Lean

A look at Mexico's most efficient bank.

Since 2018, there’s been one bank in Mexico that regularly stands out as the most efficient of them all.

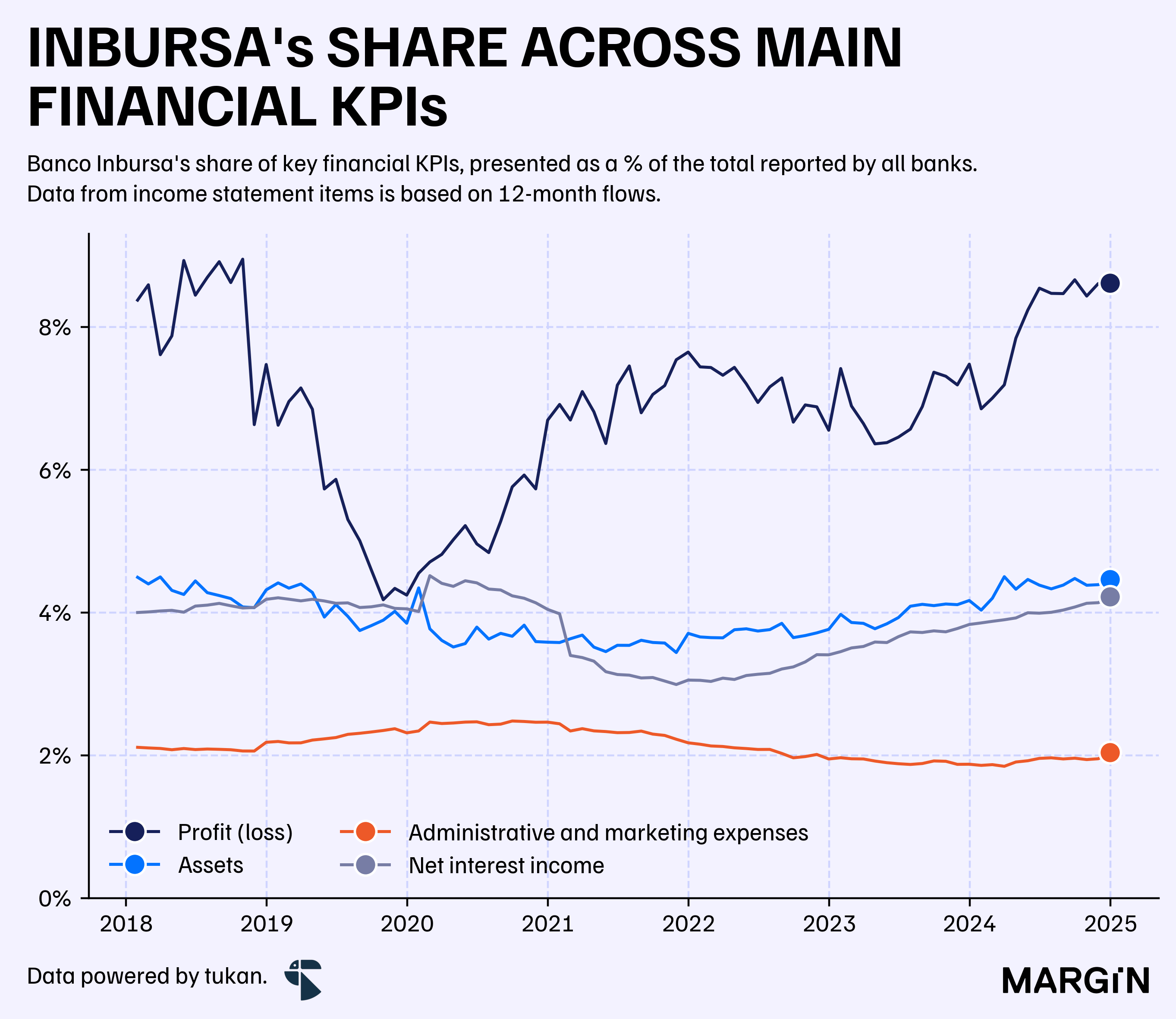

According to regulatory data, Banco Inbursa has consistently reported the lowest (i.e. best) efficiency ratio among commercial banks in the country during the past 6 years. As of 2024, general expenses for Inbursa amounted to $62 billion pesos — a figure equivalent to 24% of the company’s total revenues.

