Monday, On the Margin

Banorte; Nu; SOFIPOs; Liverpool; IGAE; inflation; trade.

Banorte

Banorte’s first quarter results showed an 8% annual increase in net income, taking the financial holding’s profits to over $15 billion pesos during the first three months of 2025.

According to February CNBV data, Banorte won 27 basis points (bps) of market share in loans against other commercial banks in the country — with important gains in the commercial portfolio (+58 bps)1, credit card loans (+49 bps) and payroll loans (+32 bps) on a year-over-year comparison.

Overall, market share in consumer loans contracted by 11 bps, mainly as a result of Inbursa’s acquisition of Cetelem — one of the largest non-bank players in the auto market.

Despite solid results across key areas, the poor performance of Bineo — Banorte’s digital bank — puts in question the subsidiary’s role as a strategic endeavor going forward.

During the past 12 months2, Bineo has spent over $1.5 billion pesos in non-financial expenses, a figure equivalent to 47 times its average loan book — for context, fintechs like Fondeadora and Ualá would have non-financial expenses in the range of 1.4 and 2.0 times the size of their respective loan portfolios.

Nu

On the other hand, Nu México received authorization by the CNBV to operate as a commercial bank.

We believe the company’s primary focus will be to target the more than $713 billion pesos currently held in payroll funding accounts in order to try and move its clients up the lending funnel to more profitable products such as: payroll and personal loans.

According to SEC filings, 49% of Nu’s interest income came from personal and payroll loans during the fourth quarter of 2024, despite this product representing just 29% of total loan balances.

