Monday, On the Margin

BBVA; Regional; Santander; BanBajío; remittances; regional statistics; business confidence.

BBVA

Grupo Financiero BBVA closed 1Q25 with over 32.6 million clients (+0.6% YoY) and with over $3.8 trillion pesos in total assets (10.5%).

The group’s total profits came in at $28 billion pesos (+10.4% YoY) — 88% of which were contributed directly by the banking operation and almost 11% by the insurance division (+16.6% YoY).

For context, Walmart México and FEMSA reported a combined net profit figure of $21.2 billion pesos during the first quarter of this year.

According to CNBV data as of February 2024, BBVA won 56 bps of market share in the banking sector’s total profits (32%) during the first two months of the year.

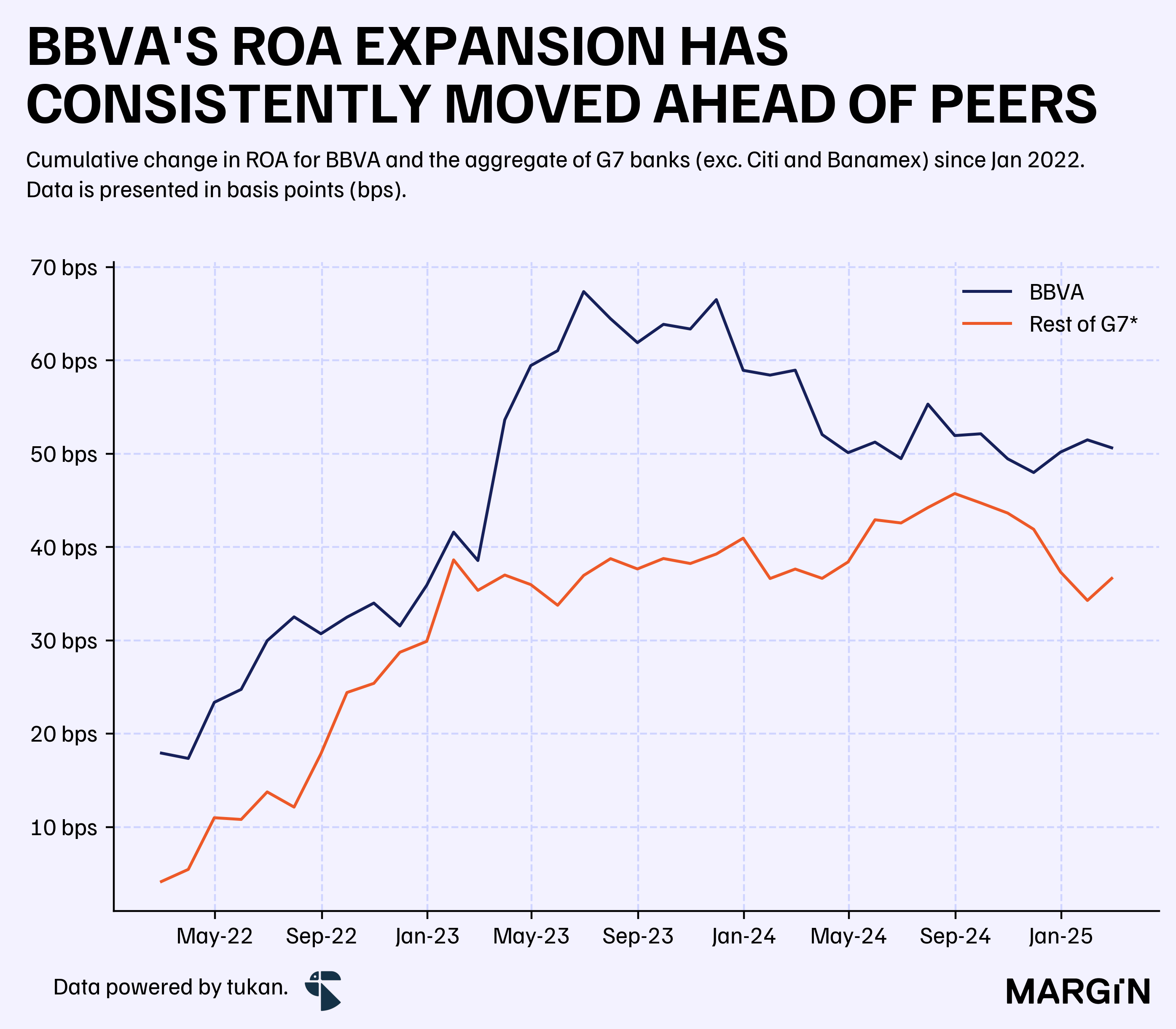

As can be seen on the chart below, during the past couple of years, BBVA has consistently expanded it’s ROA against its main competitors.

Regional

Total loans for Regional closed the month of March at $180.9 billion pesos (+13% YoY).

Hey Banco, which accounts for 5% of the total loan book, grew its loan portfolio by 2%; but presented solid double digit growth (+19% YoY) in core deposits during the quarter to close the month of March with +$12 billion in balances.

For reference, fintechs such as Finsus and Stori would have close to $13 billion and $8 billion in core deposits.

Total profits increased by 1% YoY ($1,633 million pesos), with the company’s NIM expanding by 44 basis points and the efficiency ratio worsening by around 85 bps YoY.

