Monday, On the Margin

Consumer data; SOCAPs; industrial activity; vehicle sales and production; airports and tourism.

Early warnings

Signs of deterioration in the current economic climate continue to emerge. This time, we saw the impact directly on statistics surrounding consumer spending.

Credit and debit card transaction data for February brought upon some elements of concern as purchase volumes in big box stores (i.e. Walmart, Soriana, La Comer, etc.) declined by almost 3% year-over-year (YoY).

Aside from three months in the peak of the pandemic, this is the first time that card transactions in big box stores record an annual contraction in purchase volumes.

The annual contraction came in despite having a 5% increase in total transactions across the country. This implies that the average purchase declined by more than 8% YoY in one of the most resilient categories for Mexican households.

We find this decline particularly concerning because:

Mexicans are adopting digital payments at a rapid pace since the pandemic, which implies that card transactions are expected to go up regardless of the overall spending trend.

The decline hits a category that is expected to be resilient even under the harshest economic conditions.

Overall, the use of credit and debit cards grew by 14% YoY in February, resulting in a processed volume of over $462 billion pesos (+9% YoY). Although still robust, this growth rate decelerated considerably (-3 percentage points) from the one recorded in January of this year.

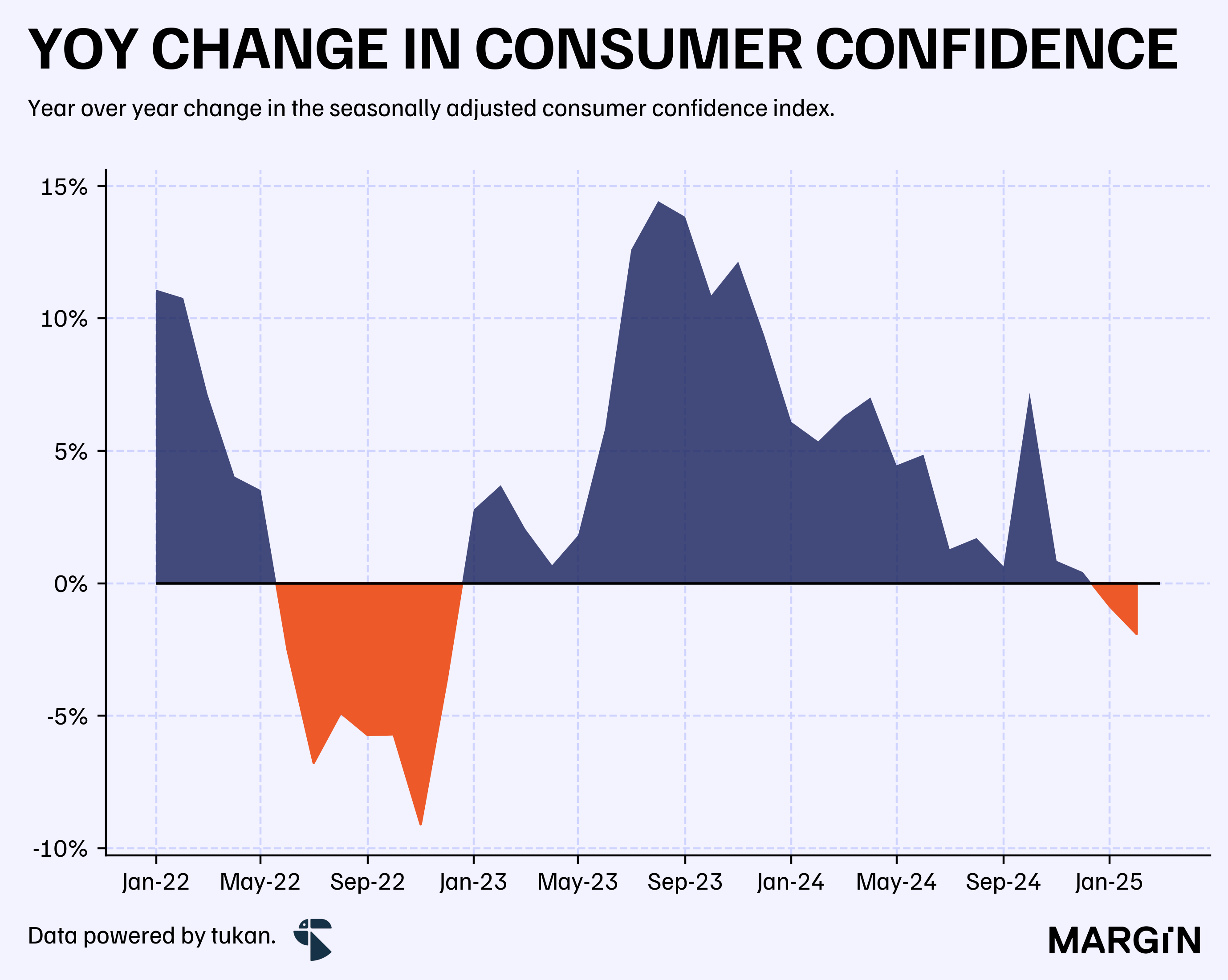

Concerns around consumer spending were also supported by INEGI’s consumer confidence survey, which recorded it’s first two consecutive contractions after posting sustained growth throughout 2023 and 2024.

