Monday, On the Margin

Manufacturing; IMMEX; tequila; Mexican stock exchange; SOFIPOs; SPEI and pension funds.

Idle

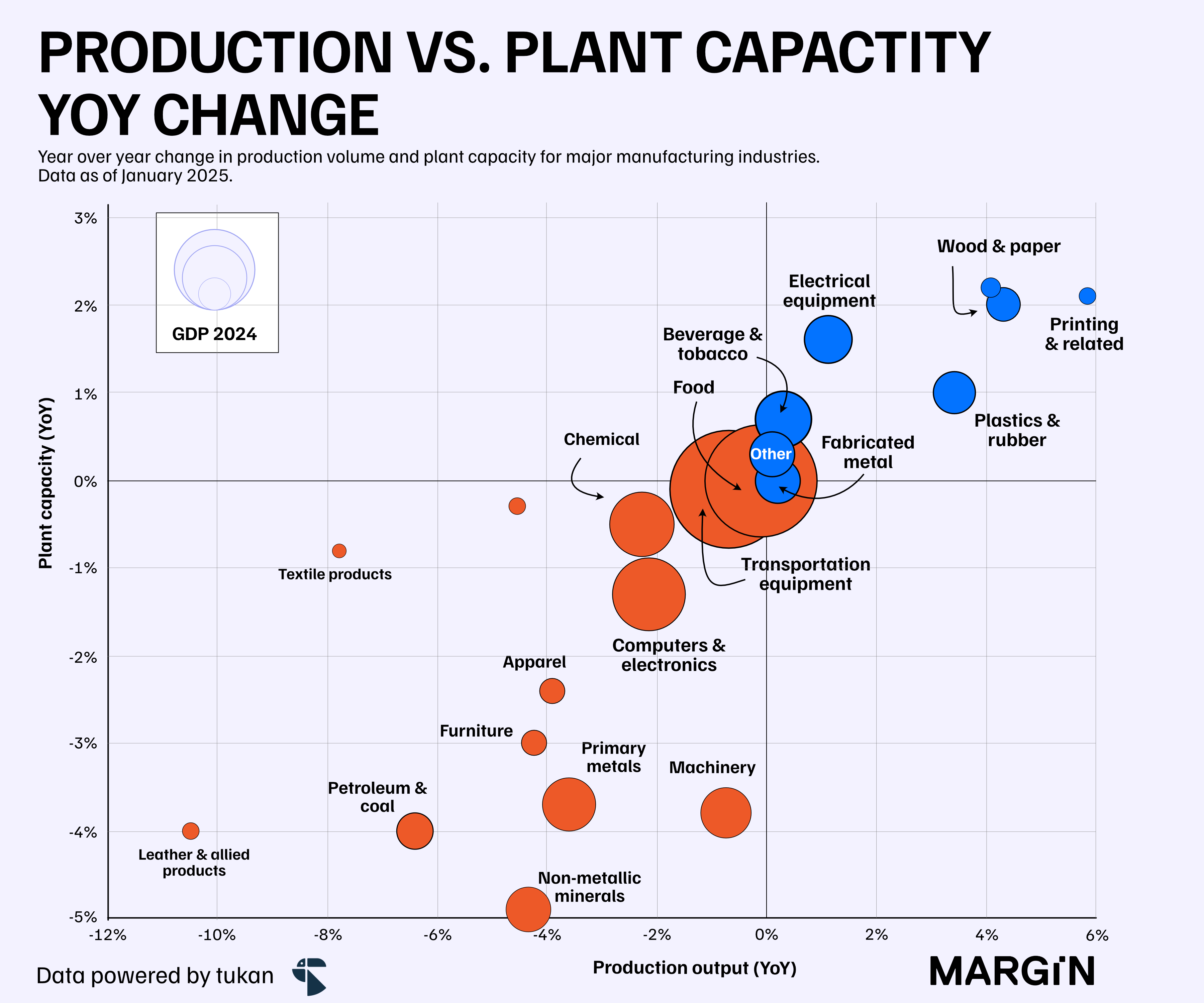

Growth across Mexico’s manufacturing industry is beginning to stall. Last week, INEGI’s manufacturing survey reported a 0.4% month-over-month (MoM) contraction in production volume for January, adding to the decline recorded at the end of December 2024 (-1.7%)1.