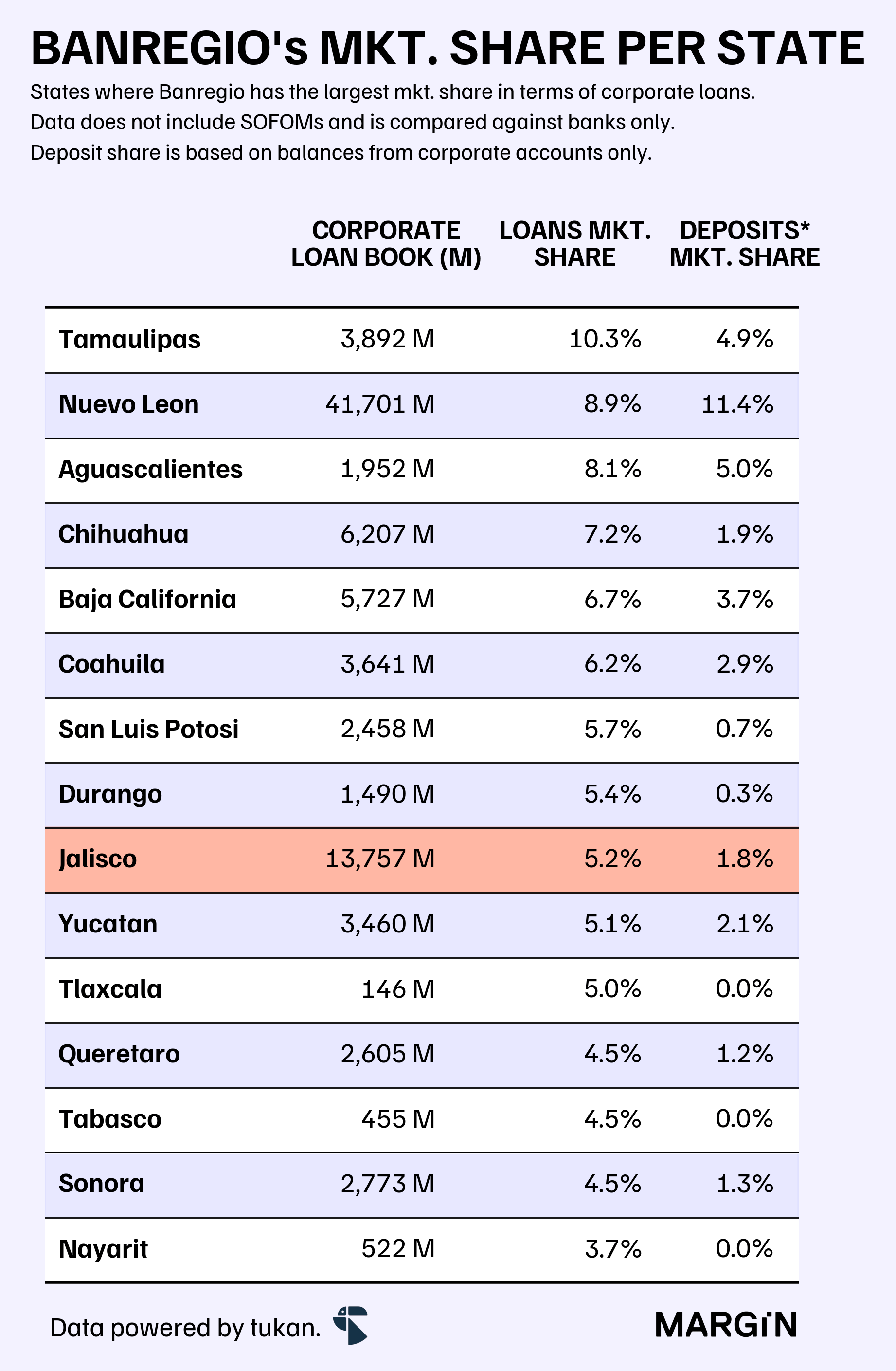

Performing loans to corporates grew at double-digit rates across the board, with particularly good results in the state of Jalisco (+16% YoY). According to CNBV data, Banregio currently has a 5% market share within that state in terms of the total corporate loan portfolio. However, they hold less than 2% of Jalisco’s wholesale deposit base (i.e. deposits balances of corporate clients).1

We’ve recently received a lot of comments asking us to switch the language of Margin to Spanish. What do you think?

Santander

First quarter results showed a 6.7% YoY expansion in the group’s total loan portfolio — a figure mostly impacted by sluggish growth in the commercial side2 of the business.

Consumer loans and mortgages, on the other hand, grew by 12.8% and 7.4%, respectively on a YoY basis during the quarter.

According to February CNBV data, Santander lost 42 bps (YoY) in market share across consumer loans against other banks, as well as losing 137 bps in the commercial loans market; resulting in an overall loss of 95 bps in total market share.

Profits totaled $7.4 billion during the first three months of the year (+7.8% YoY) — implying a ROA of 1.5%.

BanBajío

Net income for Banco del Bajío contracted by 10.4% during the quarter, impacted mostly by a 3.2% contraction in interest income and a 10.3% increase in non-interest expenses. This was partially offset by a 25% increase in other operating income (mostly trading income and commissions).

The contraction in interest income was mainly caused by cuts to the Mexican reference rate. According to the bank’s press release, BanBajío currently has a NIM3 (net interest margin) sensitivity of 21 bps for each 100 bps change in the Mexican reference rate.4

The bank from Guanajuato continues posting double digit growth across its consumer loan book, which as of March, accounted for just 2.6% of the company’s total loans — 5 years ago, this segment accounted for 1.3%.

Total loans grew by 10.8% YoY.