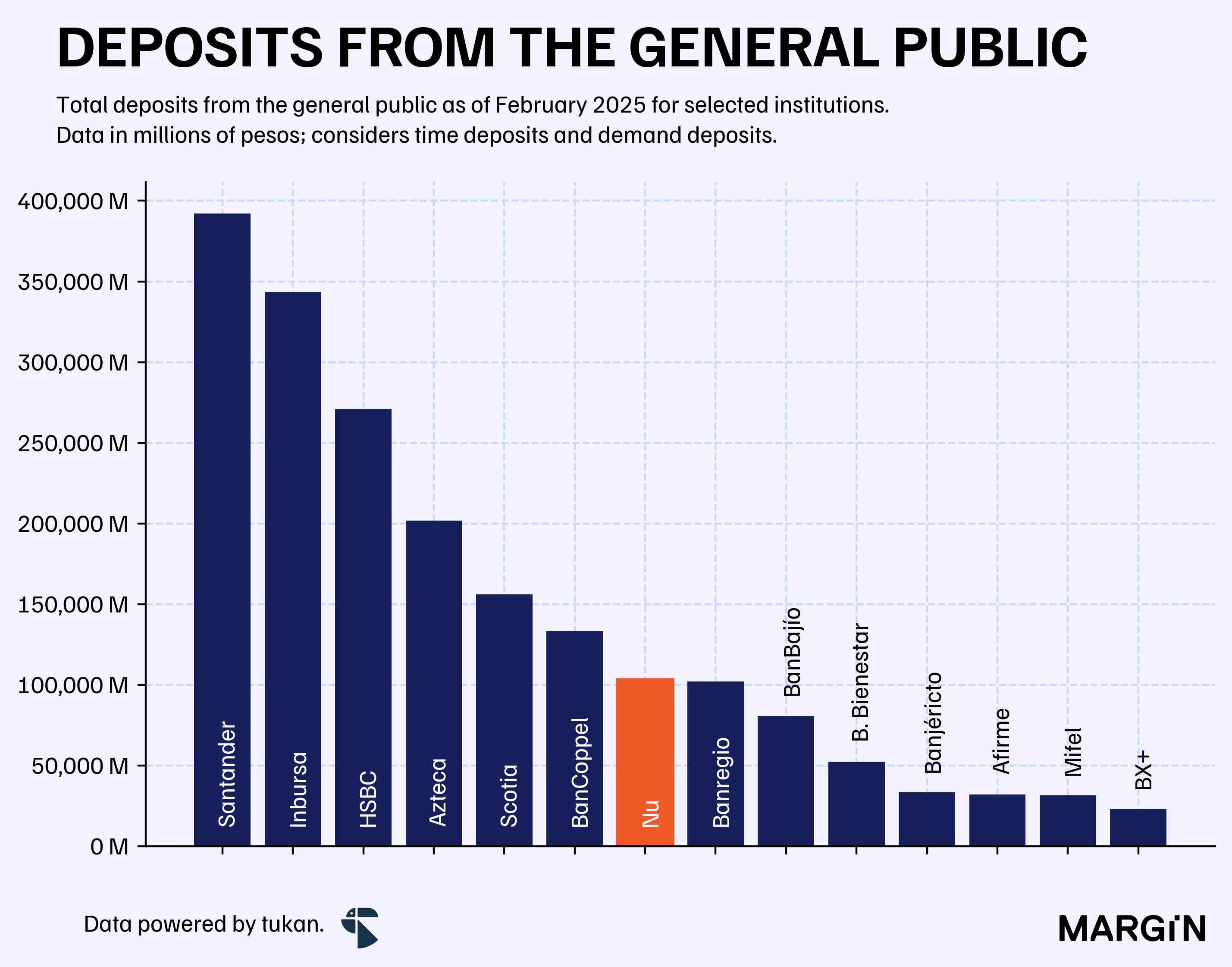

As of February, Nu had deposit balances of over $100 billion pesos — narrowing down on deposit balances from the general public3 against major players such as Scotiabank, HSBC and (surpassing) Banregio.

However, the company’s loan portfolio has struggled to produce a similar growth trajectory with total loans stalling at around $19 billion pesos since October of last year.