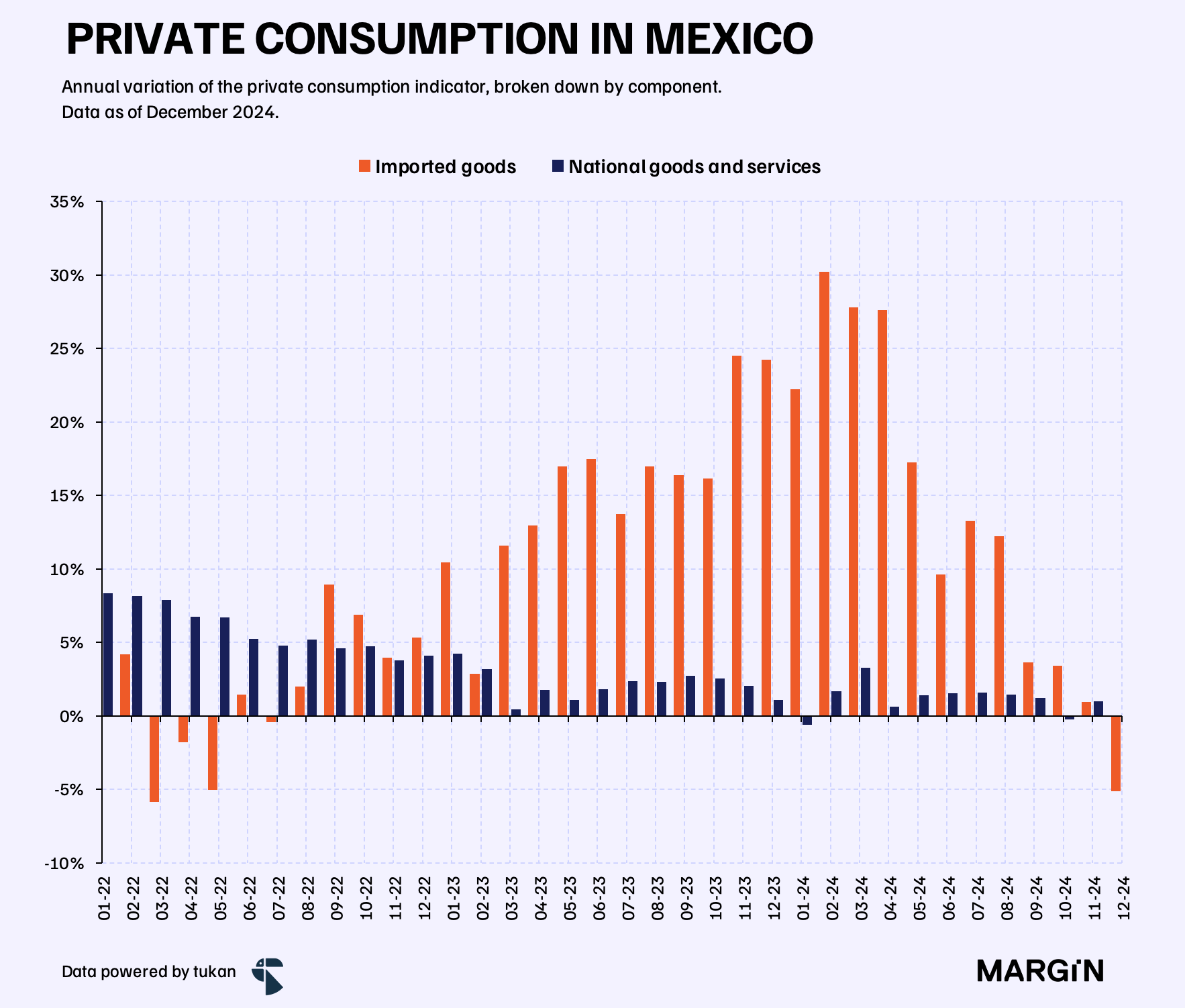

As we mentioned last Monday, the loss of confidence has also started to impact overall consumption trends — with overall consumption levels being down by 0.8% YoY at the end of December; ending a streak of 45 consecutive months of growth.

According to INEGI, the decrease was due mainly to a 5.1% contraction in the demand for imported goods.

On that note, it’s possible that we will see a stronger impact on the consumption of imported goods given the uncertainty behind the United States trade war with the rest of the world.