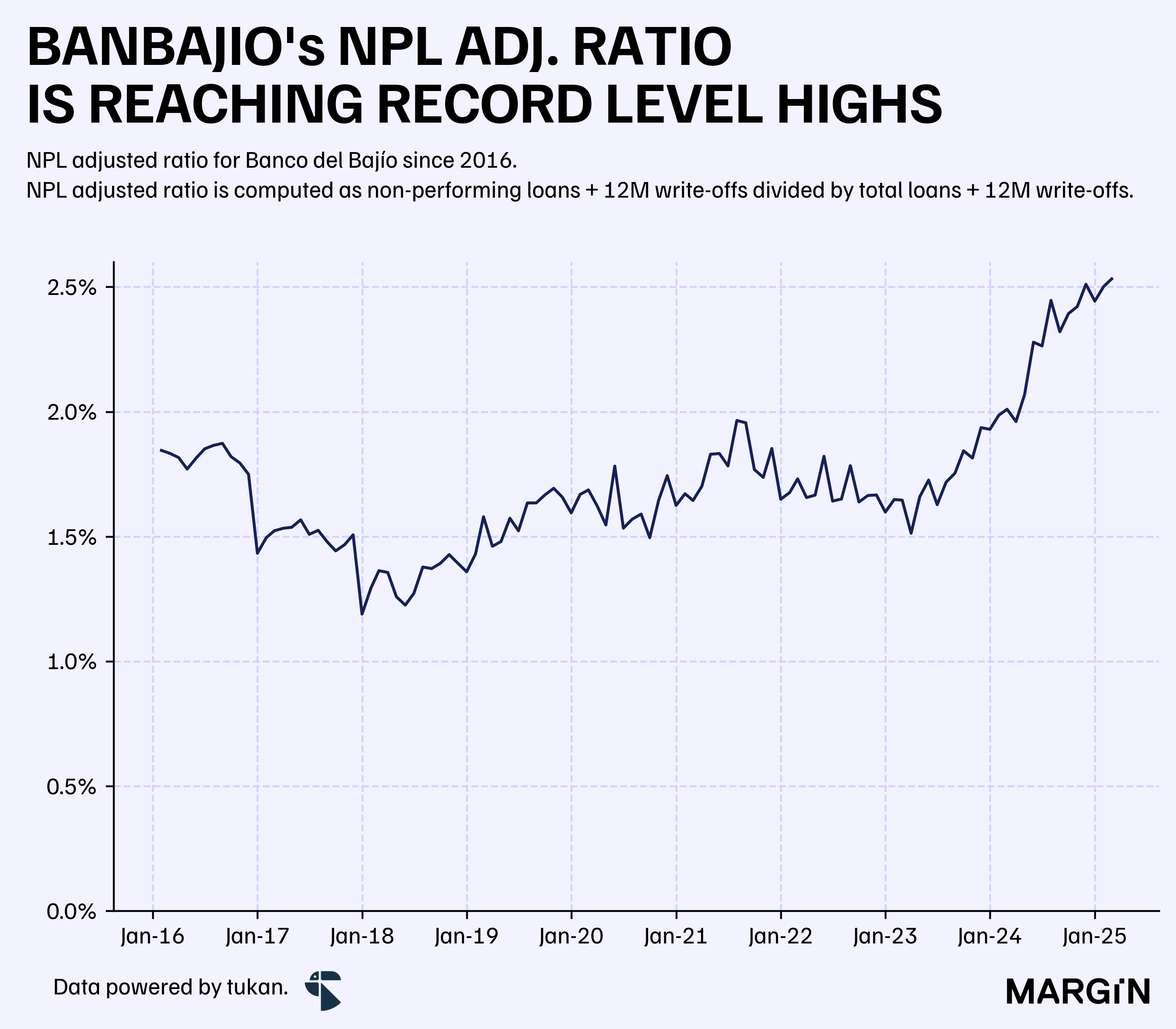

Despite the bank boasting one of the lowest NPL adjusted ratios in the market, CNBV data showed the asset quality indicator reaching one of its highest levels in the past 10 years.

This change has been mostly driven by a higher exposure to consumer loans, a segment where BanBajío recorded an NPL adjusted ratio of 11% (vs. 10.6% for the system’s aggregate).