SOFIPOs

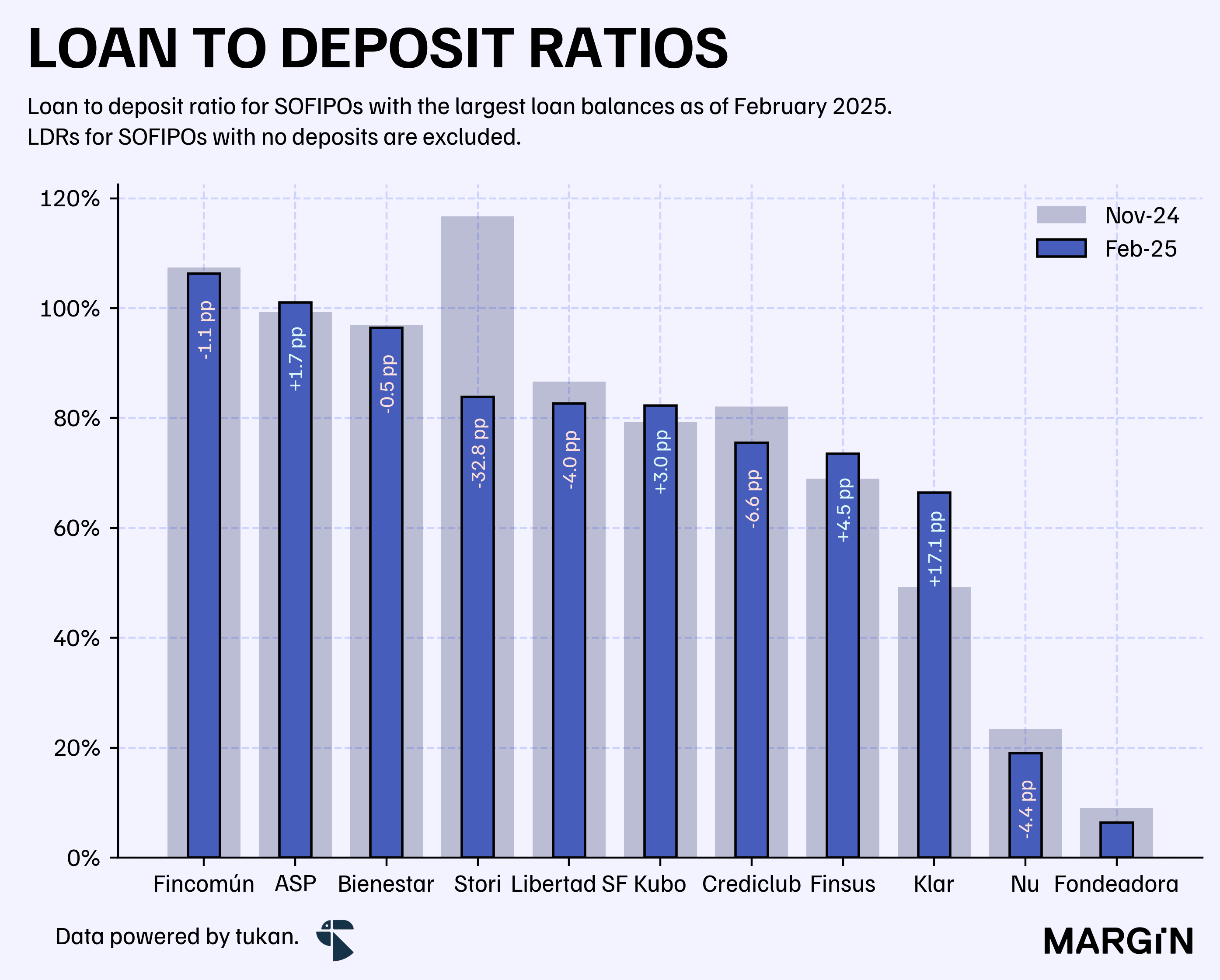

Loan portfolios for other major fintech players operating as SOFIPOs4 stood at almost $27 billion pesos — growing 5% month-over-month.

Loan to deposit ratios on the other hand stood at 85% (excluding Nu); with Klar and Finsus posting the biggest gains in this statistic when compared to 3-month lagged figures.

