New Horizons

What has happened with Mexican air traffic since the cancellation of the NAICM?

Prior to 2020, close to half of Mexico’s total air passengers passed through the boarding gates of the Mexico City International Airport (AICM), causing the country’s main airfield to surpass its 30 million traffic capacity almost every year since 2013.

Four years later, the cancellation of the New Mexico City International Airport (NAICM) — the massive infrastructure project aimed to decongest the Mexican capital — seems as something buried in the past.

Just during the first 7 months of 2024, Mexico City’s passenger count has dropped to just 37% of the country’s total regular air traffic. A figure 12 percentage points lower than the one reported in 2019, the first full year after the NAICM referendum.1

Prior to the official cancellation of the project, much was discussed about the potential consequences of such a decision. However, there has been little discussion since 2020 regarding what has actually transpired.

In today’s Margin article, we explore the shift in Mexico’s air traffic operations since 2019. Have route combinations reshaped? Has there been a clear effect on the publicly-listed airport operators? Which other hubs might be developing due to this decision?

Taking Flight

Based on CONAPO population projections and SCT data, Mexican air passengers per capita closed out 2023 at a rate of 1.4, growing at a CAGR of 6.2% over the past 13 years.

Excluding Mexico City from the equation, the traffic penetration rate increased at a slightly higher 6.8% CAGR during the same period (1.4 percentage points on top of the 5.4% reported for the country’s capital).