Financial institutions usually use the efficiency ratio as a measure to understand how much they spend in order to generate revenue. In this case, Inbursa would be spending $0.24 to make $1 peso of income.

This ratio was, by far, the lowest across the main commercial banks in the country and 8 percentage points lower than its closest competitor in the ranking (BBVA).

As expected, this has also turned the company into an incredibly profitable machine — ranking as the second most profitable bank in the country, according to its return on assets (ROA) reported at the end of December.

During 2024, Inbursa reported profits of over $25 billion pesos; an amount that beat the bottom-line figures recorded by Banamex, HSBC and Scotiabank, despite holding considerably lower assets than its peers.

At the same time, Banco Inbursa closed 2024 with more than $462 billion pesos in its loan portfolio—a figure equivalent to 6% of the Mexican banking system’s total loans.

However, one of the main strengths of the bank has been its notable strategic focus in certain products and markets.

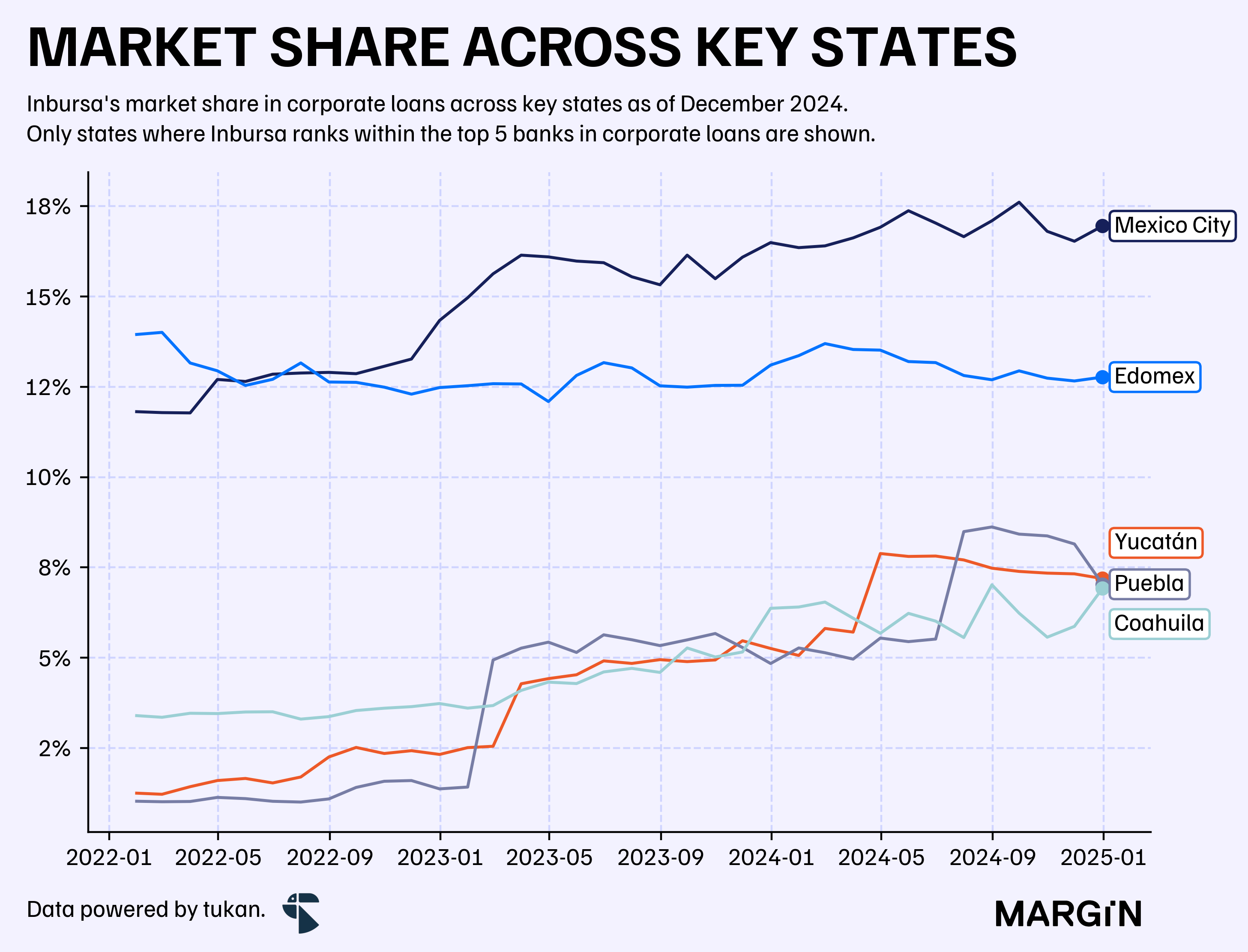

Within the commercial loan portfolio, Inbursa ranked as the fourth-largest bank in Mexico, with an 8.7% market share — 1.3 percentage points behind Santander. However, it also stood as the second-largest corporate lender in Mexico City and the Estado de México, two of the country’s largest corporate markets.

Aside from Mexico City, the company boasts top-5 level rankings in other important states such as: Yucatán, Puebla and Coahuila. Regions, where the bank has gained some considerable market share during the past 3 years.1

