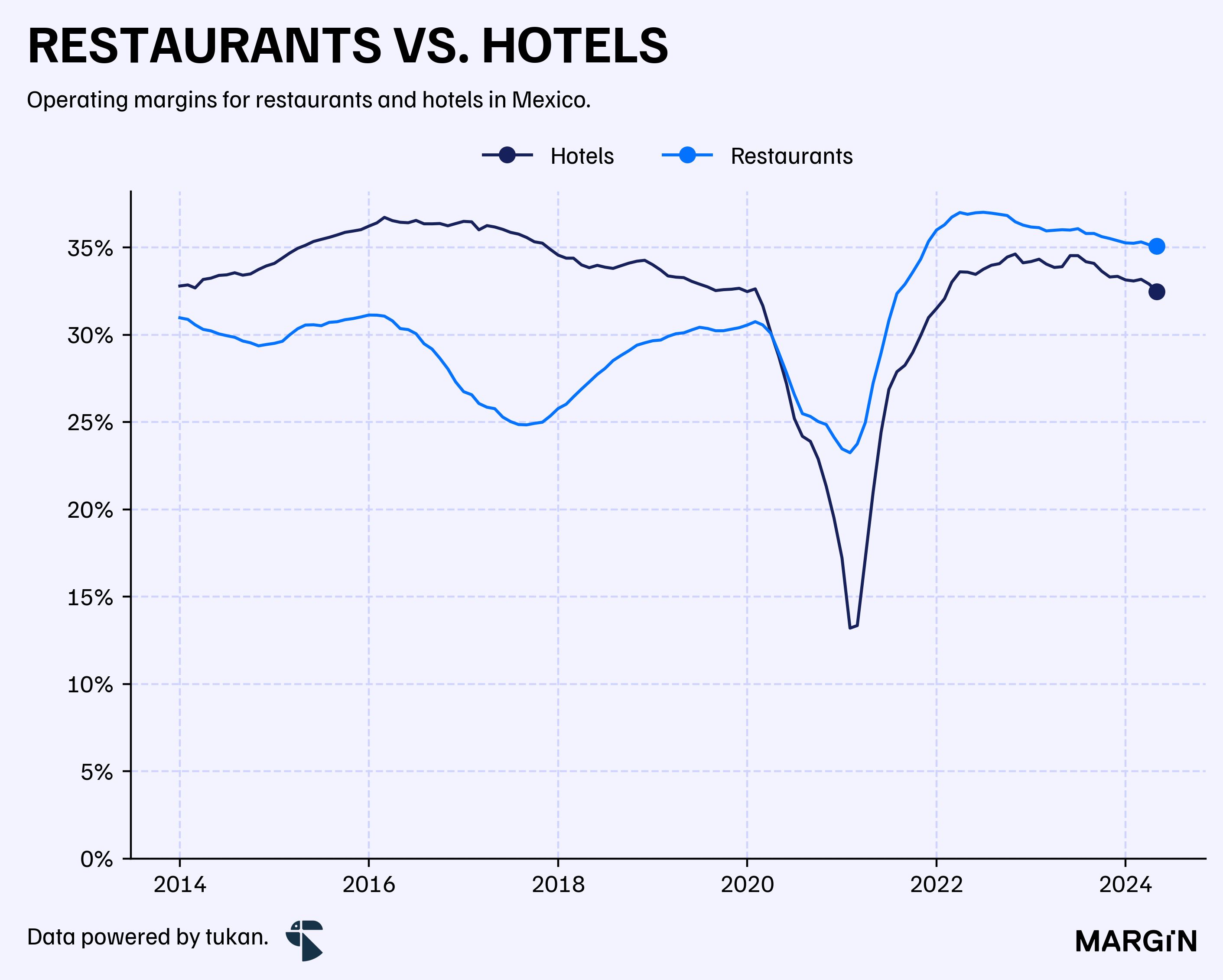

Restaurants and hotels, two of the most important industries within the services segment in the country, serve as a good example of this.

According to our estimates from INEGI data, hotels traditionally boasted higher margins than the food service industry. However, this trend appeared to be reversing even before the shock from the pandemic.

Since 2018, revenues for the restaurant industry have remained relatively flat (when adjusted for inflation), whereas for hotels, revenue has increased by approximately 2%.

Despite these opposing changes in revenue trends, restaurants have managed to reduce expenses by about 13% and control wage increases to around 6%. In contrast, hotels have suffered increases of 18% in total wages to personnel and 2% in operating expenses.