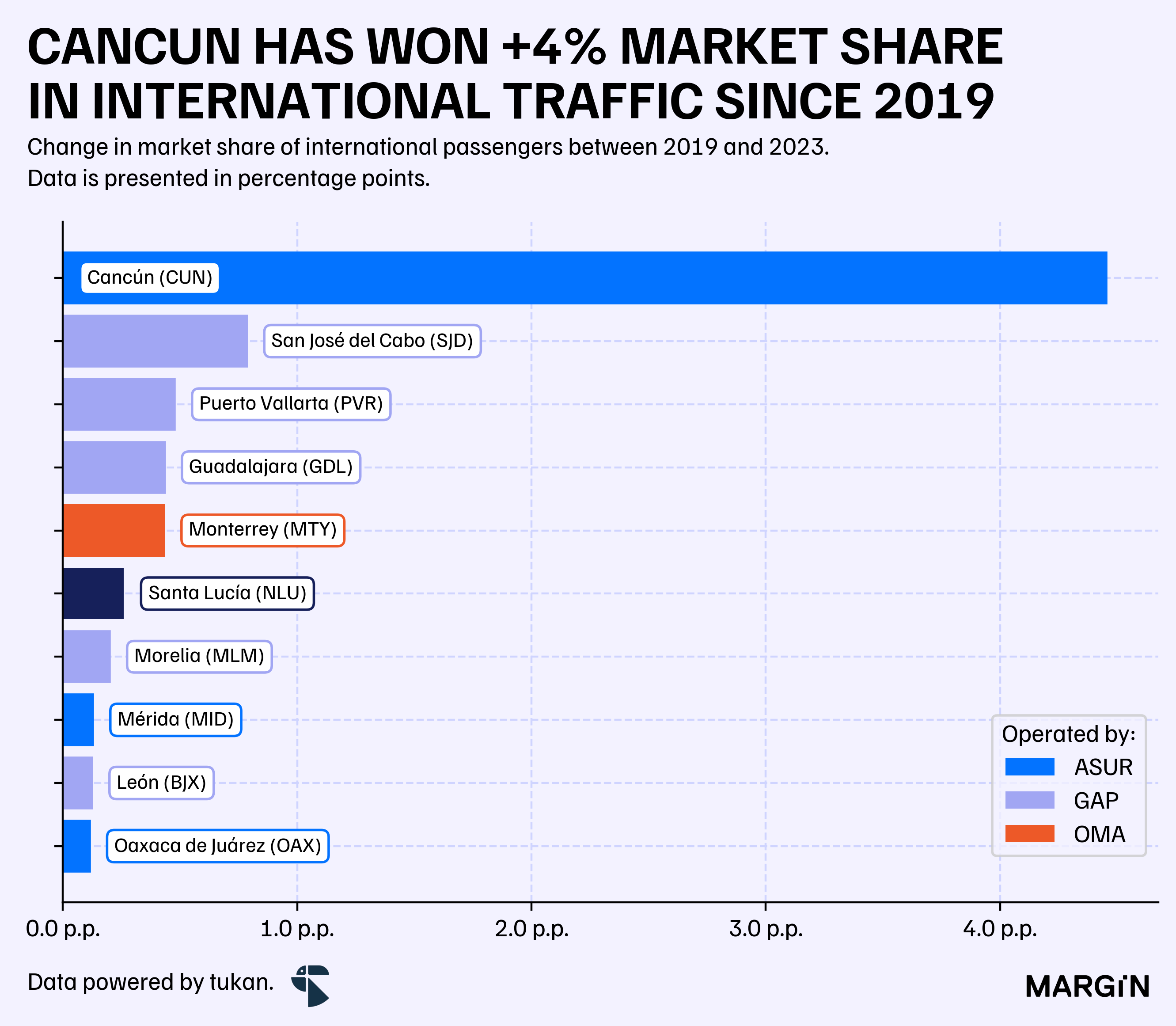

However, much of this is influenced by the country’s touristic hubs that drive most of international traffic into the country. According to SCT data, international flights made up 46% of the country’s total passengers — a category, where Mexico City’s airport ranks just behind Cancun with 29.5% of the total market share.

Since the NAICM’s cancellation, Mexico City has lost around 7 percentage points of market share in terms of international passengers. ASUR’s Cancun “captured” 4 of those points, while GAP’s Guadalajara, Cabo, and Vallarta captured 1.5 points in aggregate. The AIFA managed to gain just 0.3 points since its inauguration.