On an annual and seasonally adjusted basis, the shrinkage in production was even more pronounced, at a 1.9% YoY contraction for the month. Employment also declined by 1.1% YoY and has now recorded 23 consecutive months of annual decreases.

The negative result at the beginning of this year was primarily due to declines in key industries such as transportation equipment and computer manufacturing, which together account for nearly one-third of the manufacturing GDP and more than half of last year’s manufacturing exports.

January’s data showed decline or unchanged production volumes for most major industries on a YoY comparison.

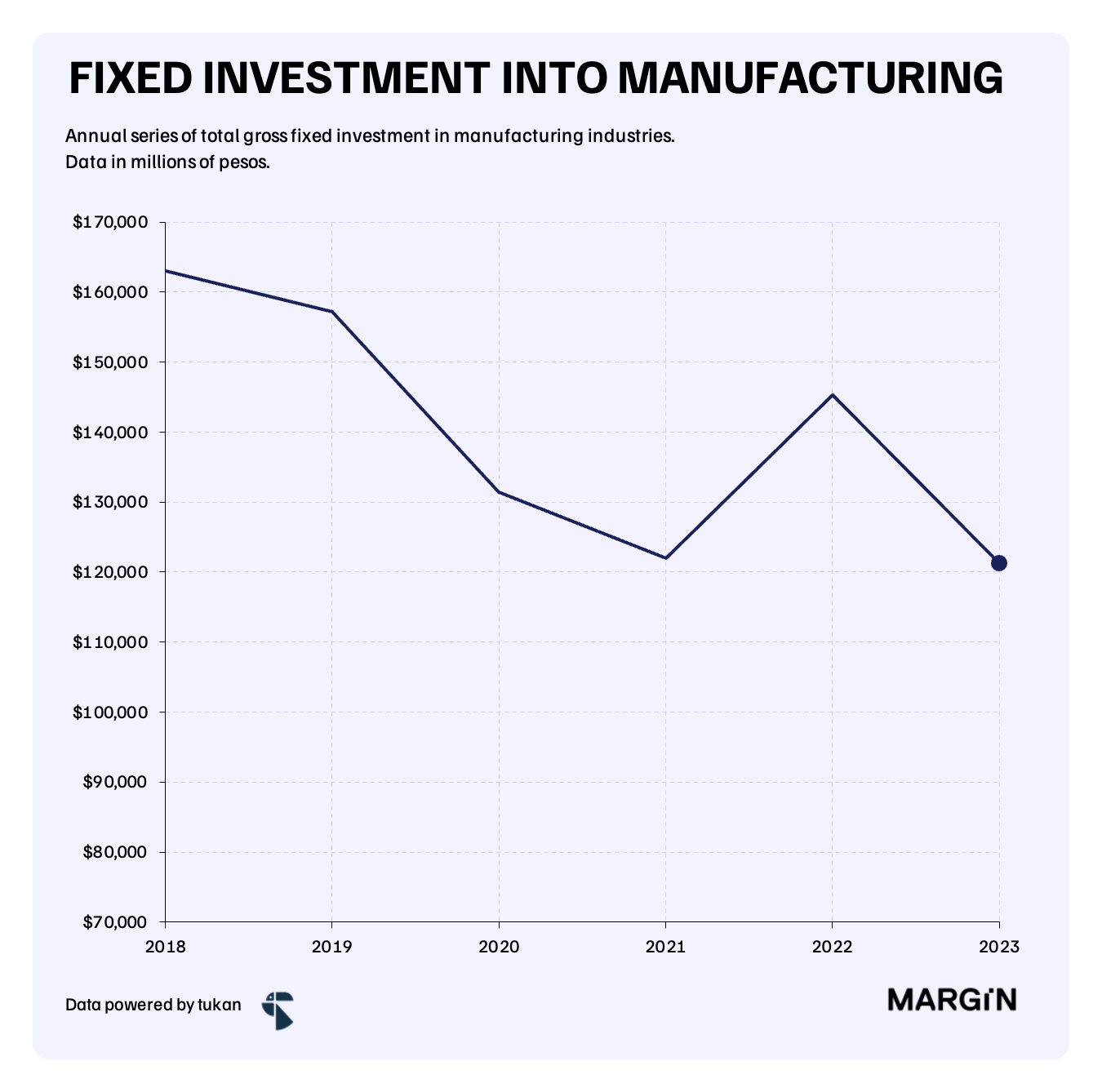

Despite a rebound in 2022, investment in fixed assets by the manufacturing industry decreased by 17% during 2023 and came in 26% below levels of investment recorded in 2018.

Taking into account the declines seen in the monthly fixed investment index computed by INEGI, it is likely we will see another decline in 2024 when INEGI publishes annual figures for the manufacturing industry.