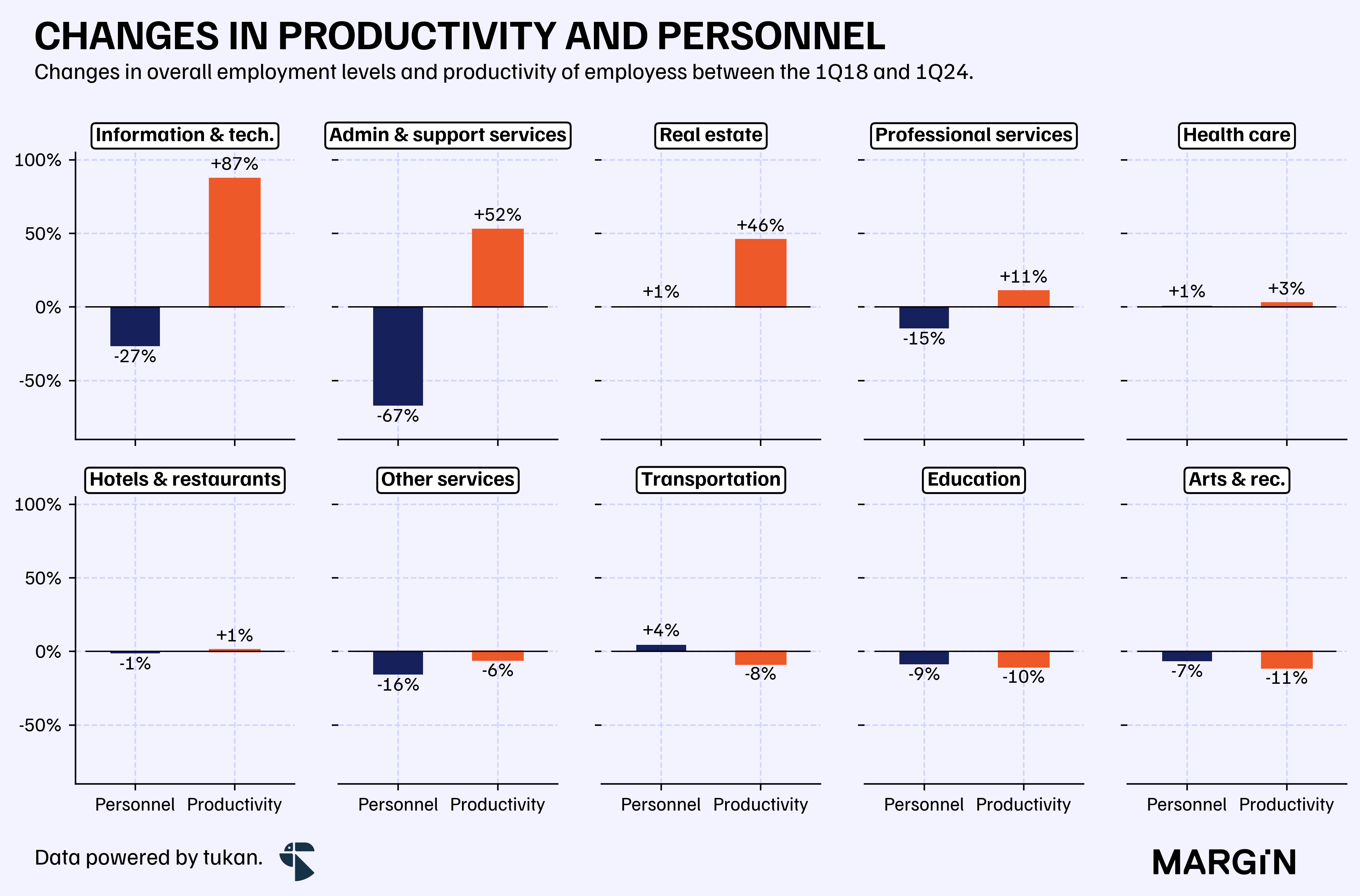

Overall, what we are seeing across the services industry in Mexico are stagnant employment levels, coupled with increases in productivity across some industries.

As businesses continue to recover from the sharp drop in revenue experienced in 2020, operating expenses are rising at a similar pace. Employment and productivity, on the other hand, are the only levers left for companies to control overall profitability.