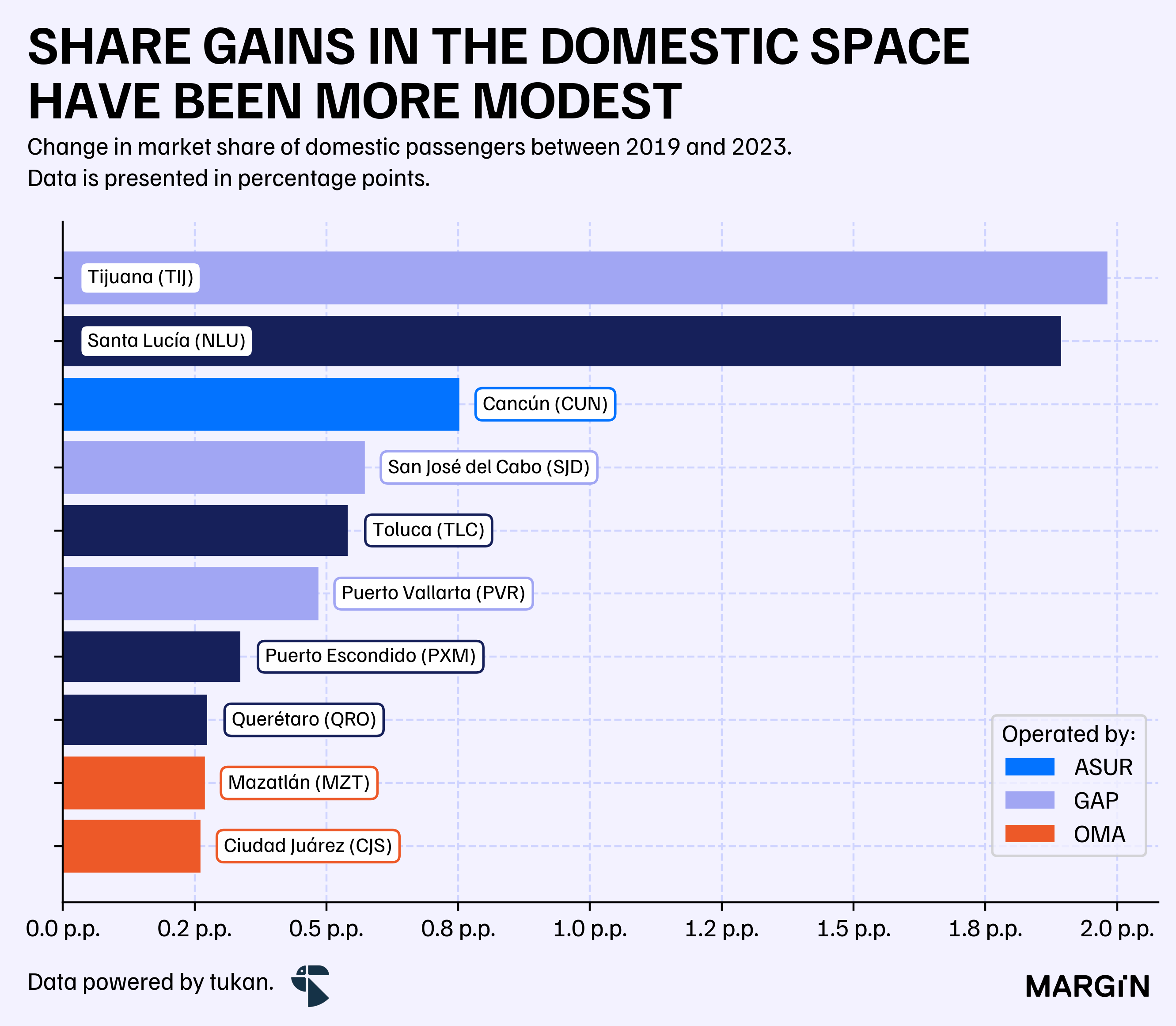

On the other end, domestic operations have taken a lesser hit.

Since 2019, the AICM has dropped just shy of 6 points in traffic share. Here, the main “winners” have been airports such as: Santa Lucía (the NAICM’s alternative), Tijuana and Cancún.

It stands out that airports from major cities such as: Monterrey and Guadalajara, which rely mostly on domestic traffic (over 70%), haven’t been gaining ground as domestic hubs since the cancellation of the NAICM.