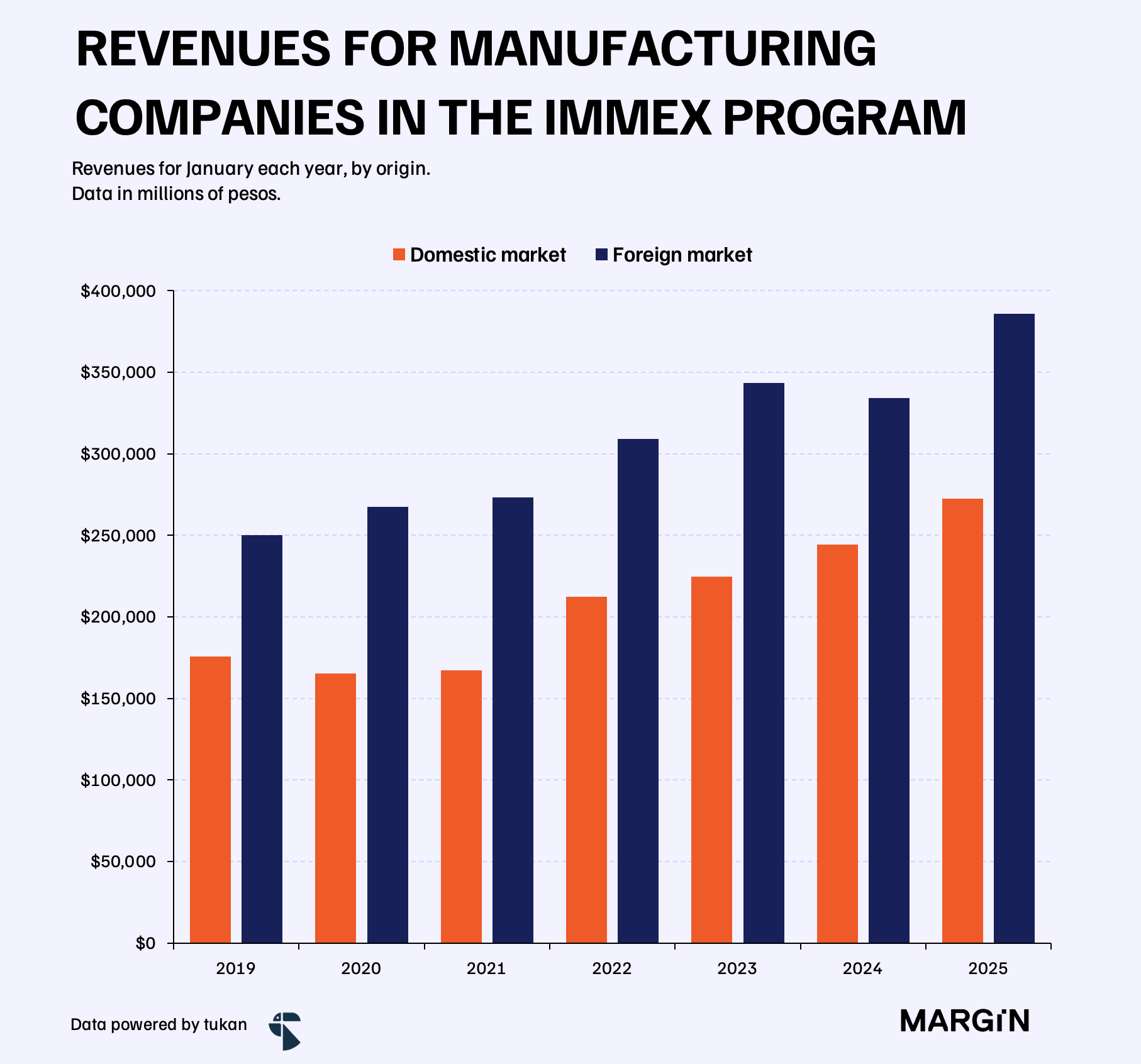

On the bright side, we saw companies participating in the IMMEX program reporting a 14% year-over-year revenue increase in January, totaling nearly $6.6 billion pesos—a record high for the first month of the year.

The main boost came from the international market, with revenues increasing by 16% YoY, compared to a 12% increase from the domestic market.

It is possible that this boost was a result of U.S. companies anticipating tariffs, and therefore advancing purchases from Mexican exporters.

