SOFOMs, An Update

Revisiting Mexican non-regulated SOFOMs (ENR).

One year ago, we published a research piece on non-regulated SOFOMs, Mexico’s largest non-banking financial sector. This article became one of our most widely read pieces on Margin.

For today’s piece, we'll be revisiting this topic, providing updates on the sector’s composition and major players.

Whenever we refer to SOFOMs we’re exclusively talking about non-regulated entities or SOFOMes ENR.

According to data from regulators, Mexican SOFOMs reported a loan portfolio of over $700 billion pesos at the end of 1Q25 — a figure 15% higher than at the end of March of 2024.1

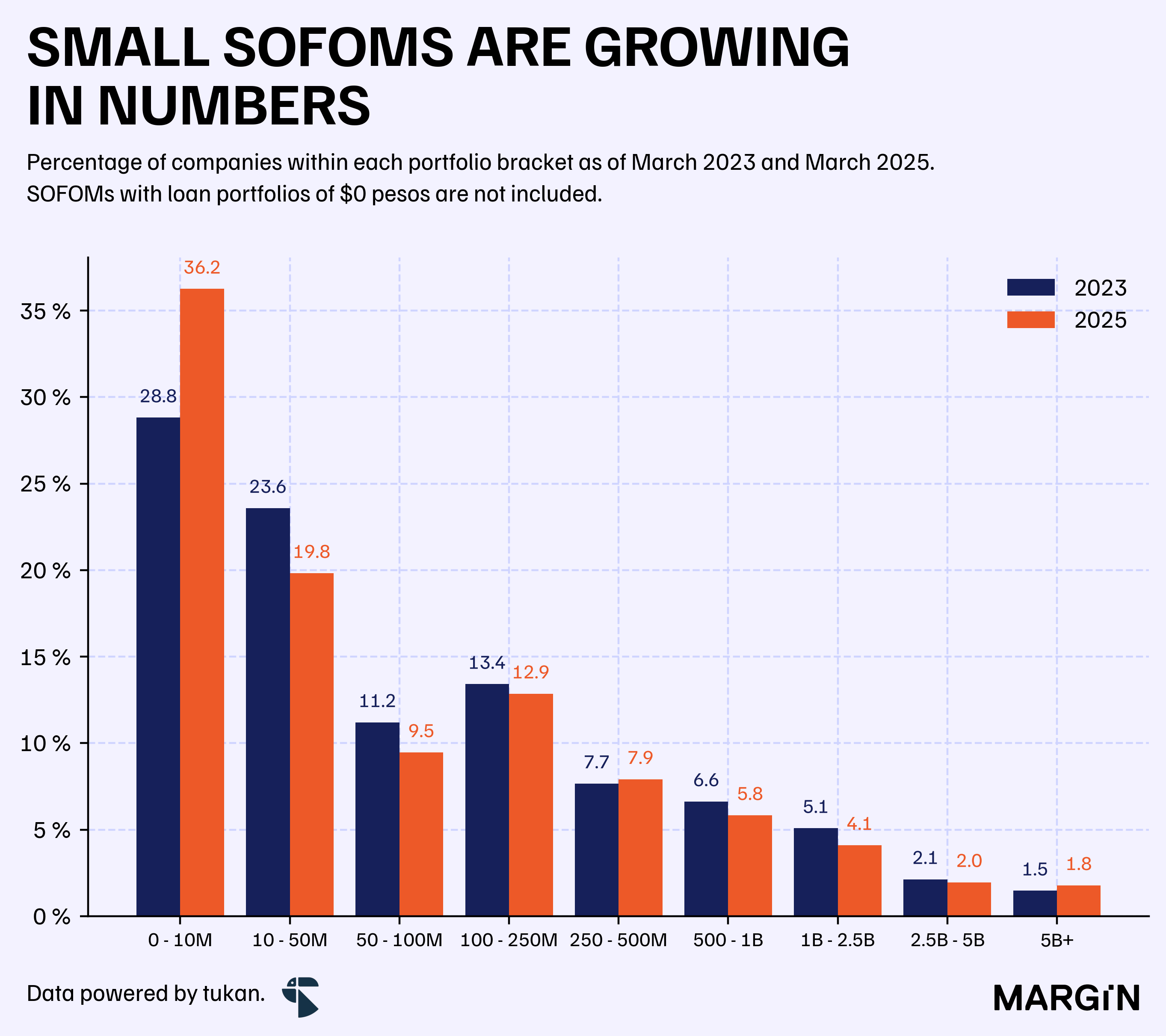

We estimate that close to 1,680 companies were actively in operation at the end of March and close to 580 had loan portfolios exceeding $100 million pesos.