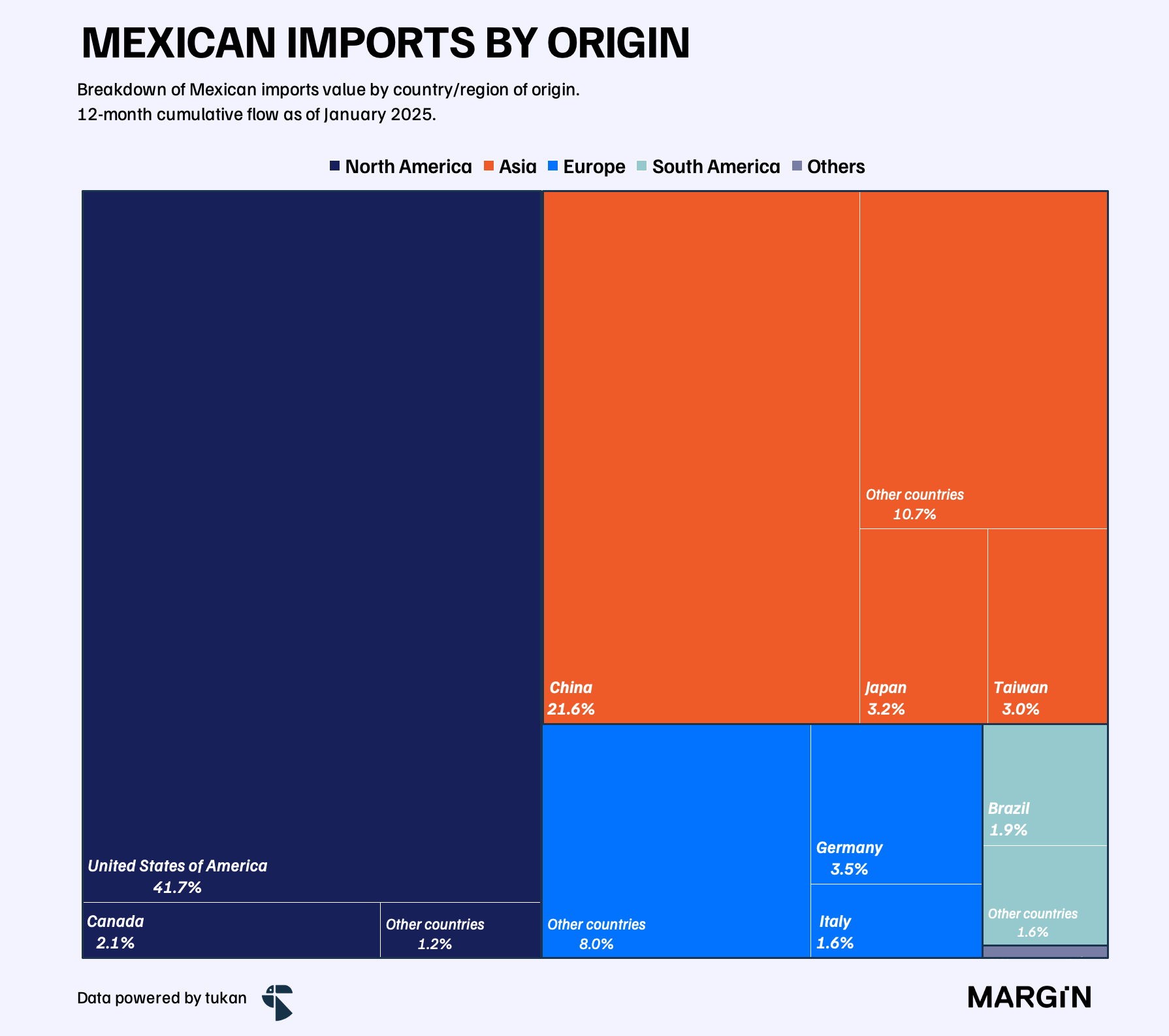

As of the latest available data, imports from the U.S. accounted for close to 42% of international purchases by the Mexican economy.

SOCAPs

Loan portfolios for cajas de ahorro (SOCAPs) reached $164.8 billion pesos at the end of February — 13% above the previous year’s figures.

Housing loans — which represent close to 10% of the total portfolio — was the strongest growing product in the sector, recording an annual growth rate of 16%. Consumer financing also recorded a double digit growth rate slightly below 13% during the month.

Industrial activity

The contraction in the industrial sector persisted at the beginning of 2025. The industrial activity index fell by 0.4% month-over-month (MoM) and by 2.8% YoY in January, according to seasonally adjusted figures. Annually, this was the second-largest decline in the index since it began contracting, in September 2024.

Certain mining and construction activities experienced double-digit annual declines in January, such as civil engineering construction (-27%) and oil and gas extraction (-11%). Meanwhile, the decrease for the manufacturing industry was less than a percentage point.