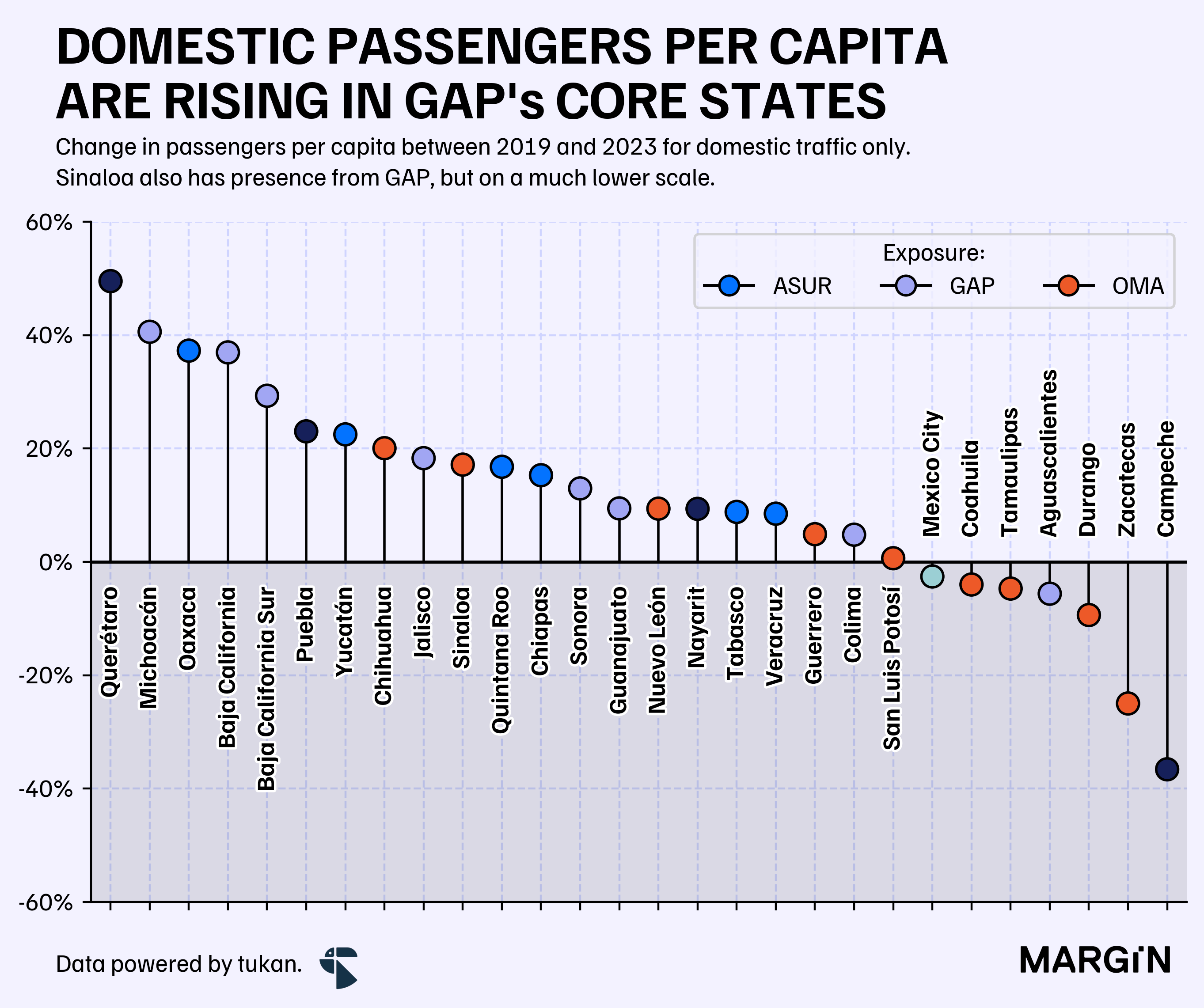

Aside from Santa Lucía (AIFA), which operates with one of the lowest passenger-per-flight ratios in the country (100 passengers per flight), much of the increase in domestic traffic can be attributed to higher adoption of this mode of transportation in other regions of Mexico.

In the chart below, we present changes in passenger-per-capita rates for each state in the country, focusing solely on domestic traffic.

As seen in the previous figure, GAP’s markets have experienced some of the most significant increases in trips per capita since 2019. The states of Baja California, Baja California Sur, and Michoacán, which are home to five of GAP’s airport concessions, account for nearly 42% of the company’s domestic traffic. All of these states reported increases of over 20% in their passenger-per-capita ratios.

OMA, on the other hand, has seen domestic trips per capita decrease in four of its markets, making it the only operator to experience contractions in this ratio across multiple states. These four states—Durango, Coahuila, Tamaulipas, and Zacatecas—accounted for just 10% of OMA’s total domestic traffic in 2023.

It’s worth noting that, unlike GAP and ASUR, which have a more balanced exposure to both domestic and international traffic, OMA’s operations rely on domestic trips for more than 80% of their total traffic.

