Monday, On the Margin

Card data; vehicle sales; industrial activity; inflation; construction costs; trade; government securities.

Rebound

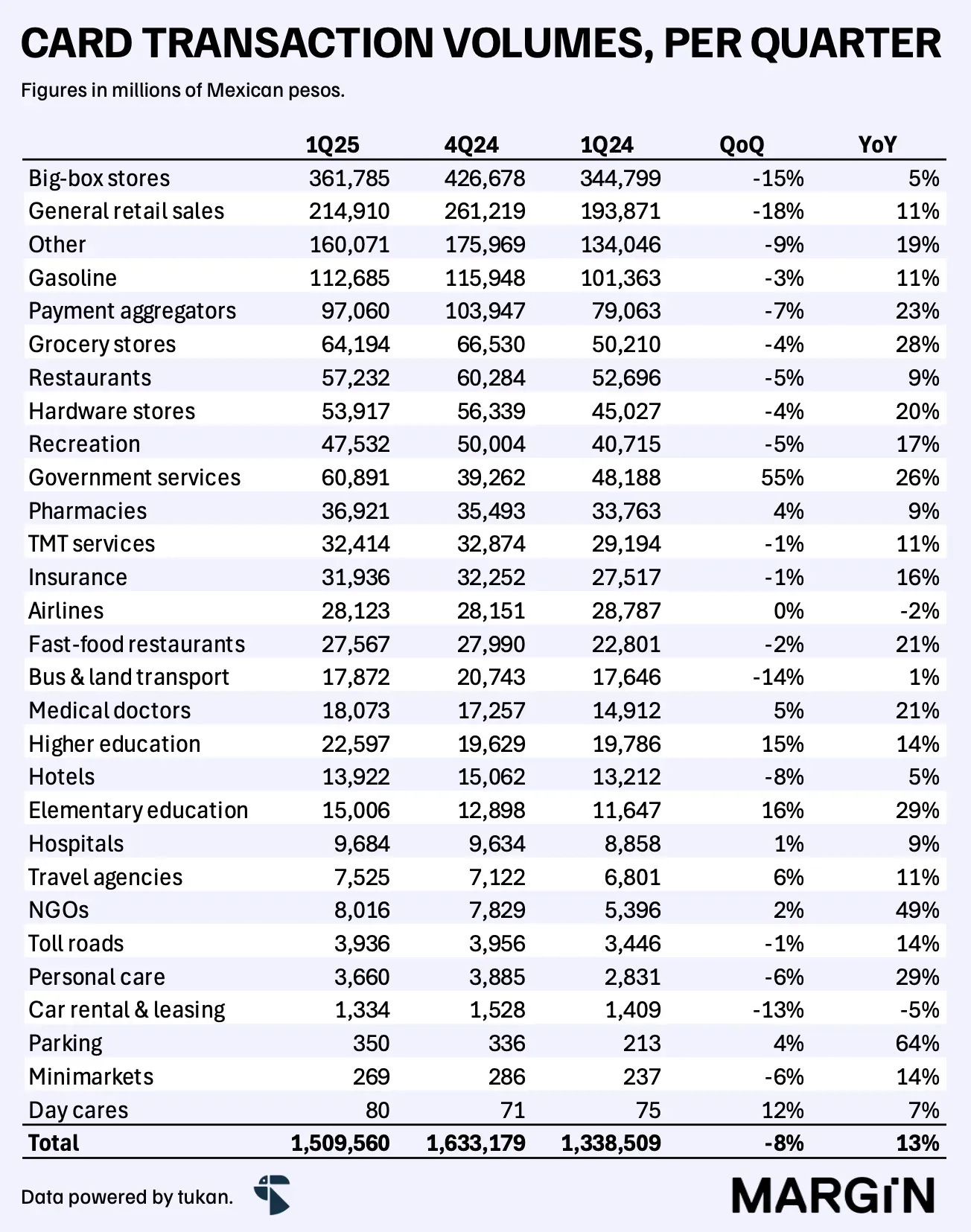

Total card transactions in Mexico for the first quarter of the year came in at 2.6 billion purchases, or 16% YoY (year-over-year). Purchase volumes totaled more than $1.5 trillion pesos — a figure 13% higher than during 1Q24.