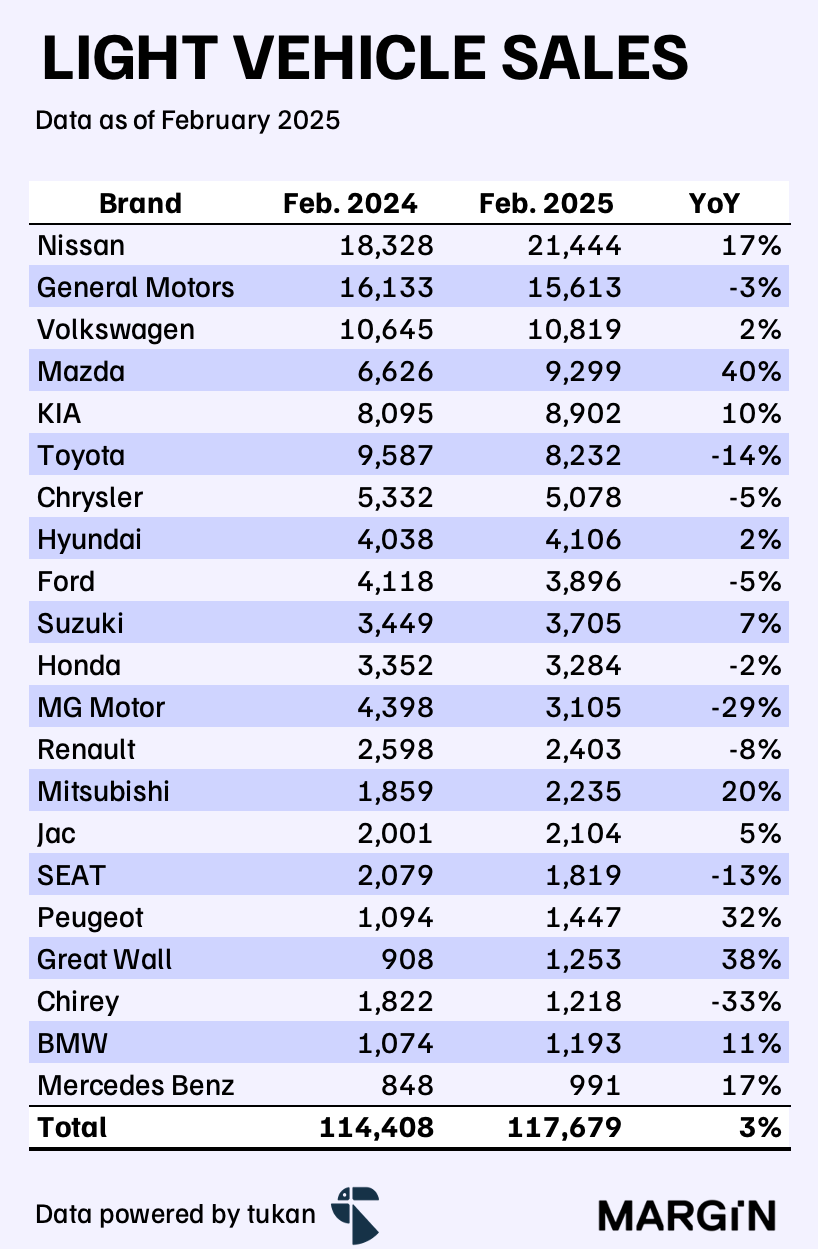

Vehicle sales

New car sales came close to 120 thousand units during February — representing a modest 3% annual increase.

Market leader Nissan achieved a 17% YoY increase, equating to over 3,100 additional cars sold. In contrast, sales for the second-largest player, General Motors, declined by about 500 units (-3% YoY).

It’s worth highlighting the poor performance recorded by top Chinese brands such as: MG Motors (-29% YoY) and Chirey (-33% YoY).