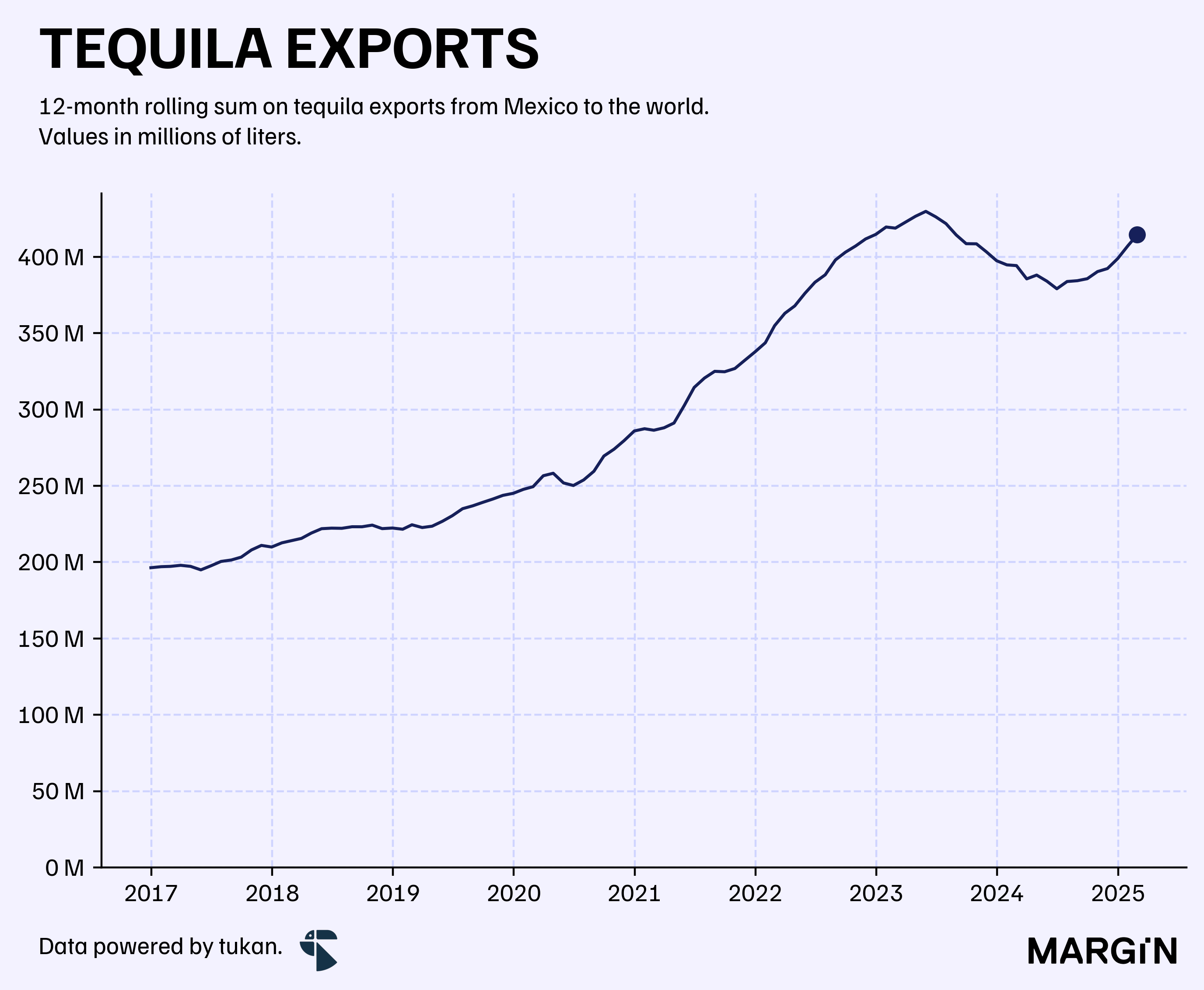

Tequila

Tequila exports surpassed the 38.5 million mark during February, growing by more than 5% YoY.

During 2023 tequila exports declined by more than 4% YoY. However, since mid-2024 export volumes have started to recover significantly for the industry.

BMV

Total value traded in equities through the Mexican Stock Exchange reached more than $381 billion pesos during February, representing a 25% increase versus the same period in 2024.

Trading in global equities (SIC) increased by more than 38% YoY, followed by a 17% expansion on the value traded in the market’s local equities.