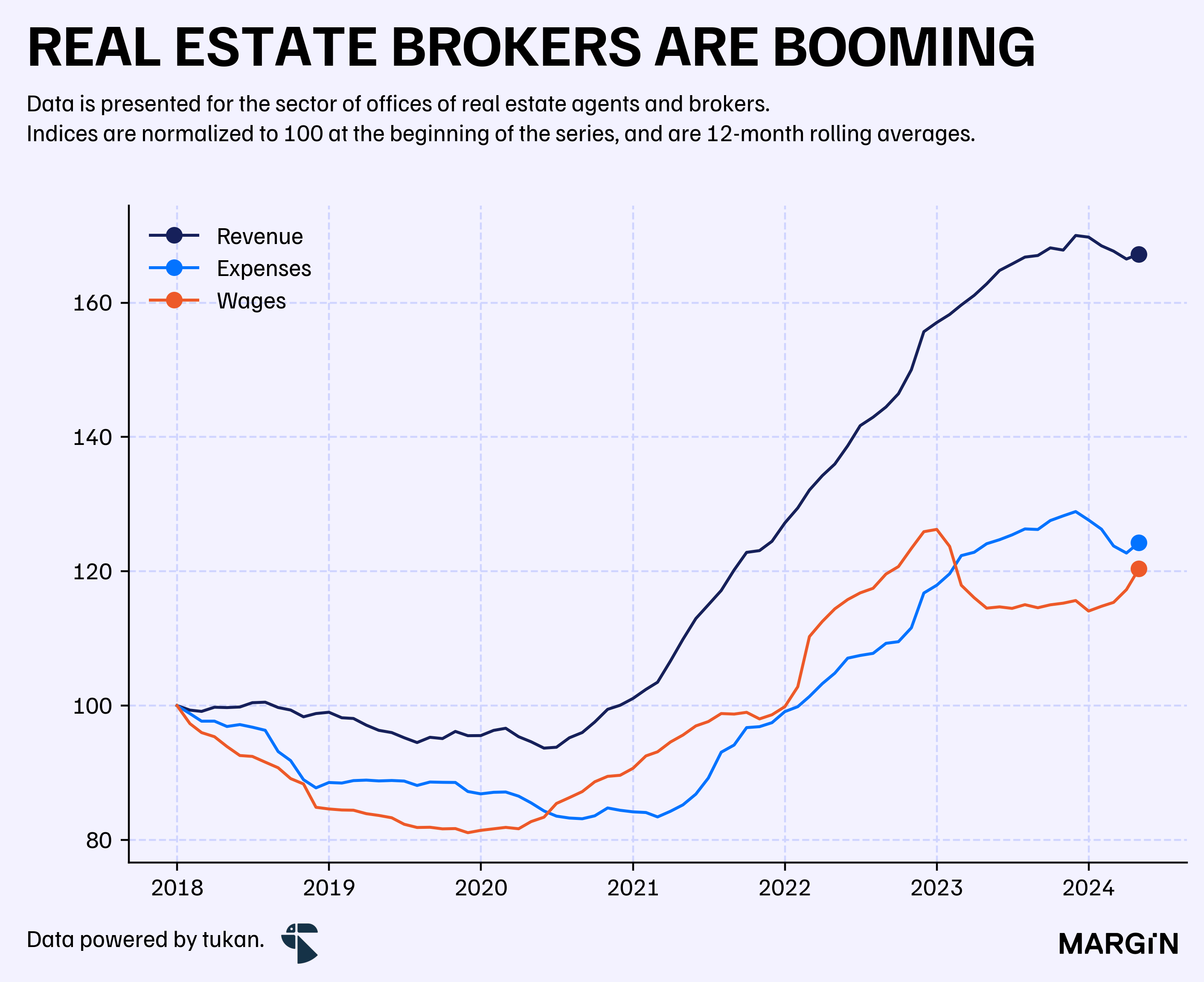

Out of the 10 major service sectors, only real estate services saw an increase in productivity with no major changes in employment levels.

According to INEGI data, the Mexican real estate service industry not only grew productivity by more than 45%, they also increased revenues by more than 69%.

We estimate that their overall margin expansion surpassed 800 basis points during the past 5 years.

By looking at the chart below, we can see explosive post-pandemic growth for an industry that seemed dormant between 2018 and 2021; most likely as a result of higher-household prices, and the high demand for industrial spaces.

All this, by keeping wages and expenses under control.