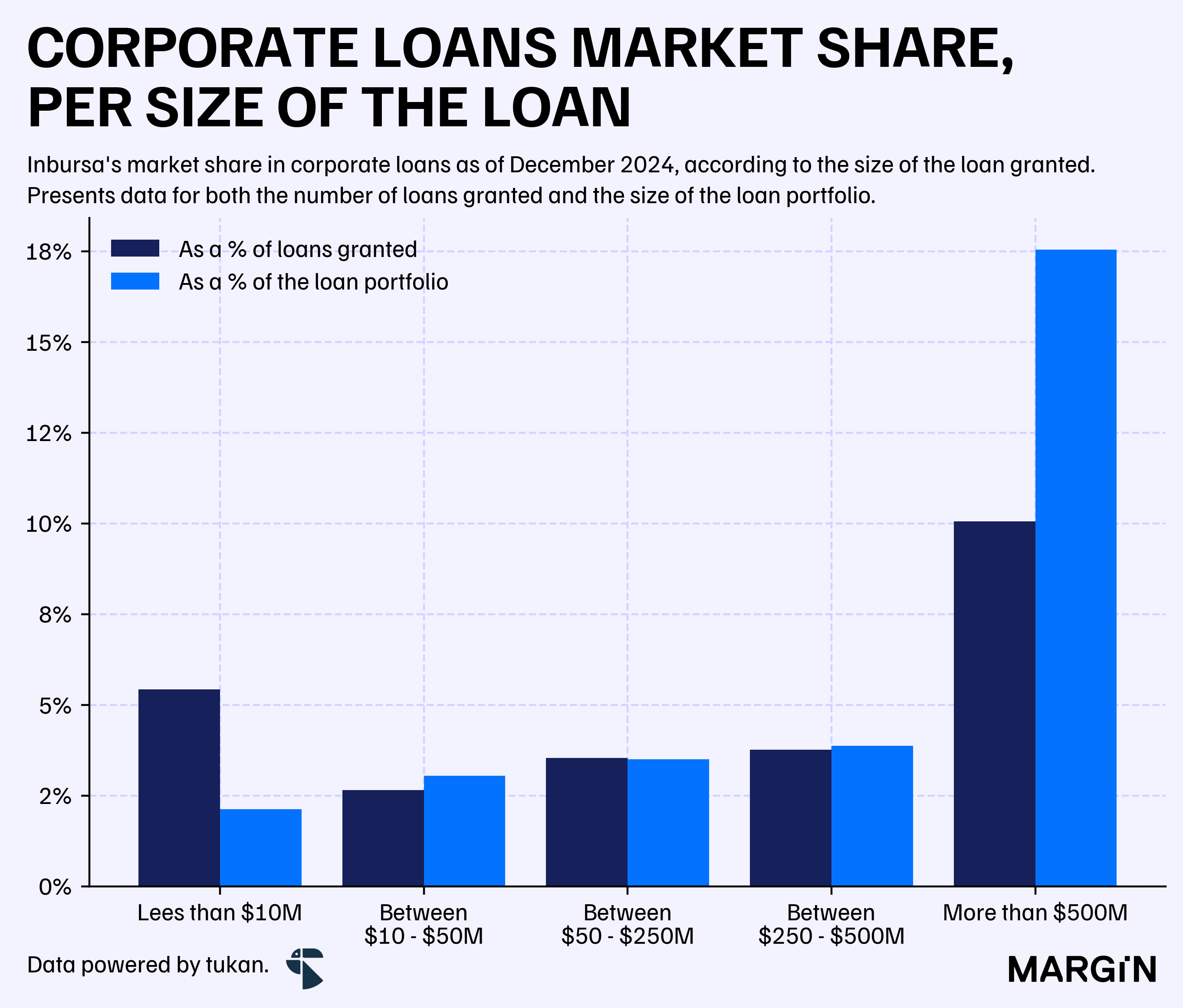

Another key insight into the bank’s specialized approach is its emphasis on larger corporate loans.

In terms of number of loans, Inbursa held a bit over 5% of corporate credits below $250 million pesos nationwide, yet captured a 10% share of loans above the $500 million peso mark. Meanwhile, looking at total portfolio value, the bank’s share was just 3% for loans under $250 million pesos but rose above 17% for those exceeding $500 million.