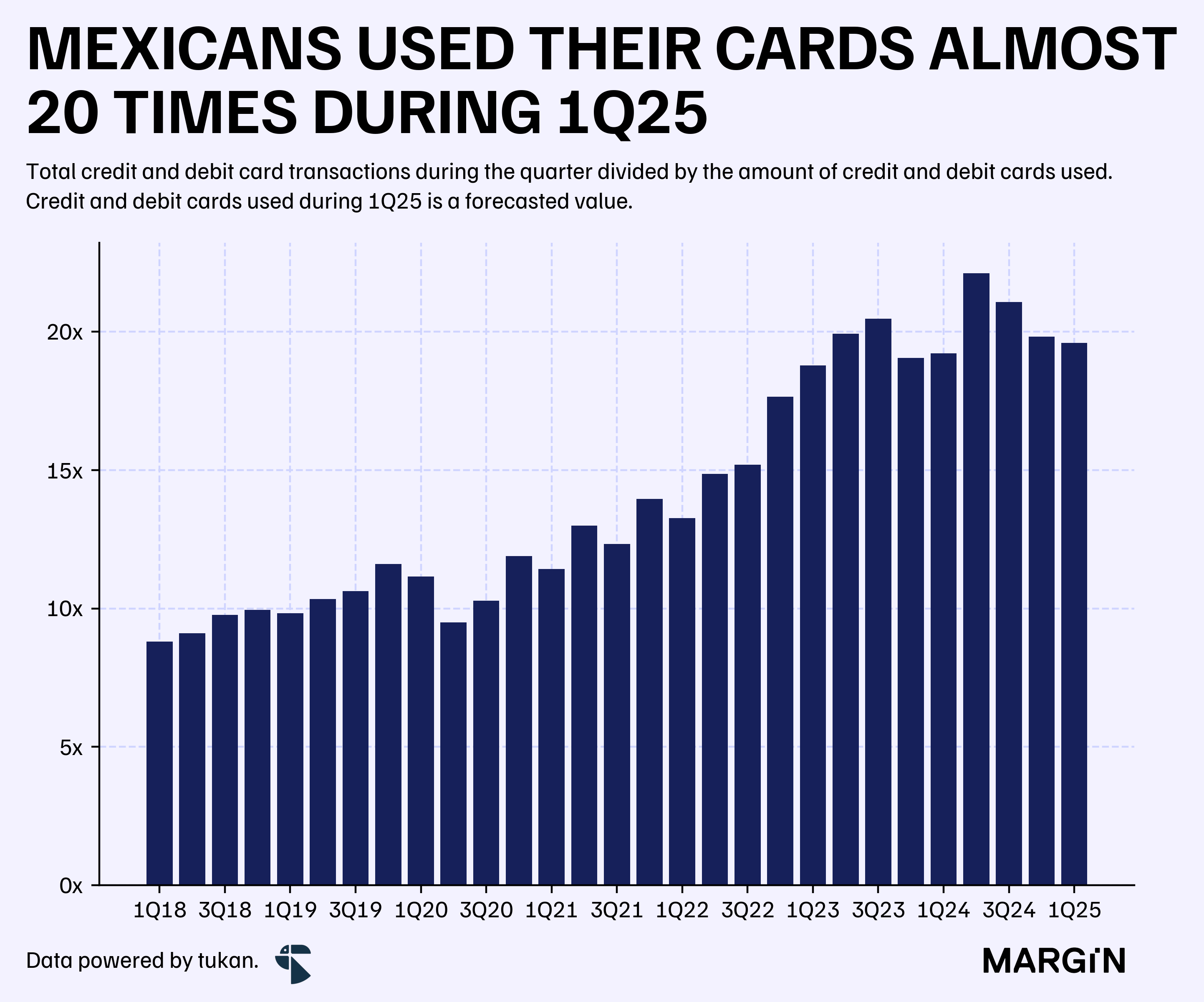

Usage of credit & debit cards remained at an average of 6.5 times per month (i.e. 19 times per quarter) — down 1% QoQ and up 1% YoY.