Liverpool

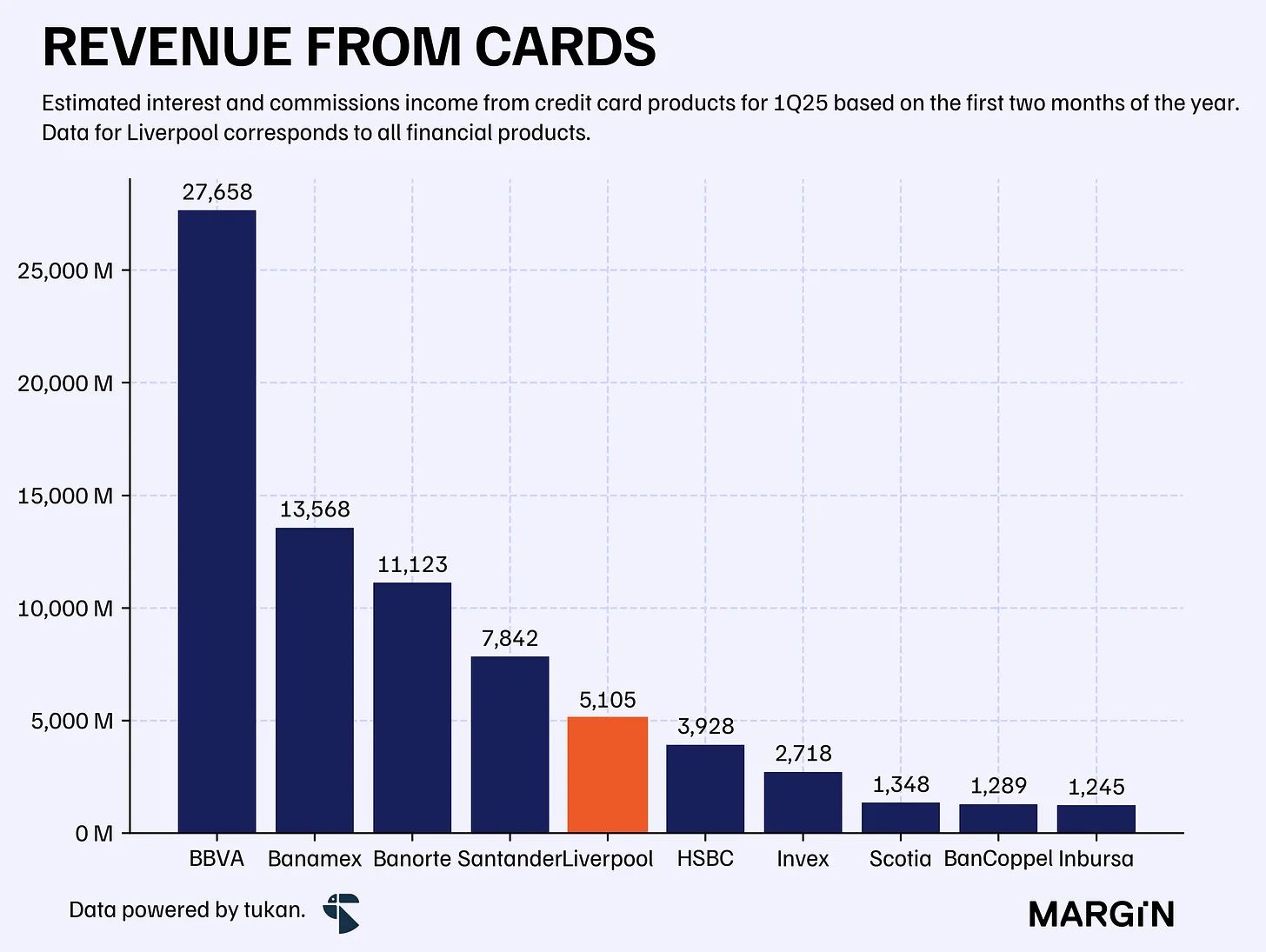

Financial service revenues for El Puerto de Liverpool topped $5 billion pesos during the first quarter of 2025, increasing by 17% YoY (vs. a 10% growth for the company’s other business segments).