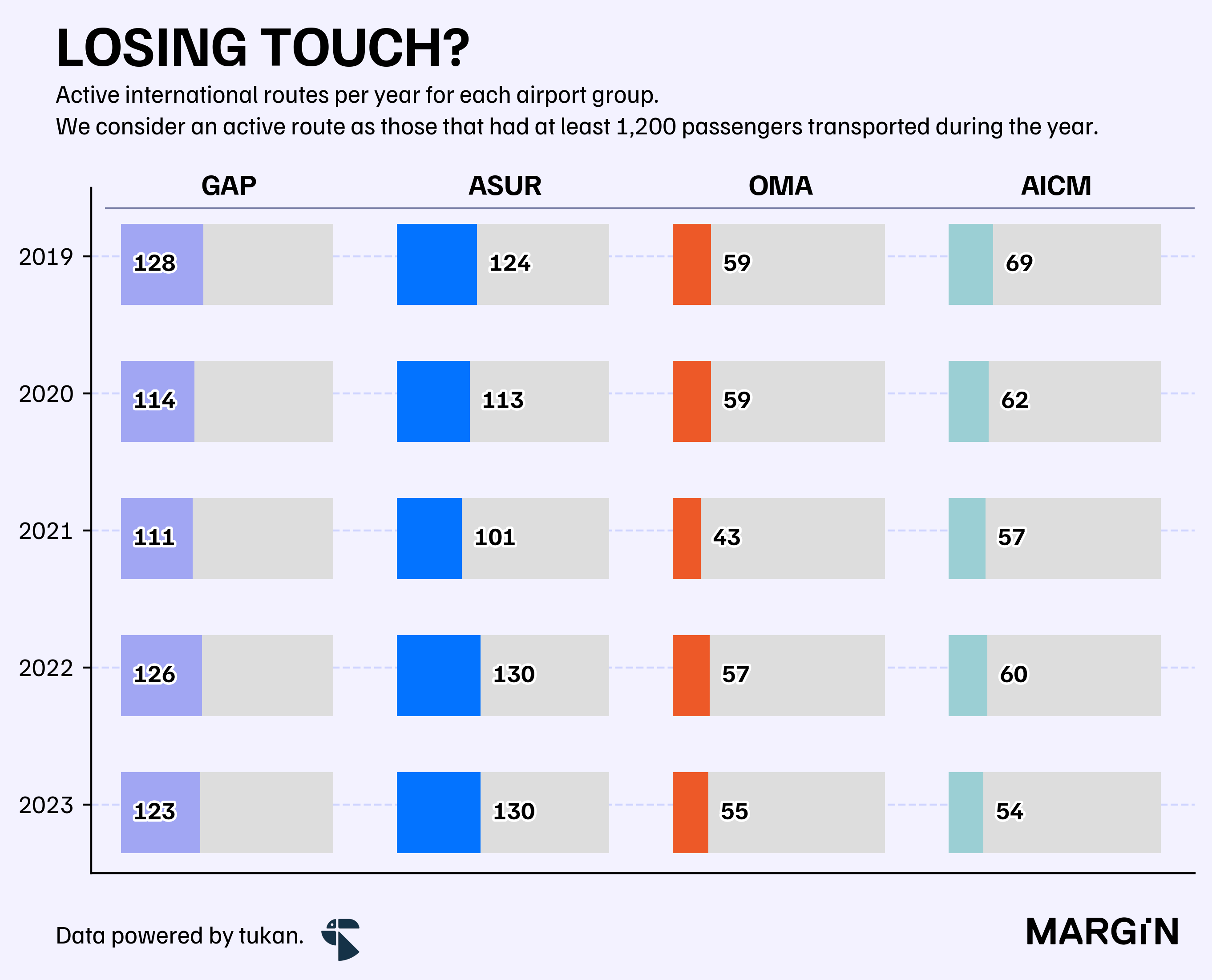

Rerouting

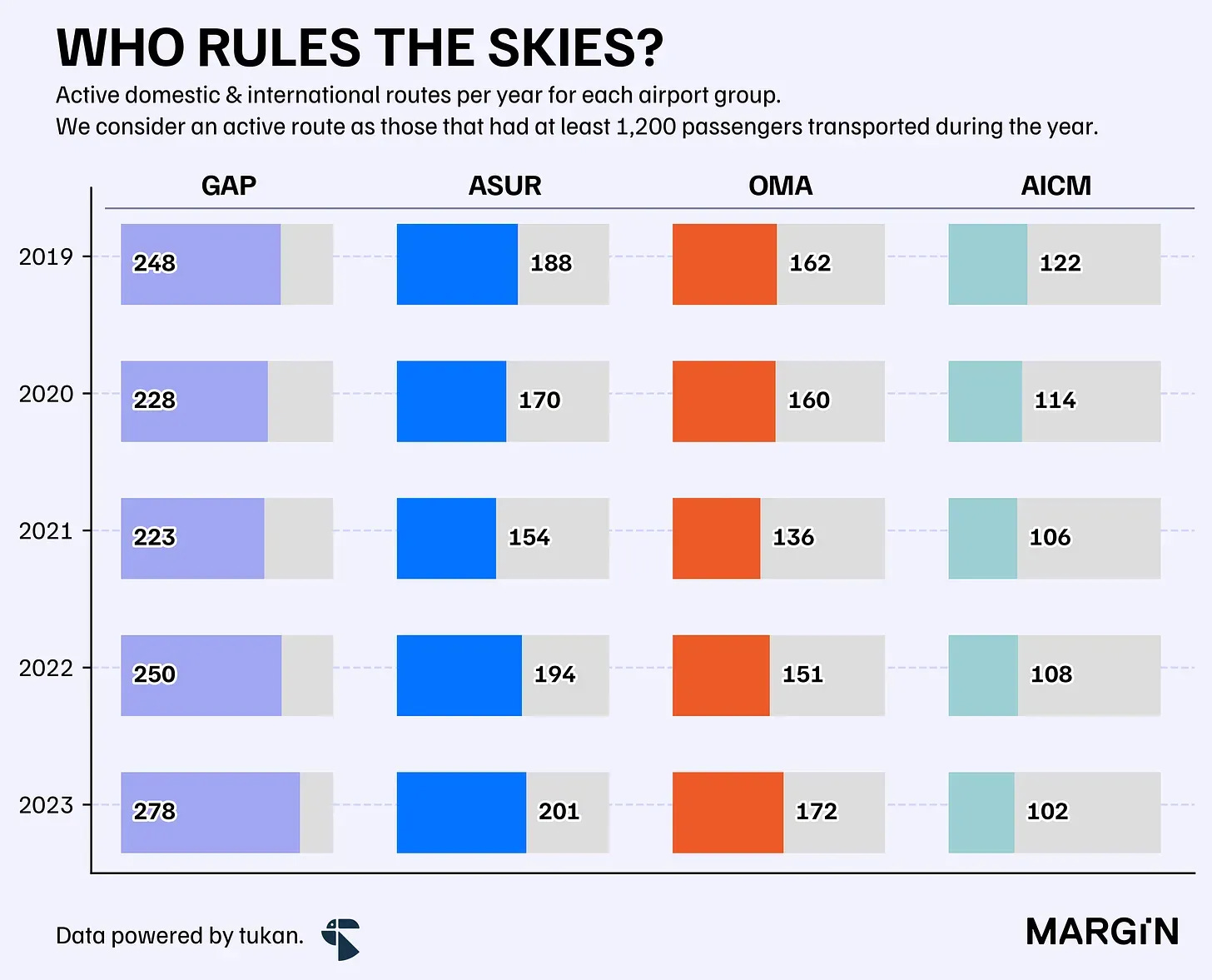

Based on SCT data, we estimate that the Mexico City airport had close to 122 active routes in 2019. A figure that has since dropped by more than 16% in the span of 4 years.2

GAP, ASUR and OMA, on the other hand have seen increase in routes by more than 12%, 7% and 6%, respectively.

According to our calculations, we estimate that GAP has added close to 35 (net) new domestic routes since 2019 — implying a (net) “drop” of 5 international destinations for the airport group. At the same time, we observe a (net) reduction of 15 international routes for Mexico City’s airport.

All in all, the four major airport groups of the country have lost (in aggregate) 18 international connections since 2019; passing from 380 active routes in 2019 to just 362 in 2023.

The Santa Lucía airport reported 25 active domestic routes and 4 international ones during 2023.