We eased our concern on consumer spending thanks to an important recovery across purchase volumes in big-box stores, which grew by double-digit rates during the month of March. This comes as a breath of fresh air, after we saw card sales decline for the first time in years during the month of February (-3% YoY).

Airlines, hotels and restaurants faced some deceleration (and even contractions) when compared to previous quarters as annual growth rates for these three “industries” came in at: -2%, 5% and 9%, respectively.

Vehicles

Light vehicle sales came in at 127 thousand new units during the month of March (+1% YoY), and 365 thousand vehicles for 1Q25 (+3% YoY).

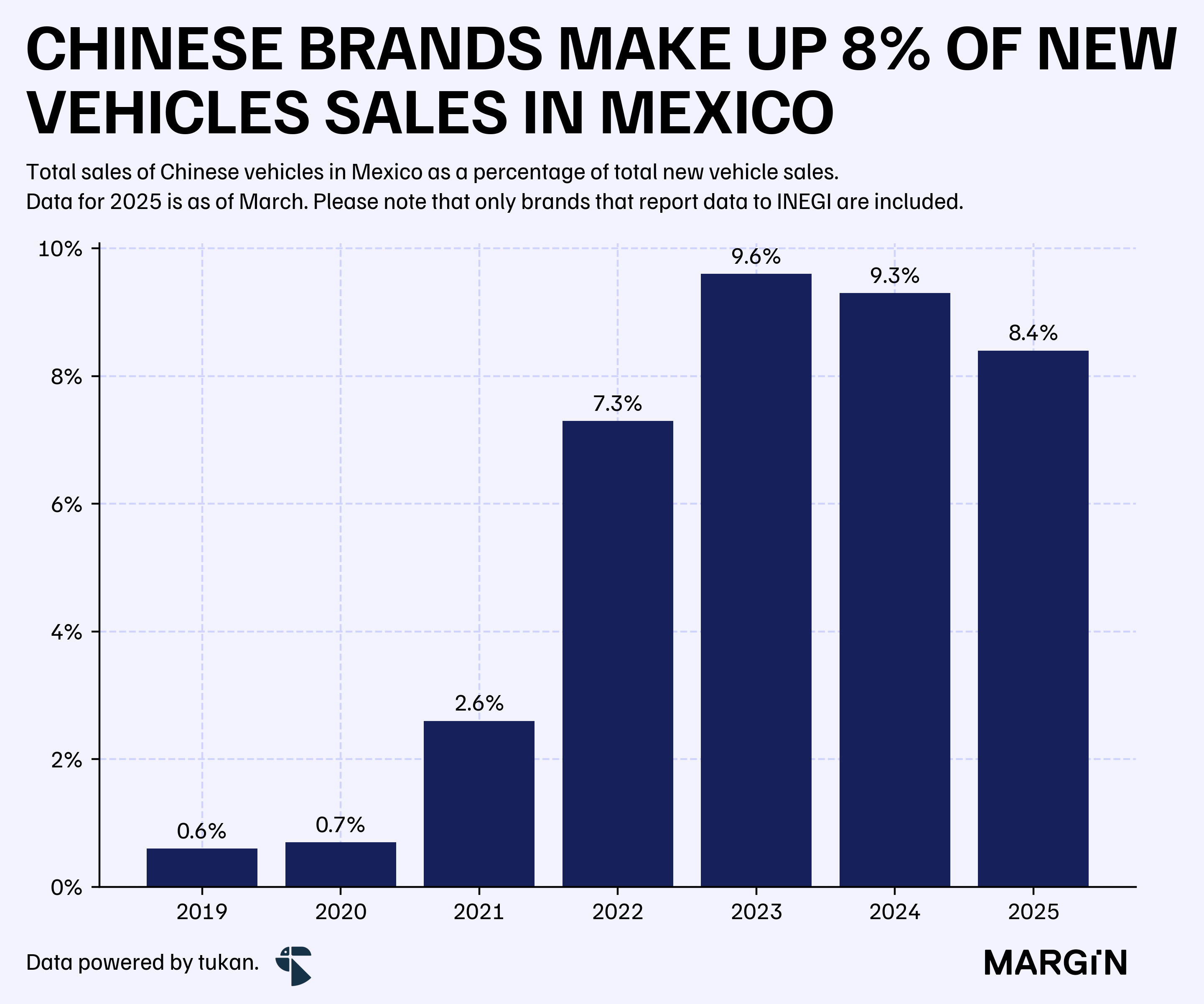

During 2023 and 2024, Chinese brands accounted for a little bit over 9% of total new vehicle sales in Mexico. However, data from the first three months of this year has seen Chinese brands account for just 8.4% of total sales.1

Brands such as MG Motors have contracted sales by over 17% since the start of the year.2

Hybrid and electric vehicle sales increased by over 30% YoY during the first quarter. This took total sales to over 33 thousand units in 1Q25, and marked the second highest figure ever recorded for a single quarter since INEGI publishes data on the subject (13% below 4Q24 sales figures).

Industrial activity

Industrial activity increased by 0.5% during the month of February, mainly propelled by a 1.8% increase in manufacturing and a 0.5% growth in construction.

Mining and utilities both offset growth by declining 6.3% and 1.1%, respectively, on an annual basis.

Inflation

Annual consumer price increases remained below the 4% threshold for the third consecutive month, recording an annual inflation rate of 3.8% in March of this year.