Based on the latest data, we estimate that over 80% of loan portfolio balances would be concentrated amongst the top 9.9% of players — a ratio 2.6 percentage points lower than in 2023 and 2.5 points higher than in 2018.

This would suggest a higher concentration amongst the industry’s largest players, with fewer companies having most of the loans in the market.

Furthermore, we are seeing close to 36% of all companies reporting loan balances below $10 million pesos at the end of 1Q25 — a share that increased by almost 8 percentage points when compared to 2023.

Interestingly, the only other two upward changes in the distribution were across very large SOFOMs (i.e. those with +$5 billion pesos in loans, +0.3 points) and across medium range companies ($250 - $500 million in loans, +0.2 points).

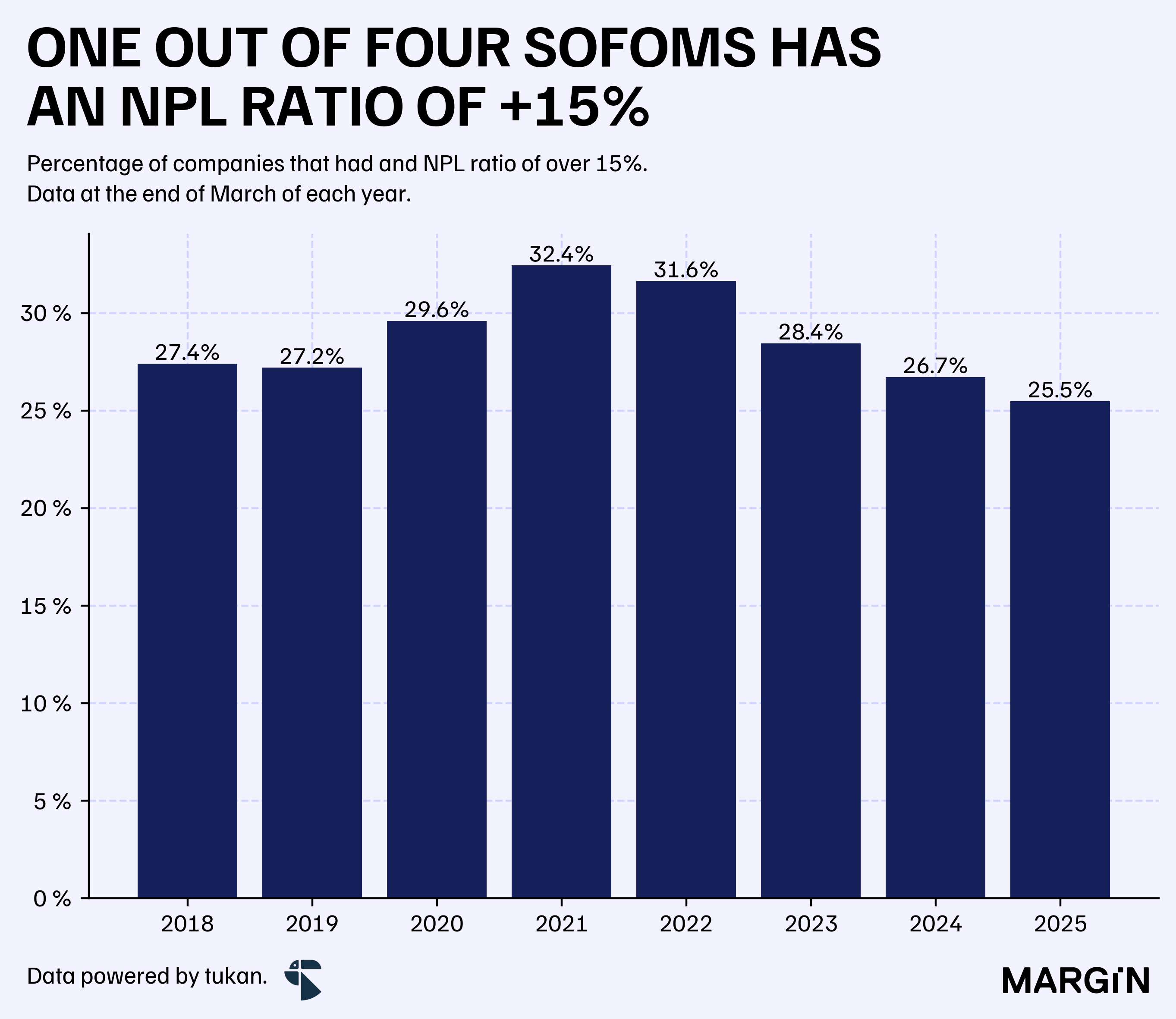

In terms of asset quality, 25% of non-regulated SOFOMs reported NPL ratios of over 15% at the end of March of this year — a figure 1 percentage points lower than the previous year; and one that’s been on a downward trend since reaching a record-high of 32% in 2021.

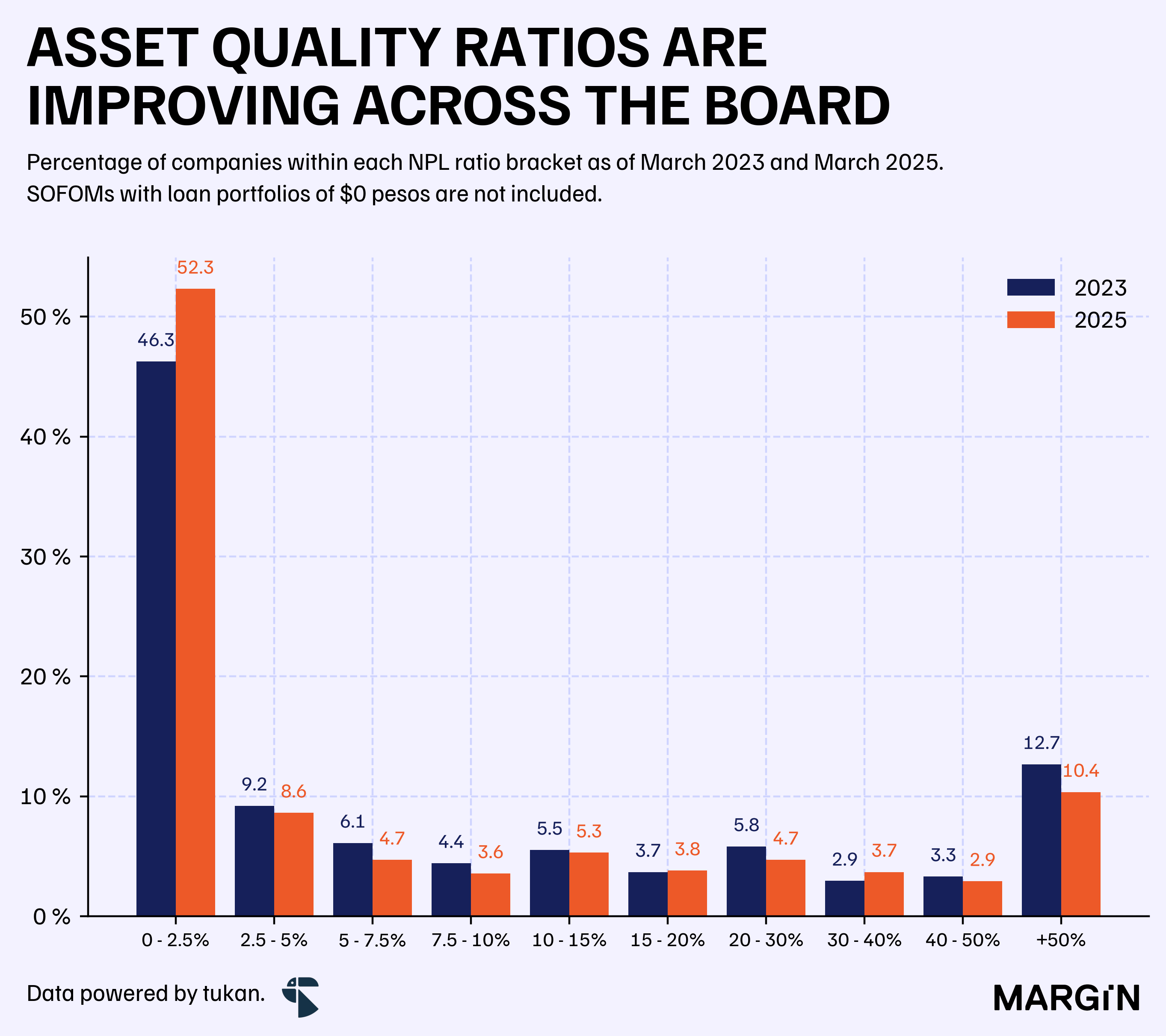

Additionally, we are seeing an increase in the share of companies that reported an NPL ratio below 2.5% — going from just 46% of all companies in 2023 to more than 52%.