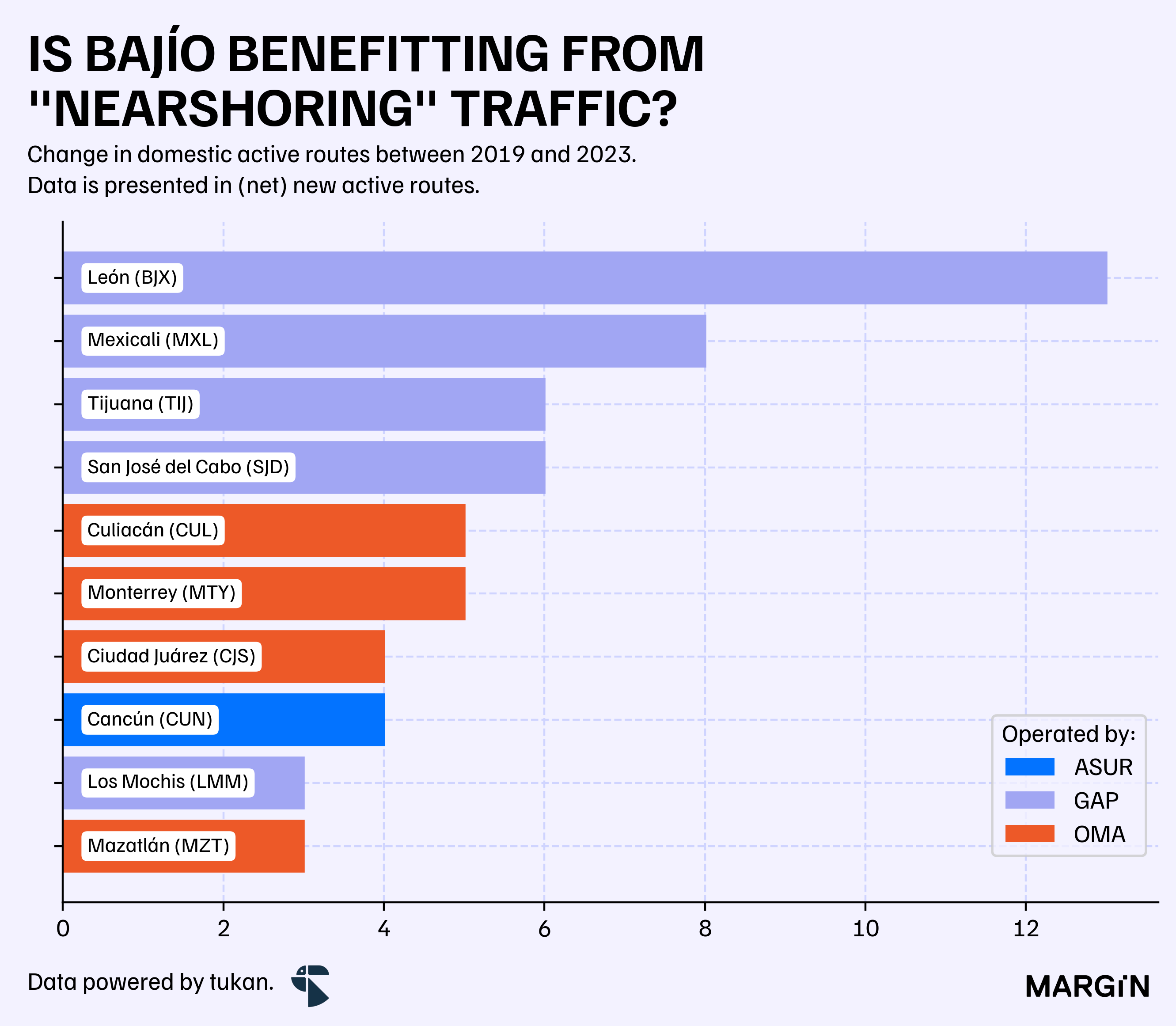

Zooming into individual airport data, where has traffic availability shifted the most?

According to our analysis, we surprisingly saw GAP’s Bajío airport as the one with most new (net) active domestic routes — something that could likely be a consequence of the region’s recent boom as a nearshoring hotspot.

Since 2019, the León airport has added routes to destinations such as: Culiacán, Hermosillo, La Paz, Oaxaca, Veracruz, Tuxtla and Mazatlán.

On the other end, only three airports in the country opened up more than 2 international routes (net) since 2019: Cancún, Mérida and Loreto.3

Cancun’s new routes according to SCT data include: San Diego, Portland, Rome, Cali, Barcelona, Quito and Vienna.