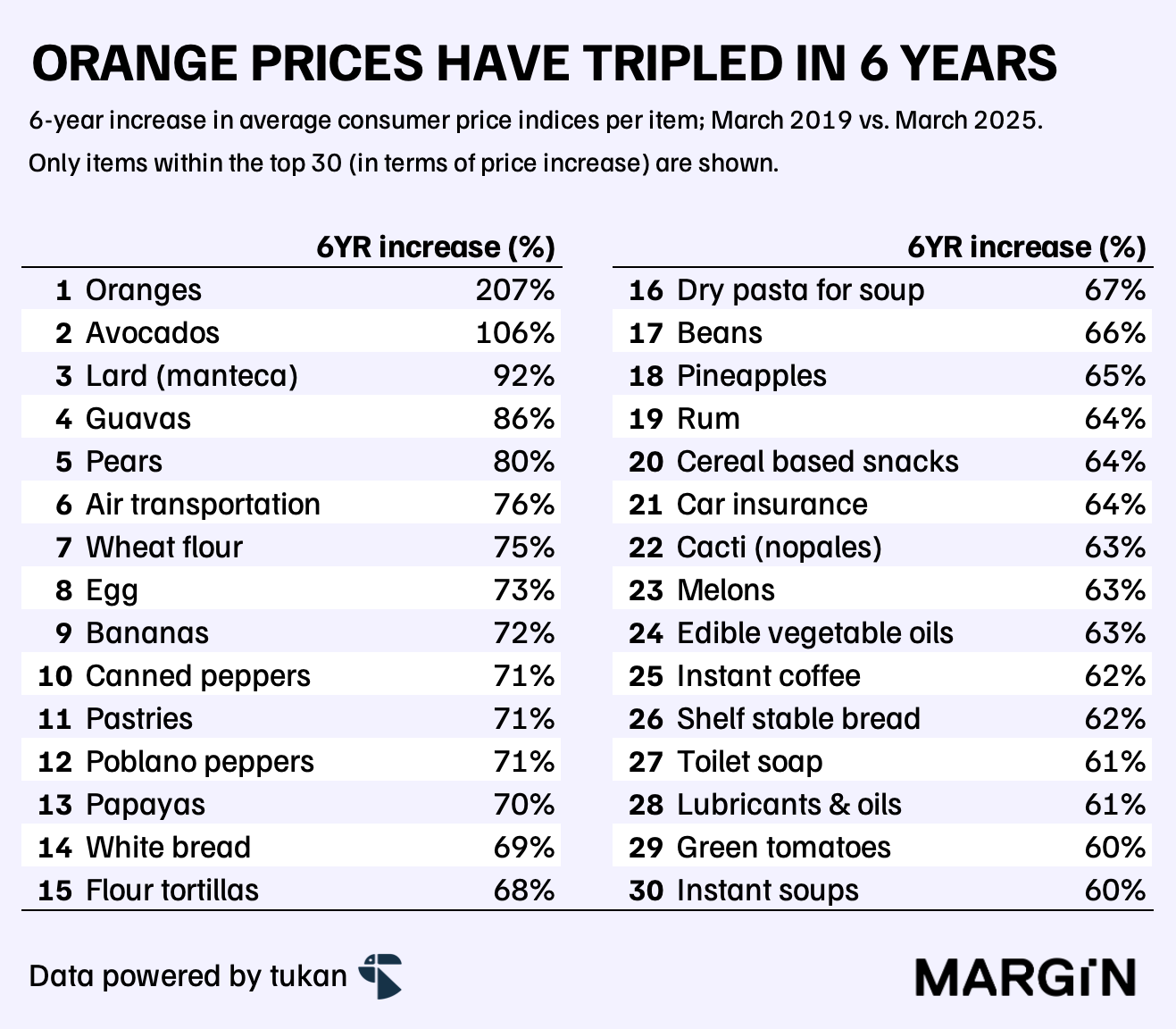

Since 2019, there have been 78 items tracked by INEGI that have suffered an overall increase in prices of over 50% (or a 7% 6-year CAGR) — 16 of these would be fruits & vegetables and 9 would be milk-based products.

Air transportation & car insurance would be the items outside of food with the highest overall price rises.

Despite the uncertain economic environment, the Citi survey on economic expectations has major economists in the country forecasting annual inflation rates of over 3.7% for 2025 (at the median). This forecast has been improving since analysts published a median forecast of 3.9% at the start of this year.