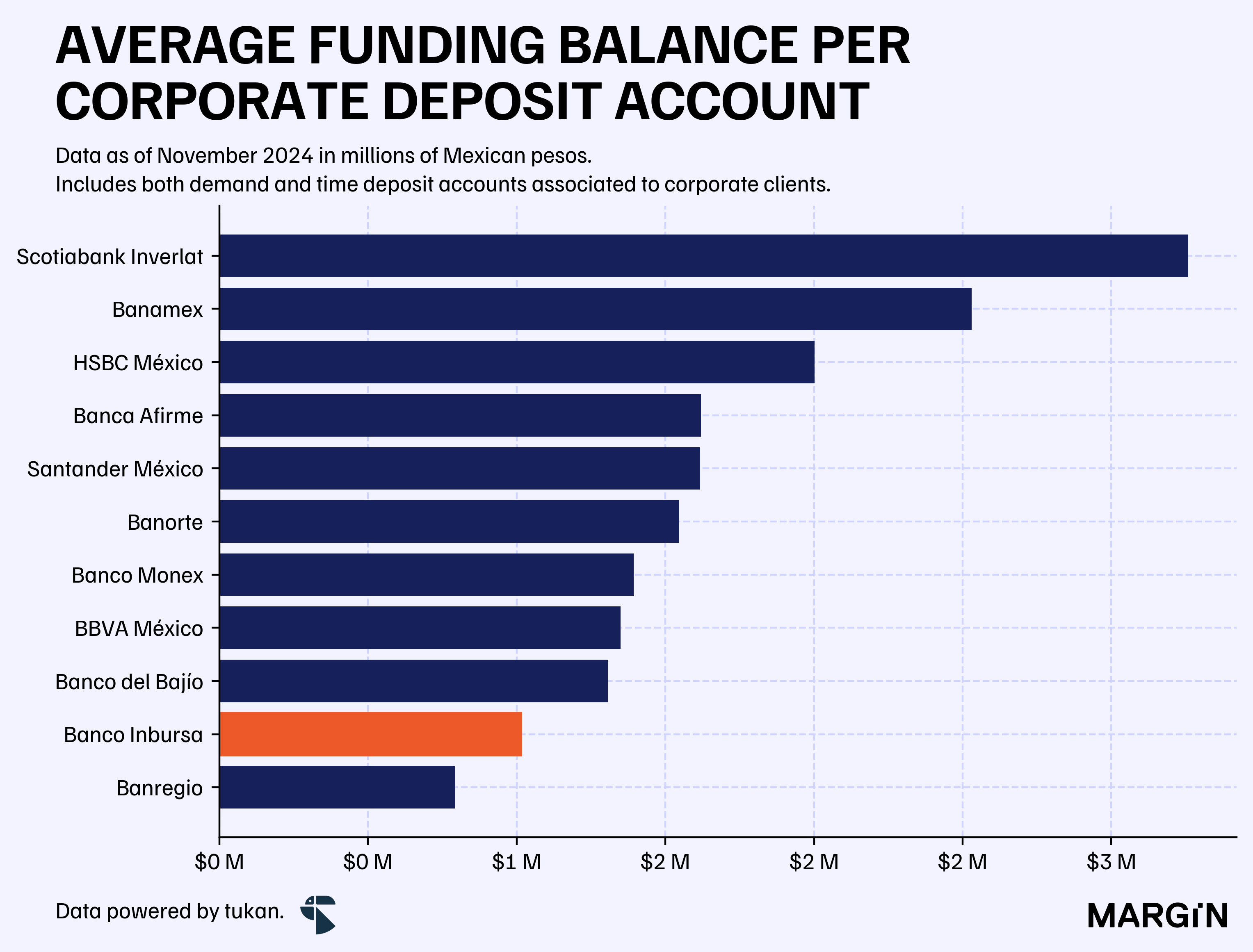

This however, hasn’t translated into a strong presence across corporate deposits. As of November of last year, Inbursa held only 1% of total corporate deposit balances across commercial banks2 — plus, they also reported below average deposits per account when compared to their main competitors.

Accounts from the general public, however, would perform slightly better, with the bank holding a 7.2% share in funds from both transactional and time deposit accounts — a rate 2 percentage points higher than 6 years ago.