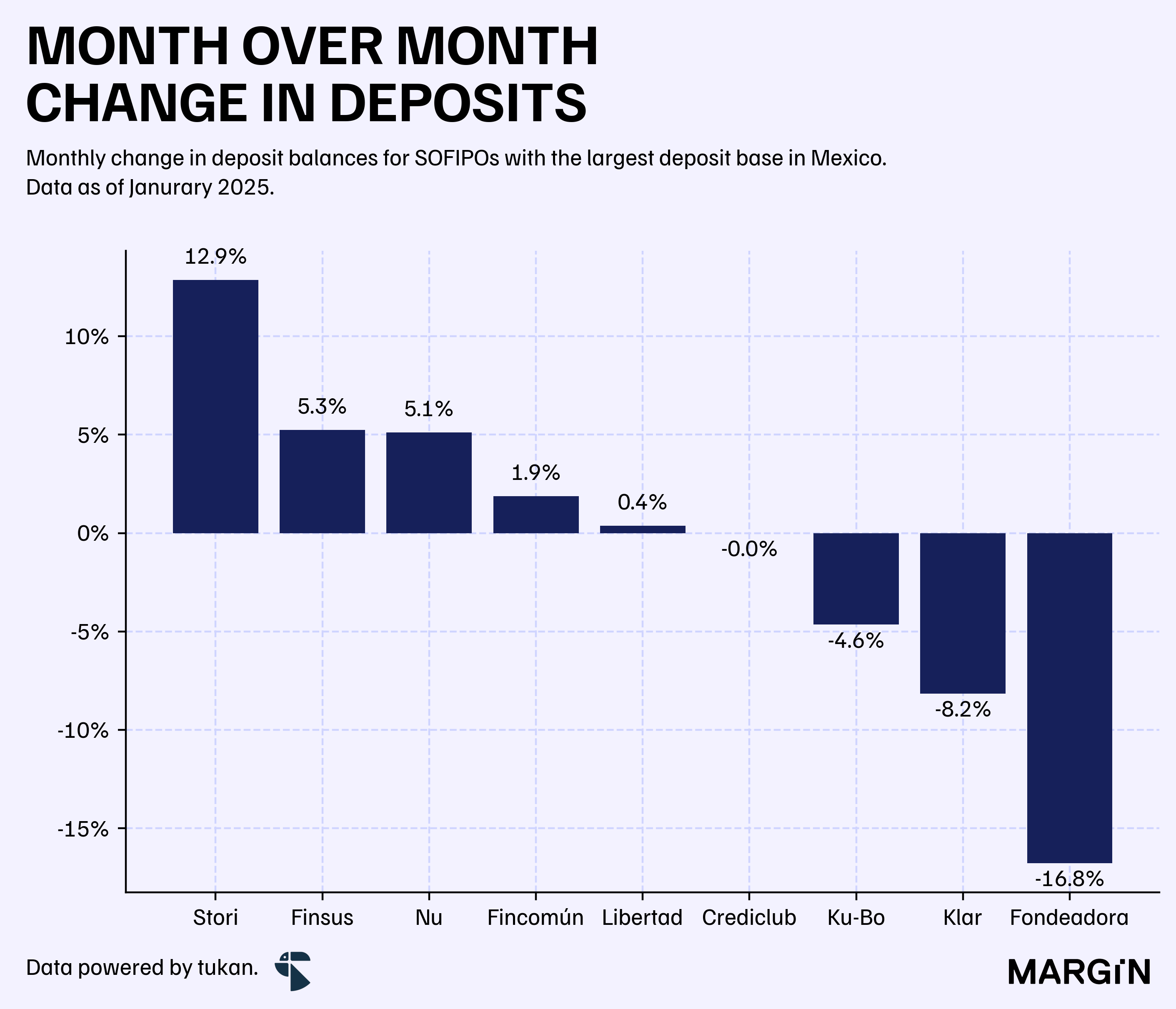

SOFIPOs

Deposits for SOFIPOs grew by 2% MoM during January and they now hold more than $154 billion pesos in traditional funding resources.

Results were mixed for the major players operating in the space — with Stori leading the growth race at 13% MoM, followed by Finsus and Nu at 5% MoM. On the other hand, Fondeadora, Klar and Kubo all posted declines when compared to their December balances.