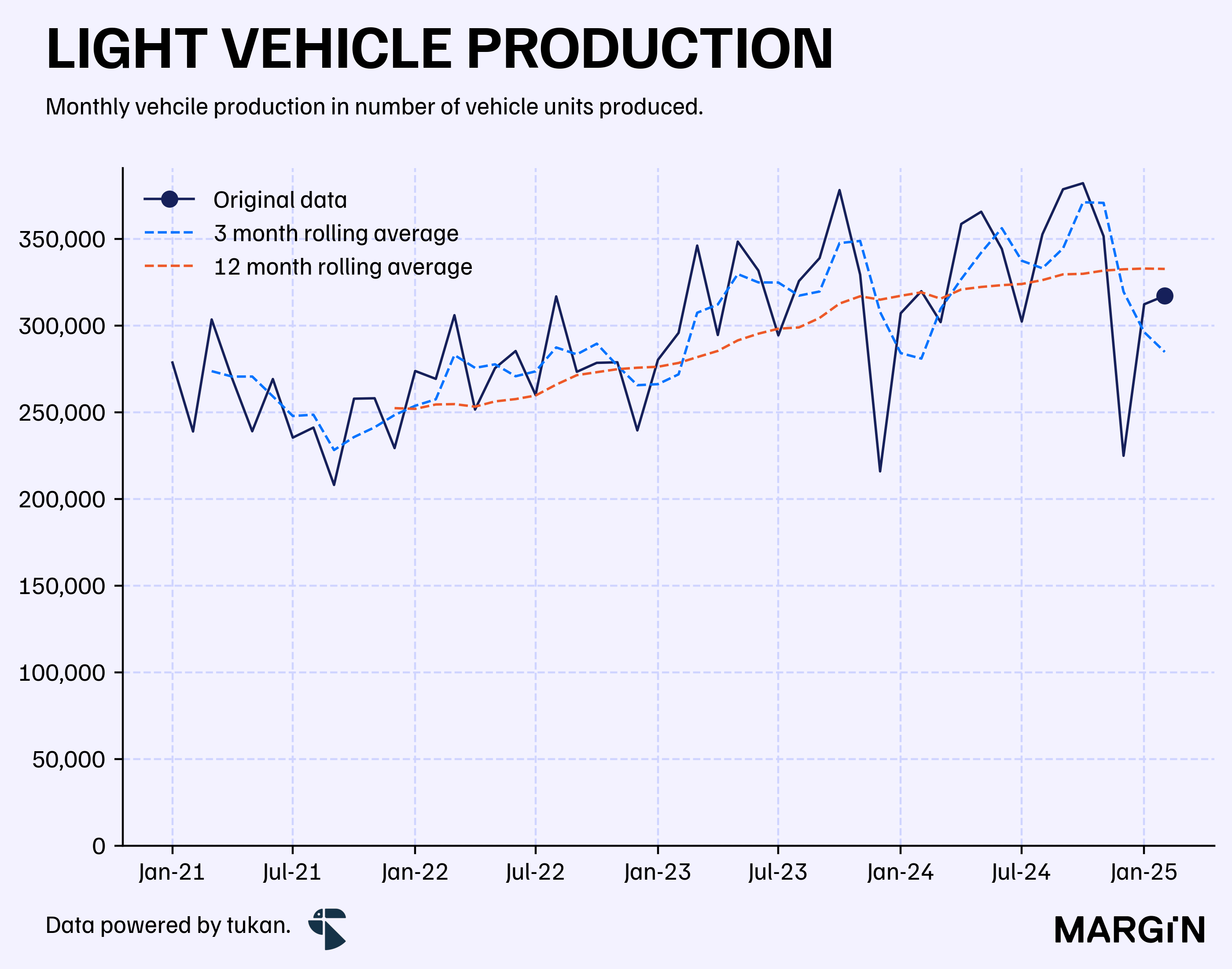

Vehicle production

Light vehicle production came in at 317 thousand units during February, representing a very slight decrease of 0.8% when compared to the previous year.

According to INEGI, Mexico’s most produced vehicles were:

The Tacoma from Toyota at 21 thousand units (+67% YoY).

The Equinox from General Motors at 19 thousand units (+28% YoY).

The Kicks from Nissan at 18 thousand units (+50% YoY).

The Versa from Nissan at 17 thousand units (-7% YoY).

The HRV from Honda at 16 thousand units (-2% YoY).