Another positive note is the contraction in the share of SOFOMs with NPL ratios surpassing 50%, a statistic that went from ~13% in 1Q23 to 10% in 1Q25.

In terms of growth rates, we saw 29% of companies (with +$100 million pesos) in loan portfolios grow at high single-digit rates2 during the first quarter of this year and 22% of companies recording over double-digit growth rates (on a quarter over quarter basis).

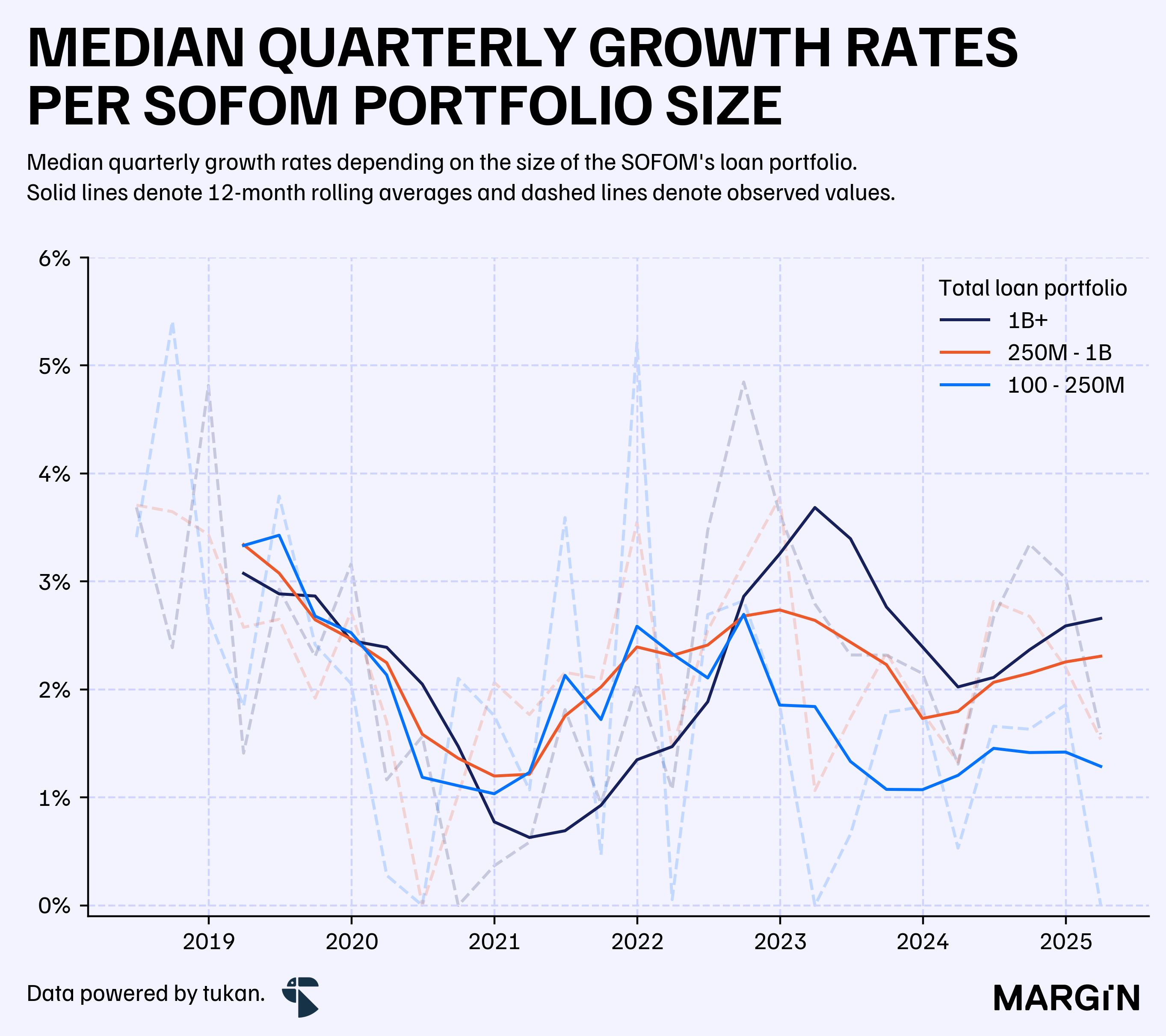

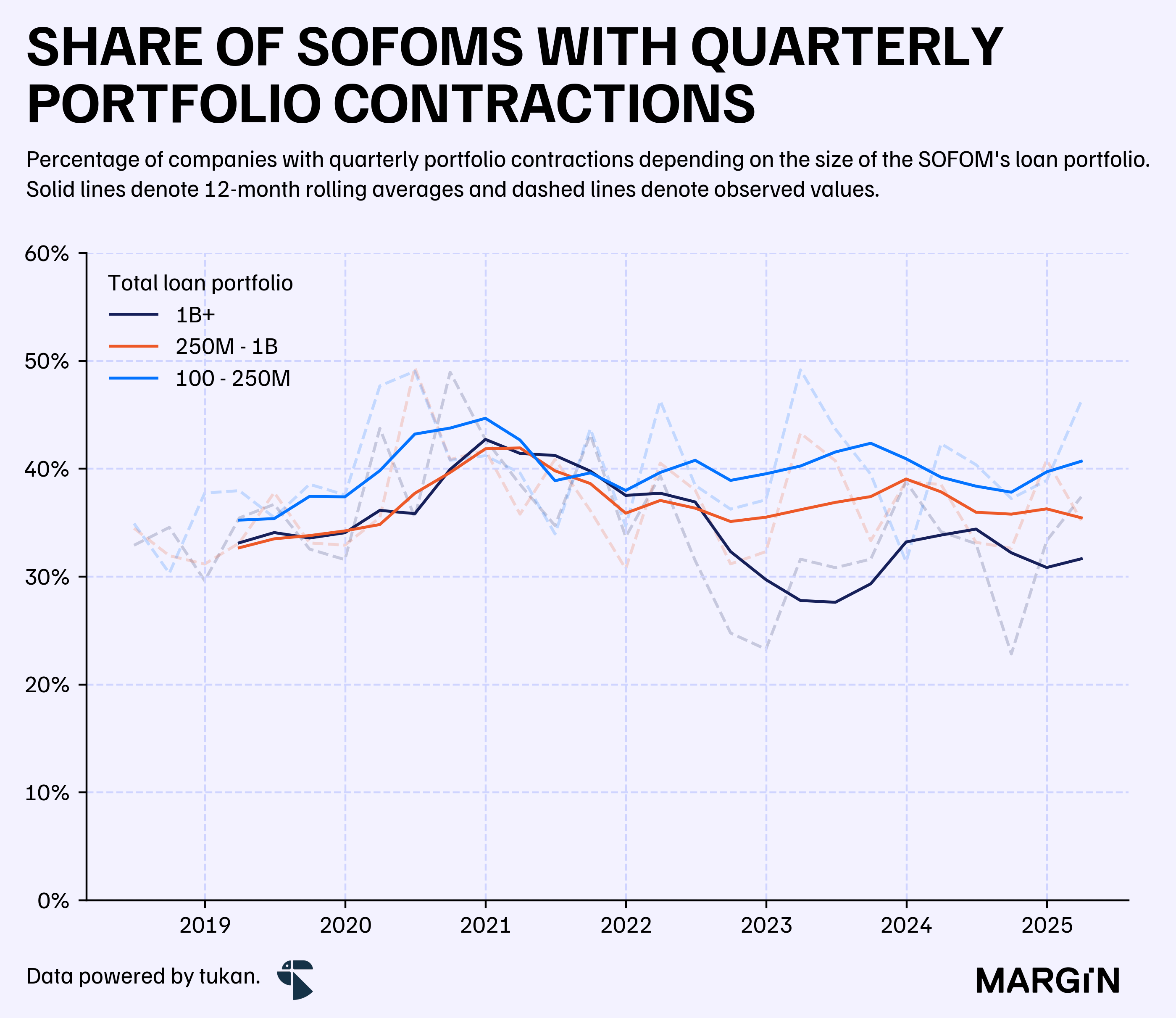

Since the end of 2022, SOFOMs with more than $1 billion pesos in total loans have been growing faster than smaller companies. In fact, the adjusted “spread” between growth rates of large financieras and smaller businesses ($100 - $250 M) has been of over a percentage point during the most part of the last two years.