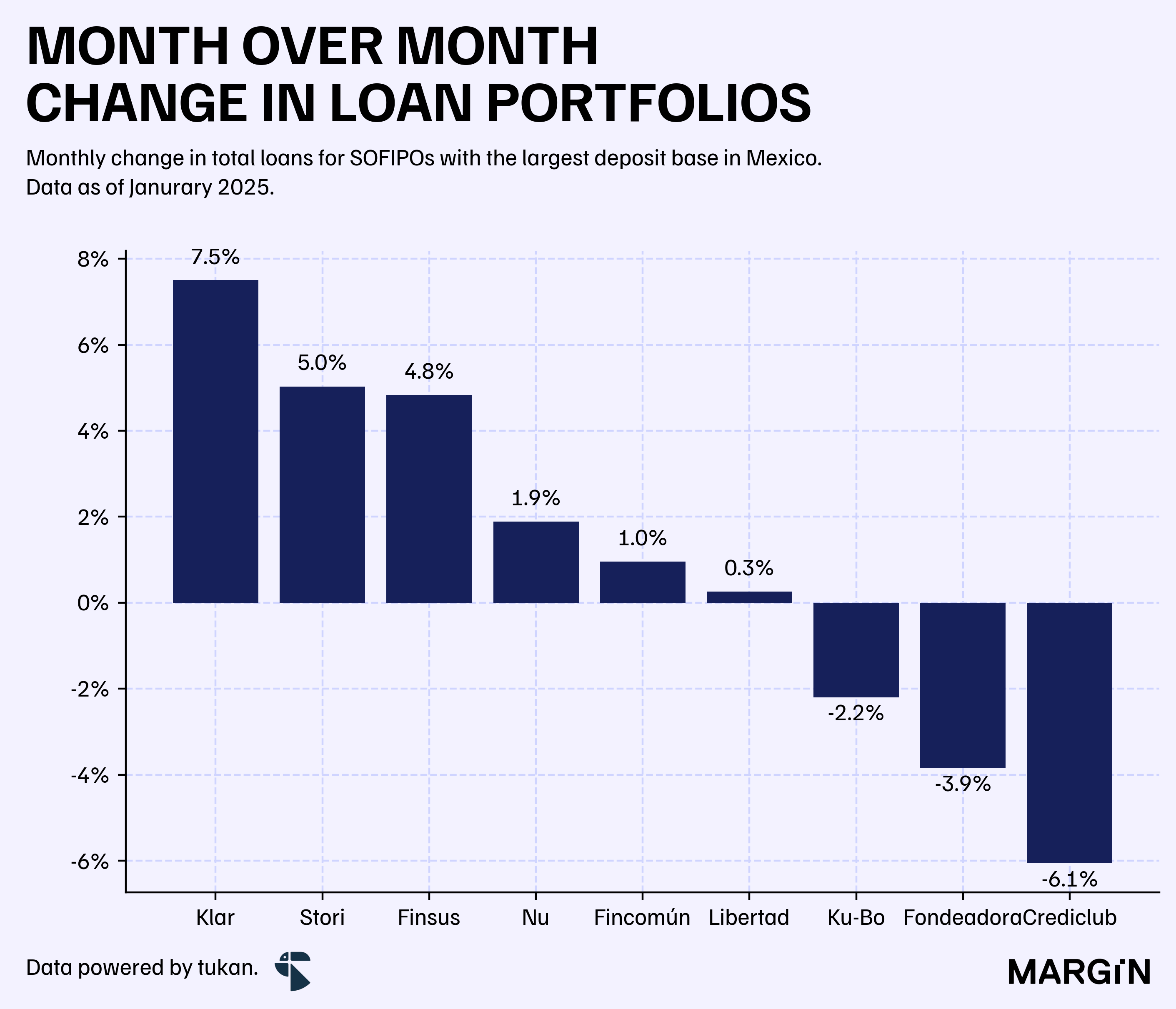

Loan portfolios also posted a mixed bag of results, with total loans closing the month of January with a balance of $64 billion pesos — down 0.7% MoM.

In this case, Klar, which recorded an 8% drop in deposits had the largest growth rate with a 7% rise in total loans.