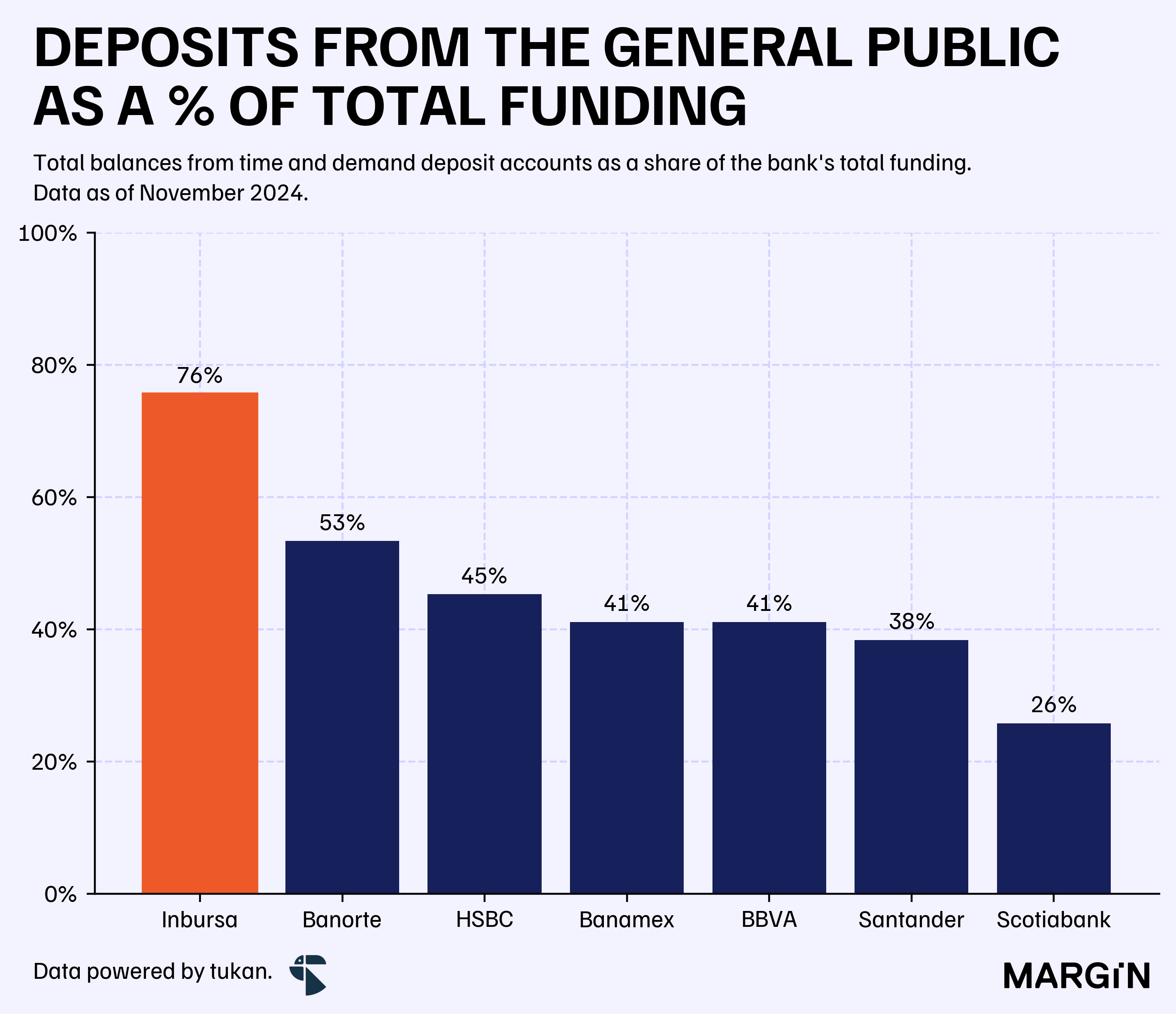

As of the latest available data, most of Inbursa’s deposit funds would come from accounts owned by the general public (88%), the largest dependency on open market funds across G7 banks.

Now that fintechs with high yields are becoming a relevant player in this space, it’s worth noting that Inbursa has always offered above market returns on demand deposit accounts to the general public; albeit, with a minimum balance of $40,000 pesos.

Strangely, it’s something they never seemed to promote aggressively to the market.

Despite traditionally being known as a wholesale bank (i.e. focused on corporates), Inbursa has, on occasion, shown intent to grow its presence in the retail market. Just last year, the company acquired an 80% stake in Cetelem, the fourth-largest financial institution in the auto loans segment.

This acquisition took Inbursa’s share in the country’s consumer loan portfolio to 4.5% at the end of last year — up 2.5 percentage points from the end of 20223 , and raised the company’s exposure to the retail market to 19% (up more than 10 percentage points YoY).

Organically, however, the bank’s efforts to grow its consumer portfolio haven’t been the most promising.

Prior to the acquisition, only the company’s payroll loan portfolio had a higher balance than it did in 2020.

So what exactly makes this bank so operationally efficient?