Furthermore, we saw 42% of businesses reporting contractions in their loan portfolios when compared to 4Q24.

Again, when compared across the size of the company’s loan portfolio we can see that a higher share of smaller SOFOMs have seen contractions across their balances versus the industry’s largest players — with the gap widening, especially, after 2023.

“Tres comas”

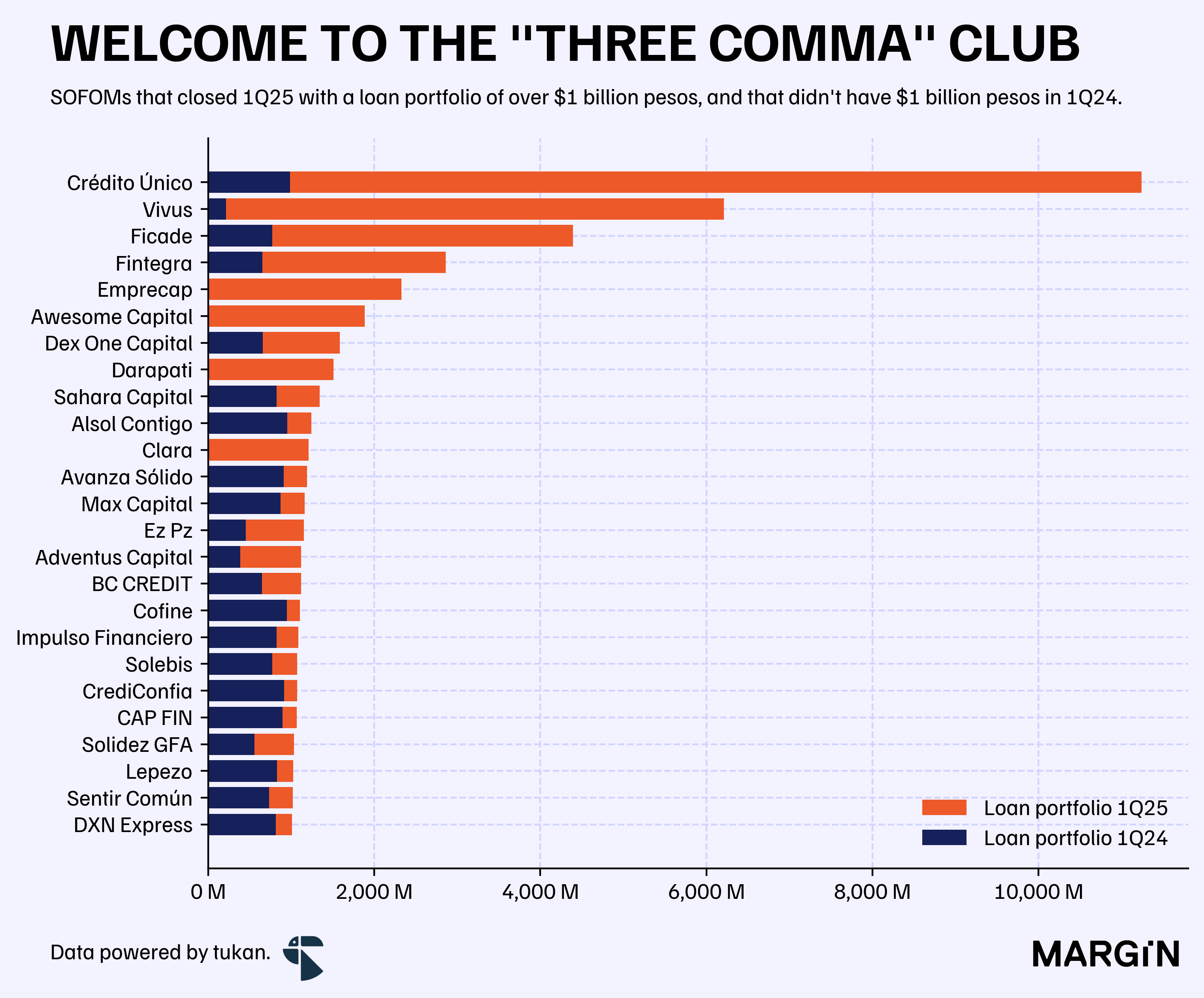

The latest data from regulators shows that there are over 133 companies with over $1 billion pesos in total loans — implying 10 (net) additional companies than in March 2024.