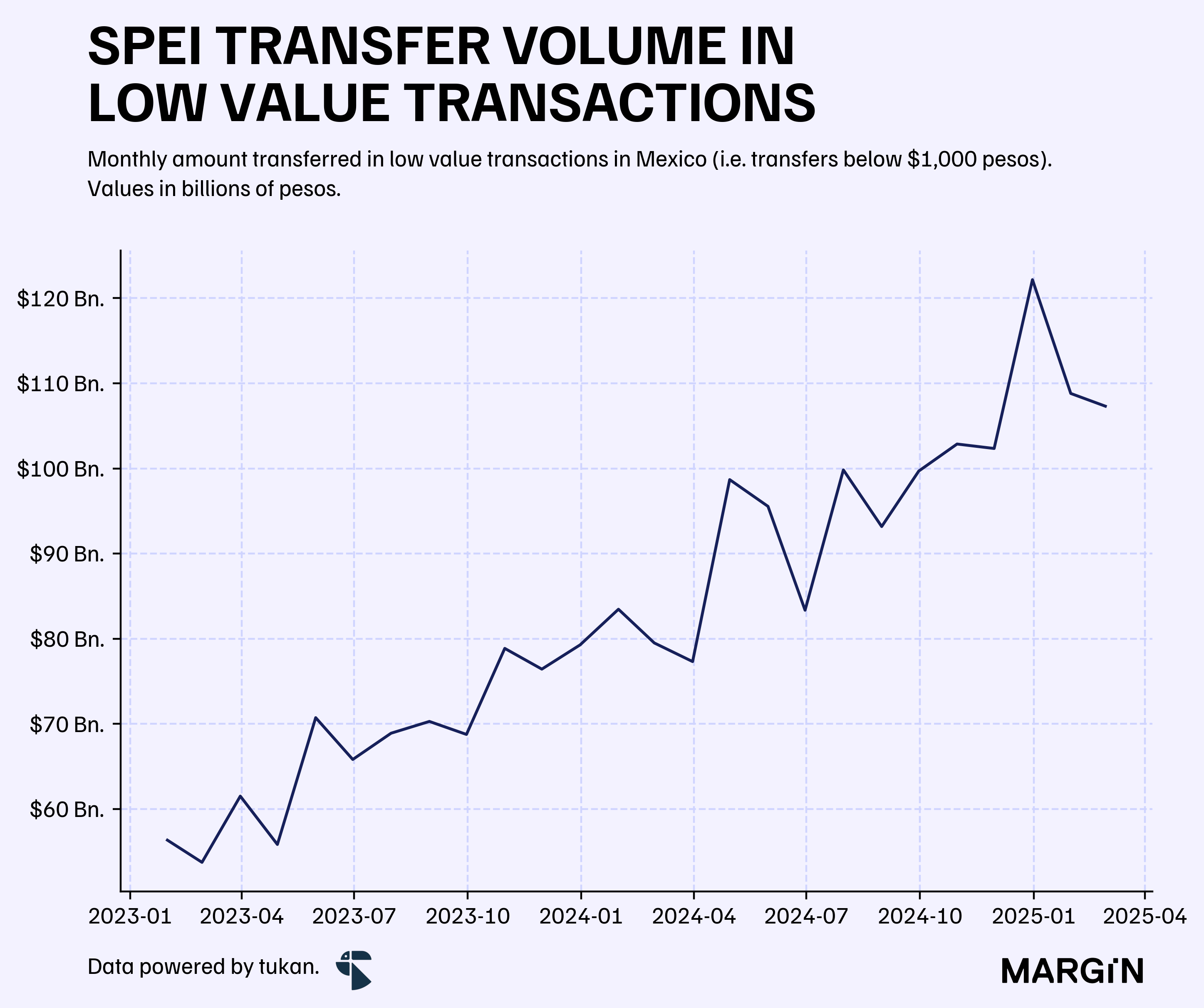

SPEI

Low value transfers (below $1,000 pesos) in SPEI amounted to $107 billion pesos during February — implying a 35% growth rate YoY.

This marks the 5th consecutive month where low-value transfers in SPEI exceed the $100 billion peso mark.

If you’re interested in SPEI data, we published a deep dive on the topic a couple of months ago.

Pension funds

Mexican Afores began 2025 on an upward trend. In February, they held over $7.1 trillion pesos in net assets, an 18% increase compared to the same month in 2024.

Growth was even more pronounced in institutions like Profuturo and Sura, with a year-over-year rate of about 22%. In contrast, Banorte's Siglo XXI grew at a slower-than-average pace of 14% YoY.

If you’re interested in learning how pension funds make money, we did an introduction to this a while back.

Based on seasonally adjusted data.