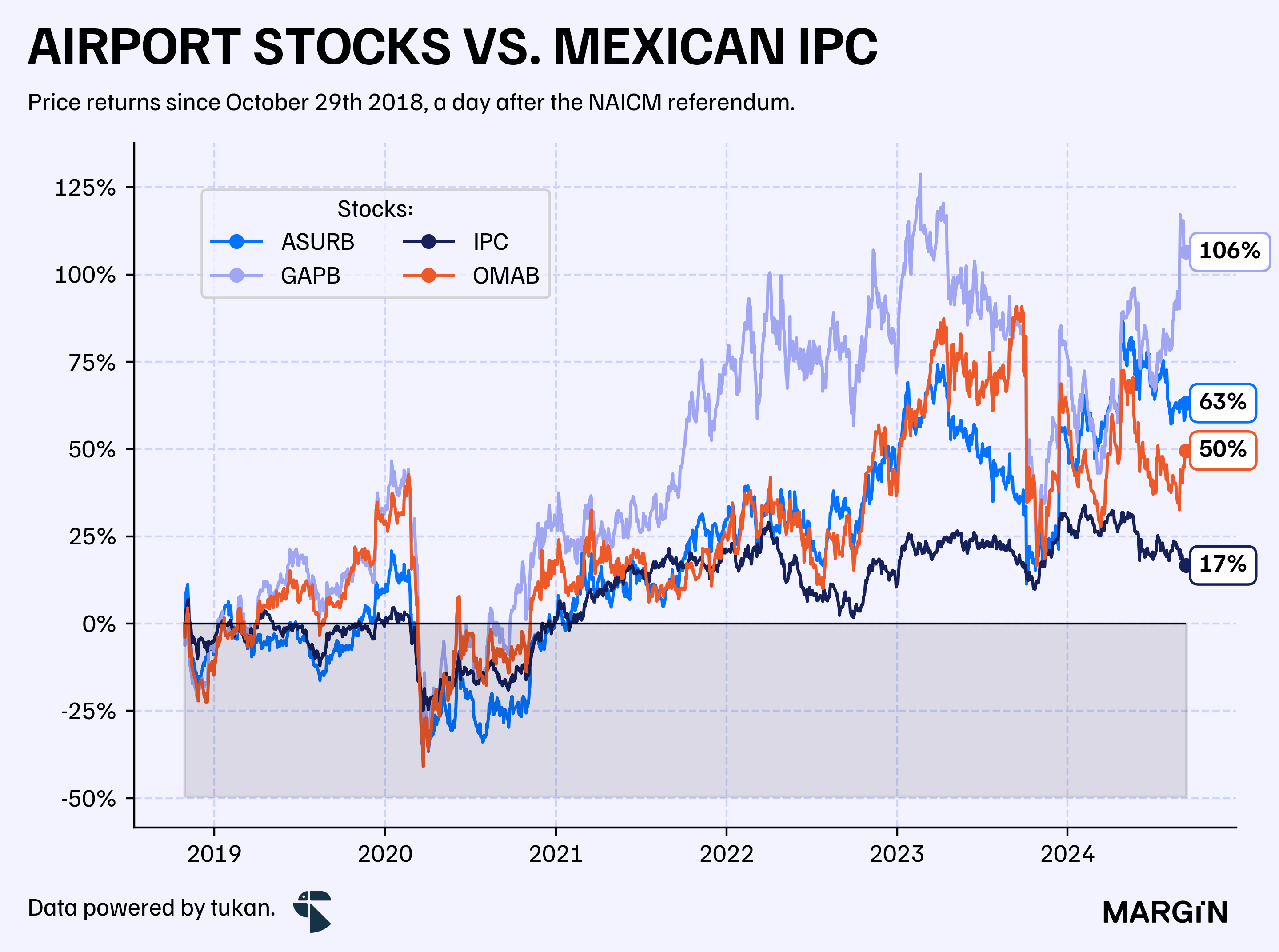

Foreword

Just a few months after the NAICM referendum in late October of 2018, airport operator stocks dropped by more than 15%.

Fast forward to 2024, and all three stocks have achieved annualized returns that surpass 7%, with GAP’s stock demonstrating the best performance of the three (+13% annualized).

What could the market be pricing in the horizon for these companies?

In this report we don’t include data regarding charter flights, which as of 2023, accounted for just 0.4% of total passengers.

Those that carried at least 1,200 passengers per year.

This excludes the AIFA which began operations in 2022.