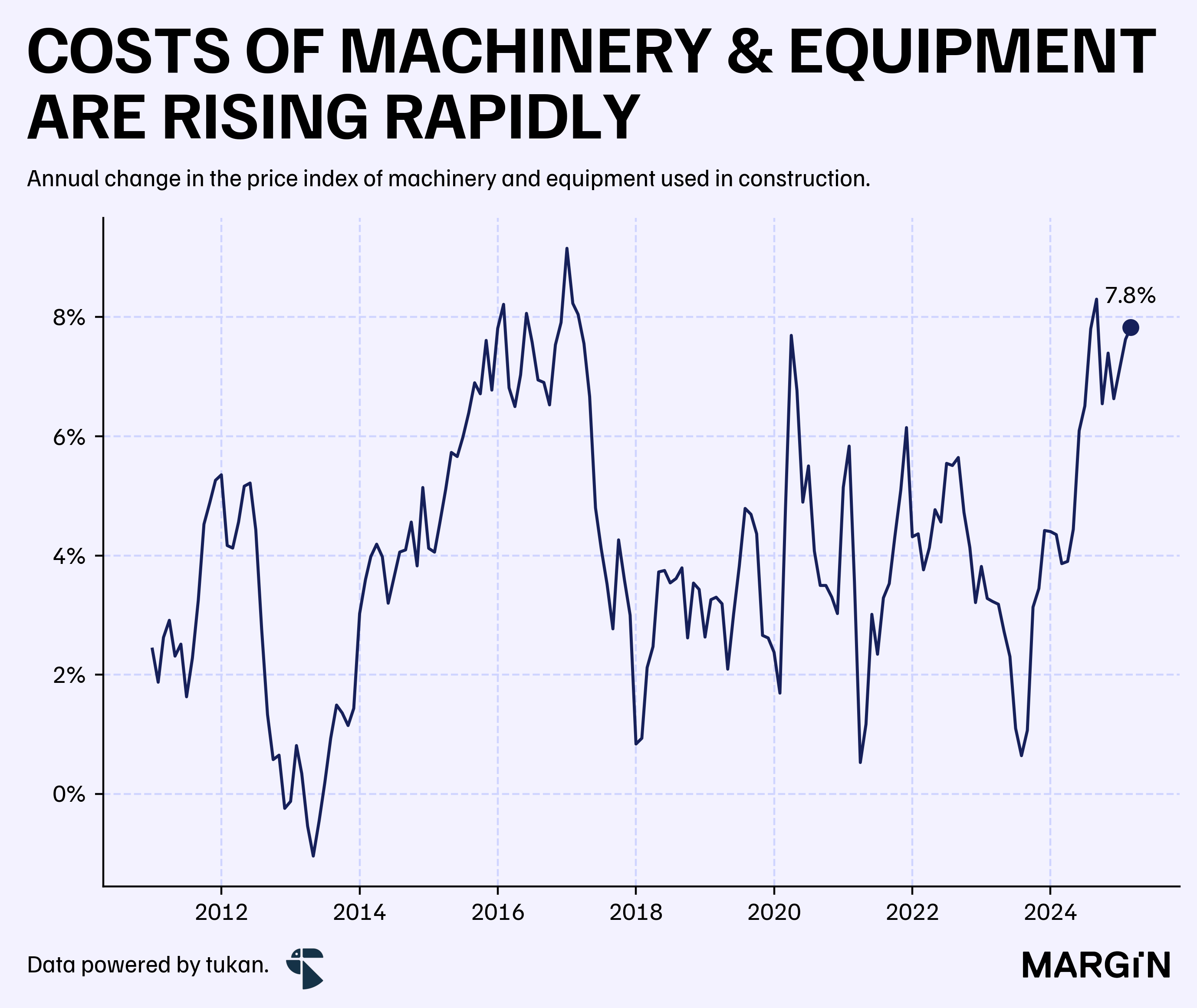

Construction costs

Construction costs rose by 3.7% YoY during the month of March.

According to INEGI, construction companies in Mexico are seeing the cost of leasing machinery and equipment rise at rates not seen since 2016 (+7.8% YoY during March 2025).

The impact from rising costs in machinery and equipment has been partially offset by a deceleration in labor costs and construction materials.