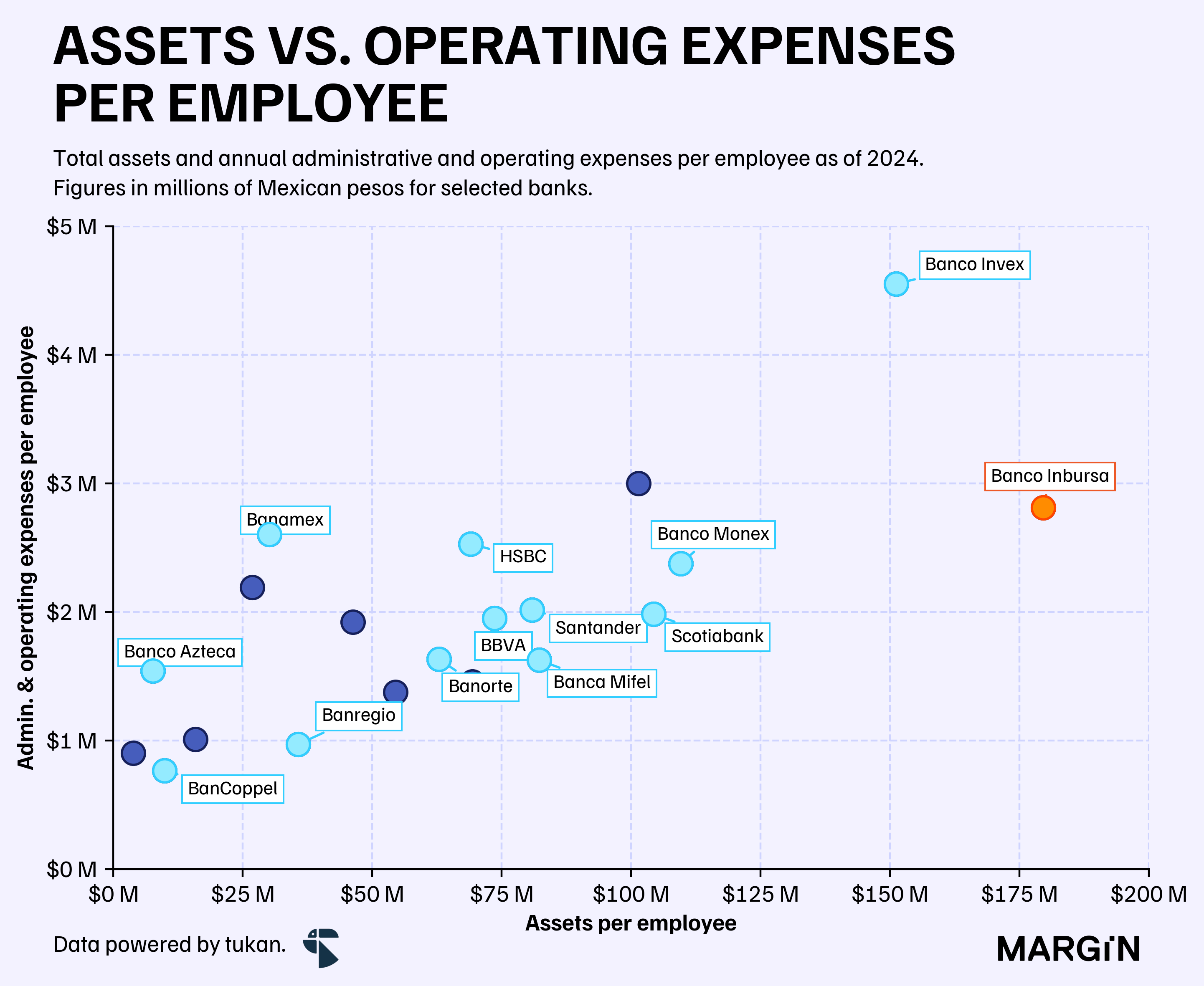

For starters, it maintains a considerably lower headcount than its peers. According to regulatory data, Banco Inbursa employed just over 3,000 people at the end of December (and over 10,000 across the holding).

Oversimplifying things this would mean that an average Inbursa employee manages $180 million pesos in assets for the bank — a ratio 3 times higher than the aggregate commercial banking system and more than 7 times the ratio reported by Banamex (one of the banks with the worst efficiency ratios in the country).

And even though their expenses per employee would be higher than those reported by the market, it would be at a considerably lower basis.

On the retail side, Inbursa’s ongoing expansion remains tentative. Although the Cetelem acquisition signals a commitment to consumer lending, the degree to which this will also translate into meaningful market share gains across other products is not yet clear. The bank may need to reconcile its traditional wholesale focus with the demands of retail clients, balancing its financial resources and technological investment carefully.

Investment in digital channels appears to have produced strong results, with digital transactions soaring by more than 90% year over year. The company also announced that nearly all new contracts for the bank were closed digitally during 2024 — a notable shift, considering that in 2022 almost half of the contracts were still being signed in person.

How this will ultimately affect the company’s spending structure remains to be seen. For now, though, the bank certainly holds enviable efficiency metrics.

With the exception of the Estado de México.

Including development banks.

The previous market share is considering consumer loan portfolios for commercial and development banks, SOFIPOs, SOCAPs, and regulated SOFOMs.

Sería interesante abrir el caso de Banamex ya que el deterioro de su eficiencia podría deberse principalmente a sus costos por la separación de Citi, no en todo el periodo de tiempo se mantiene como el peor en eficiencia.