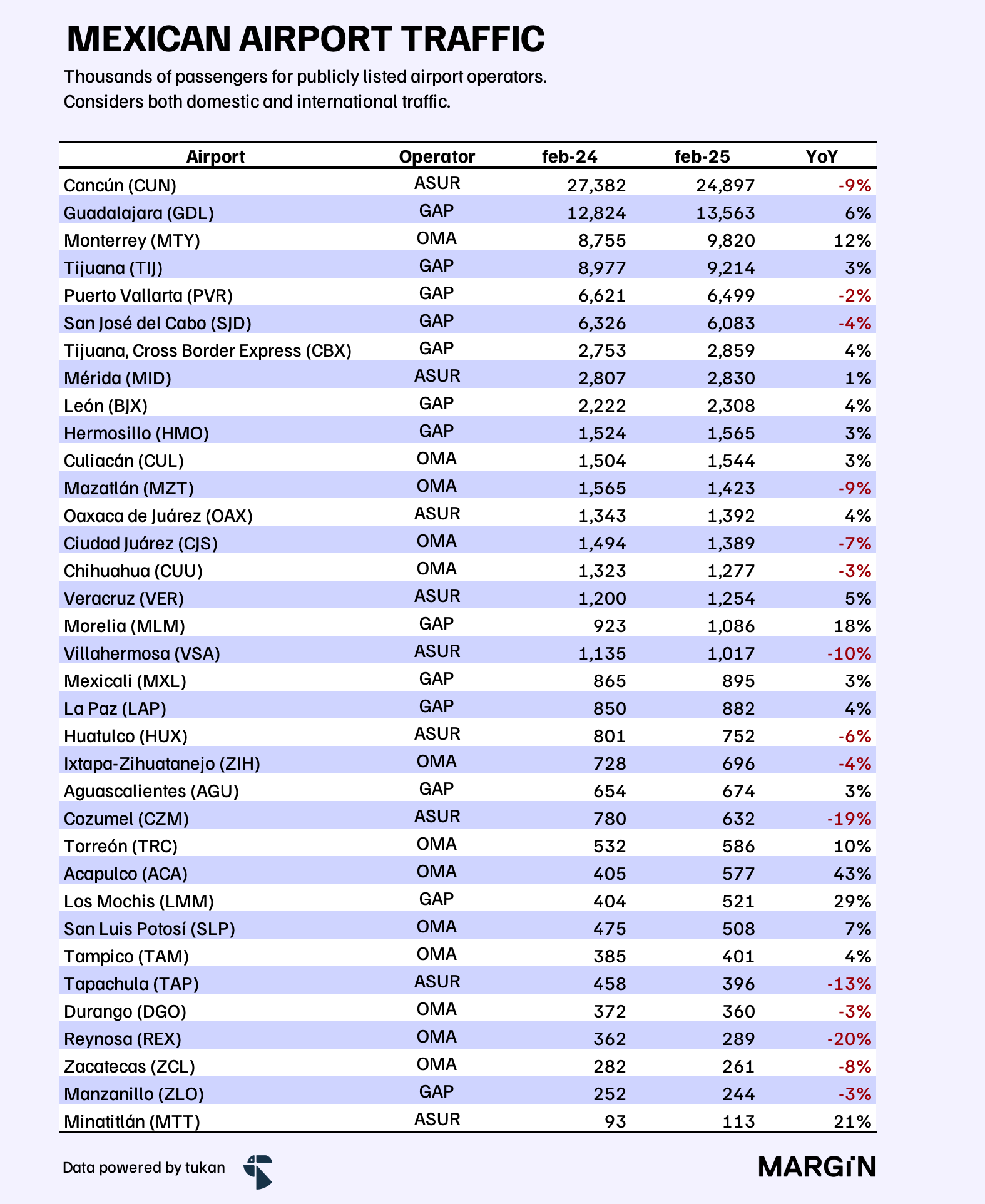

Airports

Total passenger traffic (including international operations) for Mexico’s publicly listed airport groups (OMA, ASUR, and GAP) remained relatively flat during February 2025 (+0.3% YoY).

Focusing exclusively on Mexican operations, the total passenger count declined by 1%.

In this case, GAP experienced the highest growth at 7%, primarily driven by increased traffic at Guadalajara airport (+6% YoY). OMA followed with a 4% increase, boosted by a 12% growth rate at Monterrey airport. Lastly, ASUR recorded an 8% decline, hindered by a 9% contraction in the number of travelers passing through the Cancun airport.

Tourism

The tourism sector remained dynamic throughout 2024. According to SECTUR data, hotel occupancy in Mexico closed December with an overall rate of 59.3% across 70 touristic destinations, a similar level to that at the end of 2023.

Beach destinations achieved a higher occupancy rate of 65.8%. Puerto Escondido, in particular, showed the largest annual increase of 4.8 percentage points, reaching an occupancy rate of nearly 46% at the end of 2024.