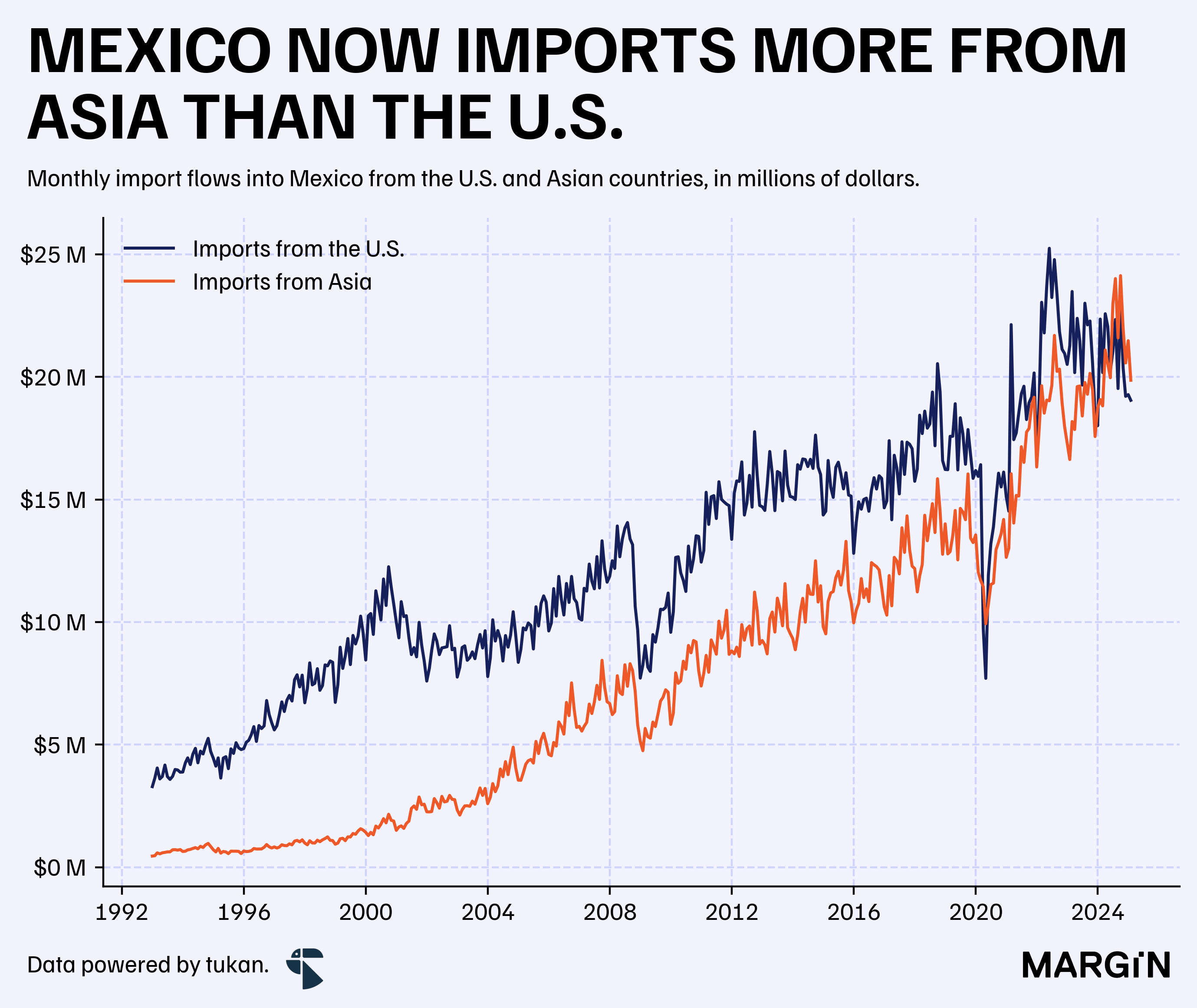

Trade

Mexican exports totaled $49 billion USD in February of this year, recording an annual contraction of almost 3%.

Notably, exports to European countries declined by more than 22% YoY and reached one of the lowest values in recent years: $1.8 billion USD.

On the other end, total imports came in at $47 billion USD — declining by 8% YoY, with merchandise coming in from the United States contracting by close to 15% YoY during the month. Asian imports, on the other hand, grew by more than 4% YoY.

At the beginning of 2024, total Asian imports exceeded those coming in from the United States into Mexico for the first time in history. This event has held true every single month since July 2024.