Remittances

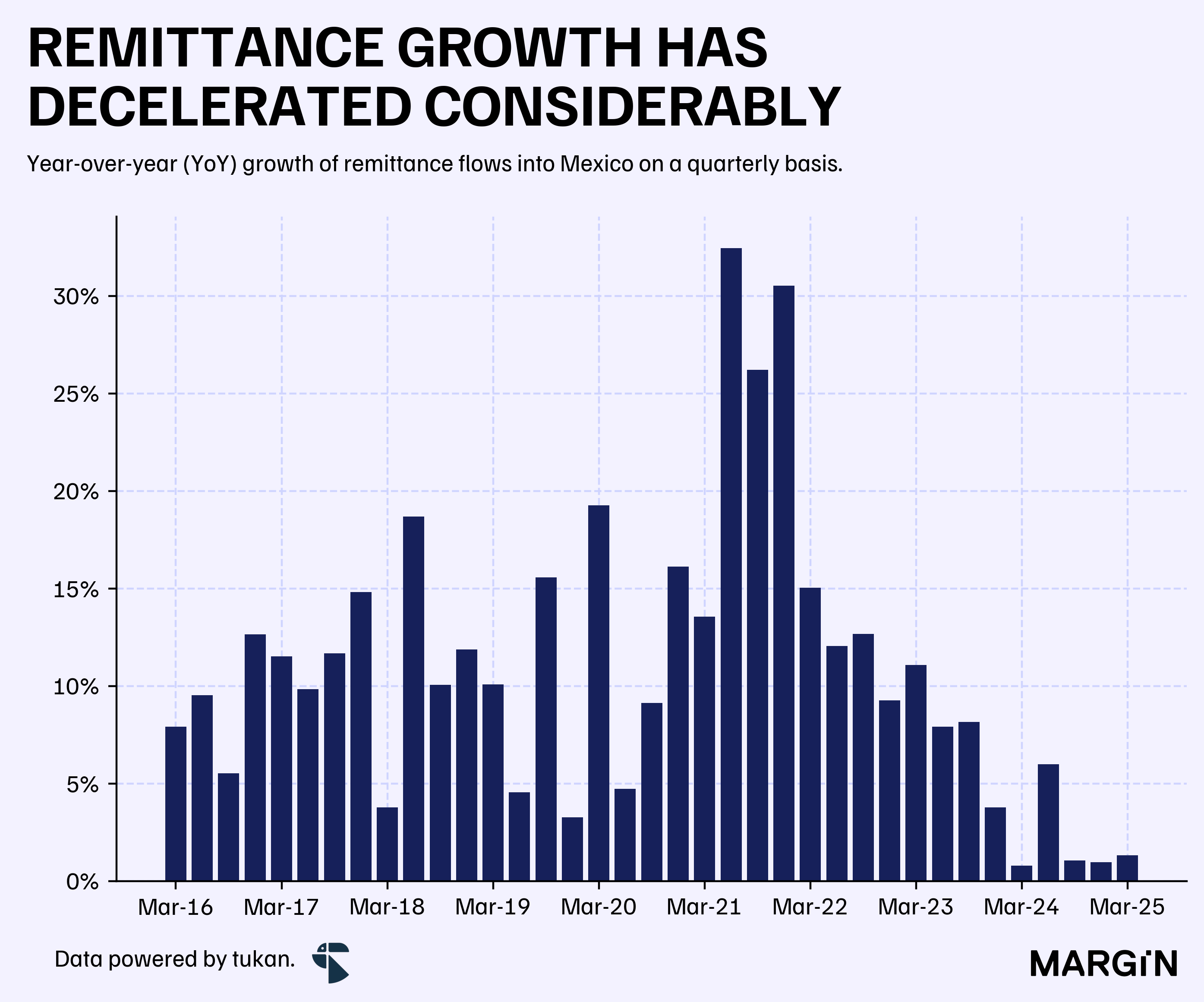

Total remittances (in terms of monetary value) increased by 1.3% YoY during the first quarter of the year, showing some deceleration when compared to previous quarters.

With consumer confidence in the United States tumbling to one of it’s lowest levels since 2021 it’s hard to see how remittances into Mexico might pick up their growth trend in the near future.

ITAEE

According to INEGI’s regional economic activity index (ITAEE) the states with the highest growth rates during the 4th quarter of 2024 were Guerrero, Zacatecas and Oaxaca.

The south of the country, in particular: Campeche, Quintana Roo and Tabasco suffered the largest contractions.

Business confidence

INEGI’s business confidence survey showed another month of “negative” perception across business leaders in all major industries in the country.

According to INEGI, manufacturing, trade and services recorded their second consecutive month with confidence levels below the 50 point threshold5 during the month of April. Construction, on the other hand, posted it’s eight consecutive month of a “pessimistic” outlook.

Data as of February and does not include SOFOMs that consolidate with Banregio.

Corporate loans, SMEs, government and financial entities.

Interest income minus interest expenses divided by total productive assets.

If the reference rate goes down by 100bps, the BanBajío’s NIM goes down by 21 basis points.

Index below 50 points to pessimism, and vice versa.

Estaría bueno que las notas salgan en español!