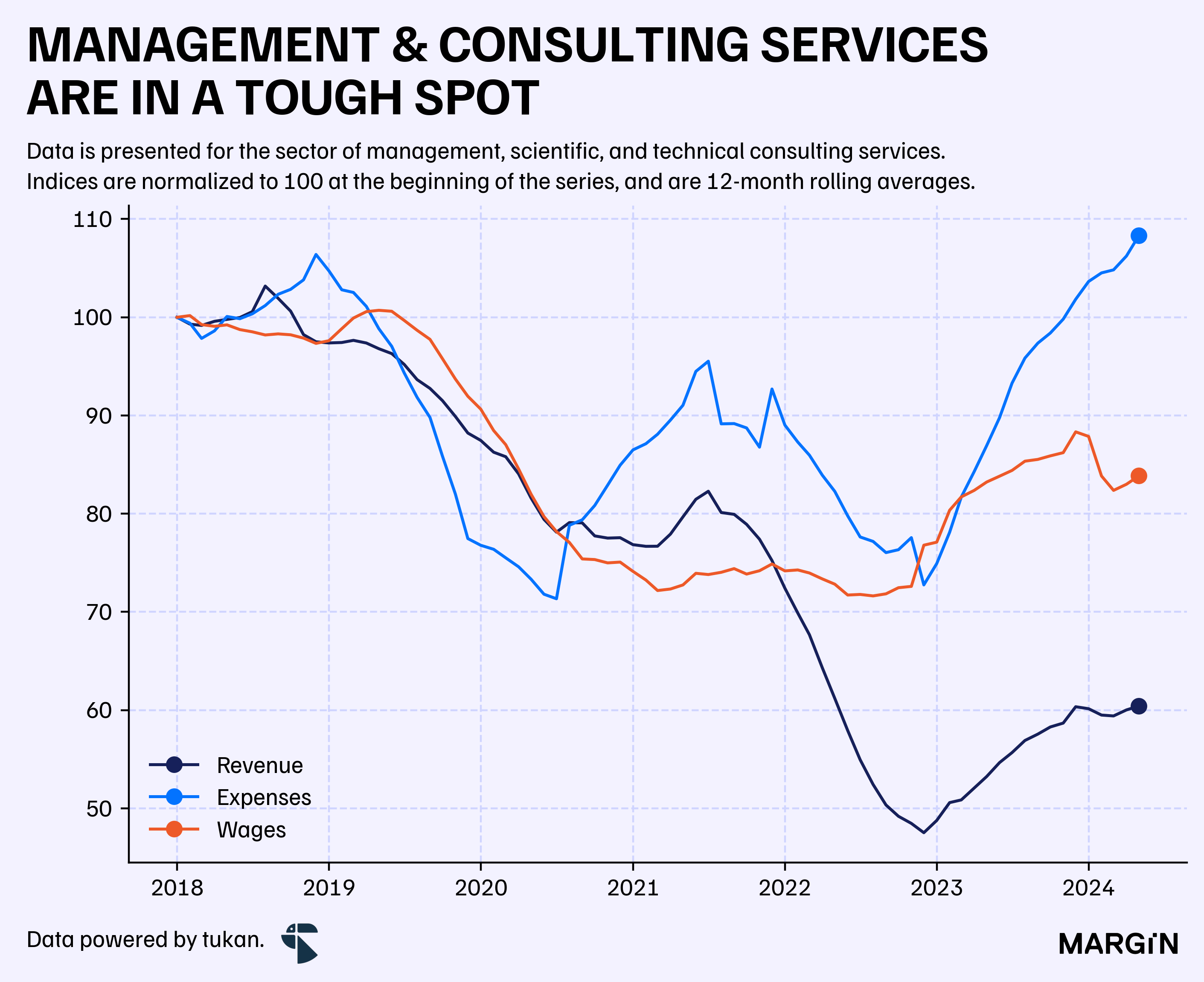

On the other end of the spectrum, we have industries such as management and consulting services. Despite showing some slight recovery in recent years, these industries continue to struggle with keeping expenses at bay and suffer from a downward trend in their overall income.

All in, the services sector in Mexico has shows mixed results across its major industries — with some, still suffering heavily from the downturns in 2020. Whilst others, such as freight trucking and transportation, seem to be investing heavily on personnel and other expenses to make the most of what they expect to be a profitable bet on the nearshoring hype.

For the full list of operating margins and growth of the sectors covered in this article, please refer to the following table.

Note that this is the overall inflation-adjusted growth rate over a 5-year period.

Foreword

Our goal with Margin is to create a newsletter that provides weekly, differentiated, data-driven insights on what’s happening across the Latin American economic and business landscape.

As we transition from the “legacy” version of this newsletter, we would love to hear your thoughts and feedback on this new type of content. If there’s any industry or topic in particular that you would like us to explore, please let us know.

Feel free to reach out to me at miguel@tukanmx.com with your thoughts and feedback.

Thank you for reading!

We define operating margin as the ratio of revenues minus the sum of employee related expenses and expenditures on goods and services, divided by total revenues.