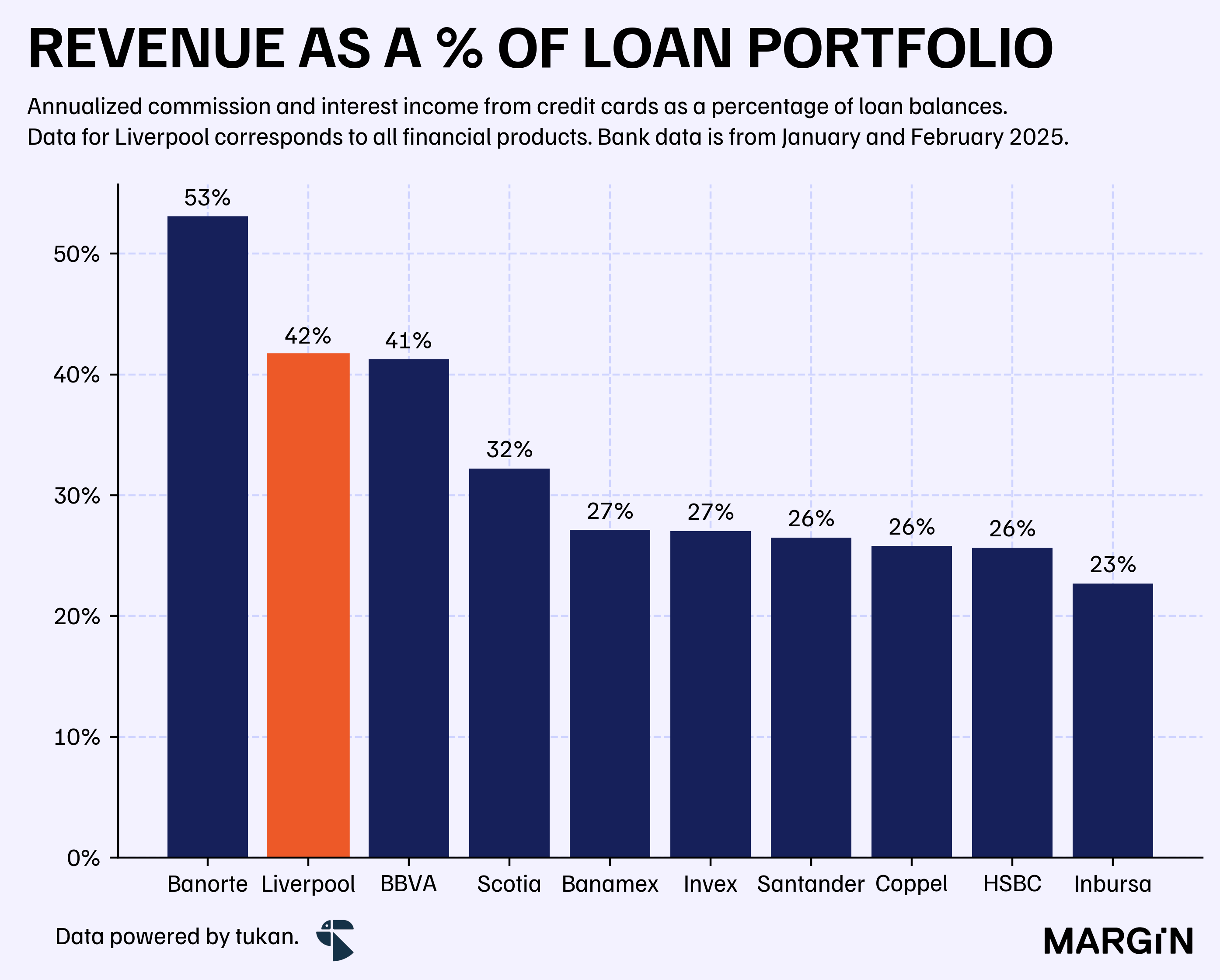

Financial revenues would be equivalent to 42% of the company’s loan portfolio — only BBVA and Banorte would have a ratio in the same range as the retailer.5

According to the company’s latest press release, the number of cards grew by almost 7.3% YoY — reaching 7.8 million plastics in total. For context, this would make the retail giant the third largest player in the market (in terms of number of cards).6

If you’re interested, we explored Liverpool’s financial business in detail last year.

Economic activity

Mexico’s IGAE index, a proxy for GDP growth, grew by 1% MoM on a seasonally adjusted basis against during the month of February.

According to INEGI, professional services and recreational activities were some of the best performing industries during the month; as they both grew by mid-single digits against January’s figures.

Inflation

The annual inflation rate for the first two weeks of April came in at 3.96%.

Households suffered from +4% annual increase in prices across food items and services, an effect slightly offset by the 2% rise in general merchandise products.

This was above consensus’ expectations (3.8% for April) — we think if inflation remains too close to the 4% mark, it could pause Banxico’s recent cutting spree to the Mexican reference rate. Most analyst’s, however, are expecting we will end 2025 with a reference rate of 7.75% (currently at 9%).

Trade

Retail trade in Mexico grew at an 1.7% pace YoY during the month of February — on a seasonally adjusted basis.

However, non-adjusted figures showcased a 1.1% annual contraction in retail activity; with supermarkets and department stores suffering a 3.3% blow (YoY) on its income figures; according to INEGI estimates.

Driven by an annual expansion of over 38% in loans to non-bank financial companies.

March 2024 to February 2025.

I.e. natural persons (personas físicas).

Finsus, Crediclub, Fondeadora, Kubo, Klar and Stori.

Although Liverpool’s financial business includes revenues and commissions from other financial products (insurance, etc.).

Although most of this cards would be restricted to purchases within Liverpool stores.

Solo una pregunta porque el post no es en español.