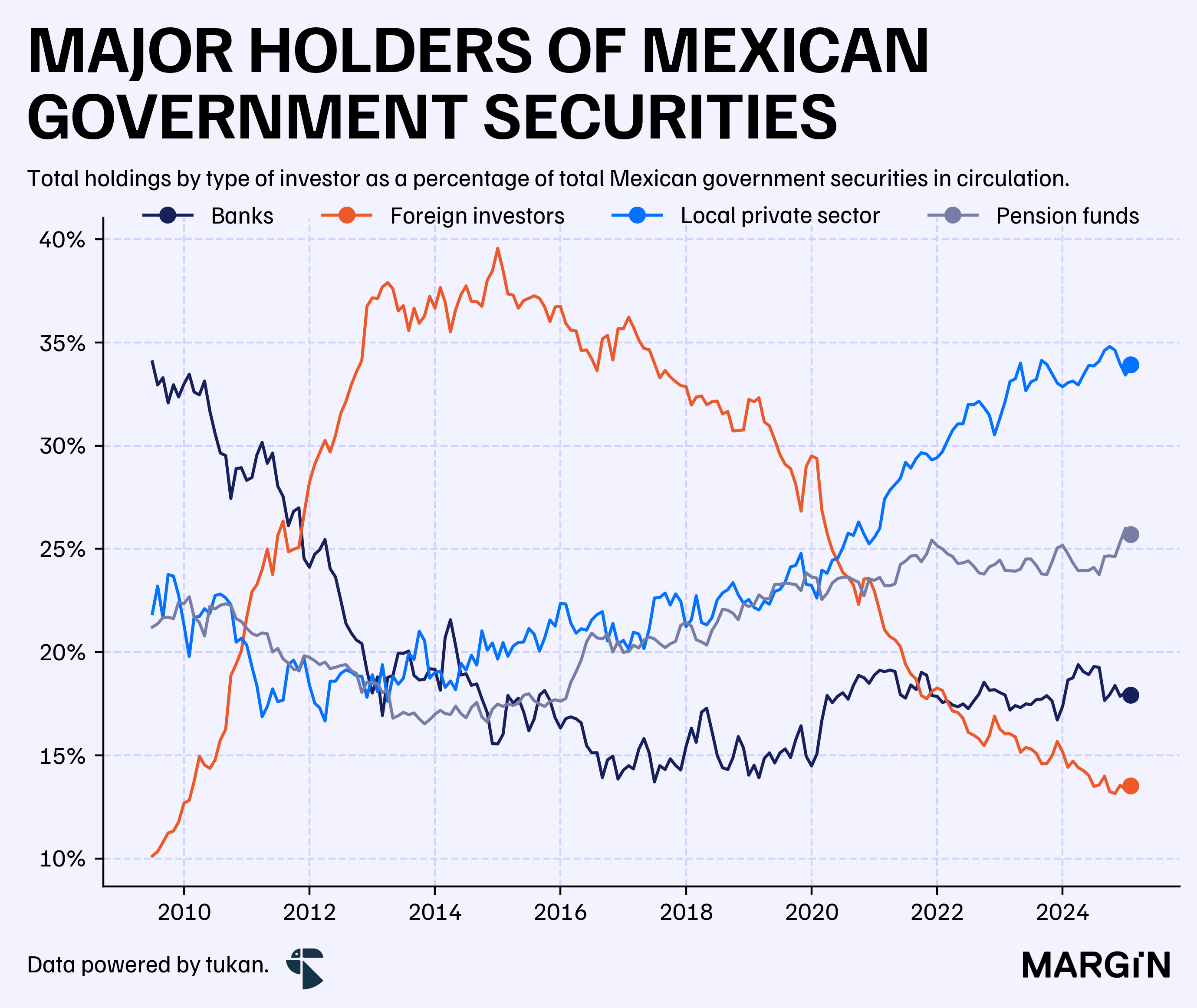

Government securities

Foreign investors increased their total position on Mexican government securities by more than 7% YoY in February of 2025.

Despite the increase in the investors’ position, securities held by foreign investors as a percentage of all securities in circulation closed the second month of this year at 13.5% — 88 basis points lower than at the end of February 2024.

Up until May 2020, foreign investors held the most “interest” in local government securities. Since then, commercial banks, pension funds and the private sector (in Mexico) have surpassed them as major holders of government bonds.

This is only considering data for brands which report data to INEGI. For example, BYD (a major Chinese brand) is not included in the analysis.

Based on first-quarter data for 2025.