The following chart shows those companies that entered the “three comma” club during the past 12 months.

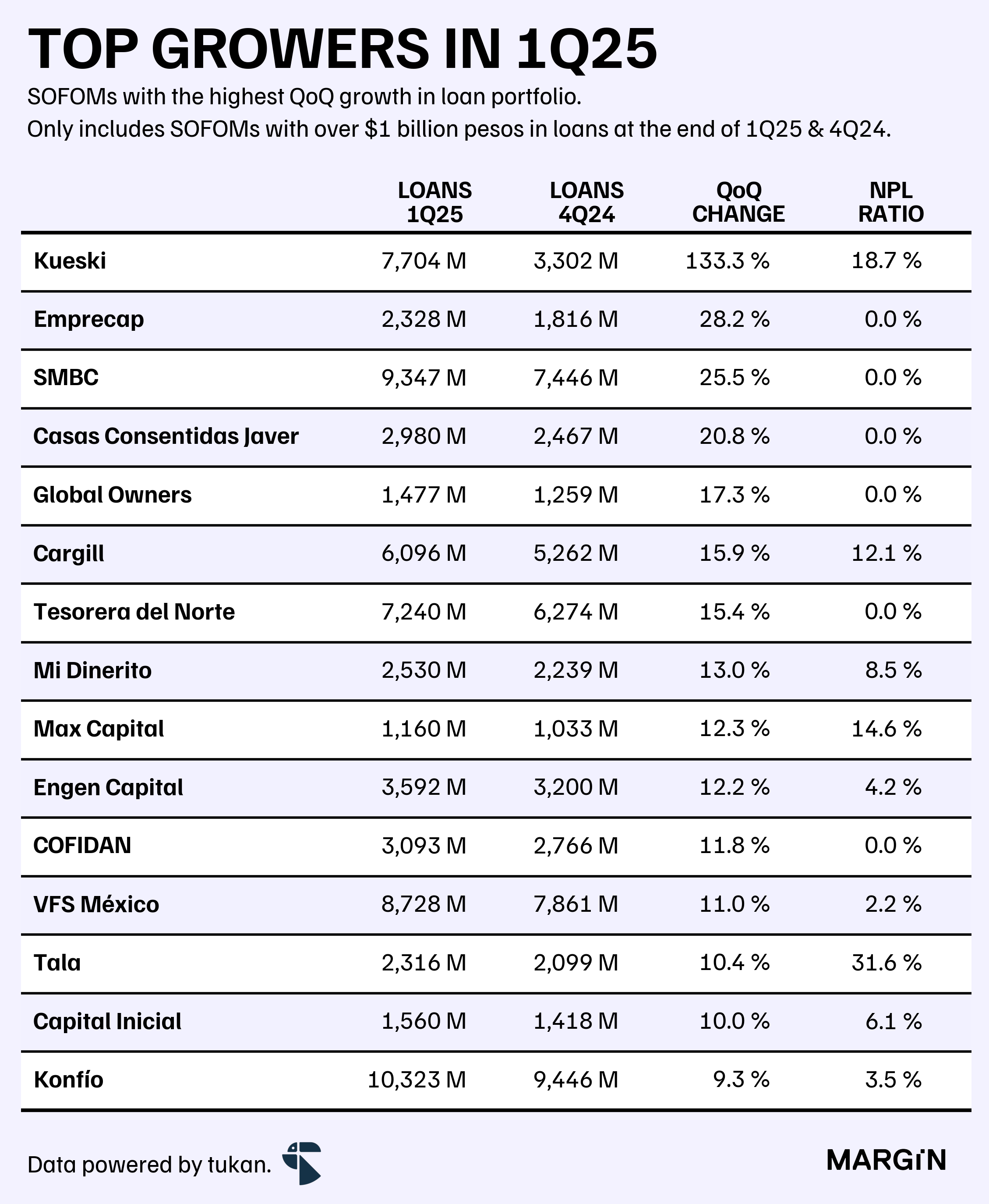

And here are those businesses, within this subset, that grew the most during the past three months.

We highlight fintechs Kueski and Konfio who posted impressive results during the first quarter of the year; as the former recorder over +130% increases in just three months and the latter crossed the $10 billion mark at the end of March.

The median quarterly growth rate for companies in this subset was just shy of 2% during the first quarter of the year. Meanwhile, 41% of companies reported contractions in their loan portfolios when compared to 4Q24.

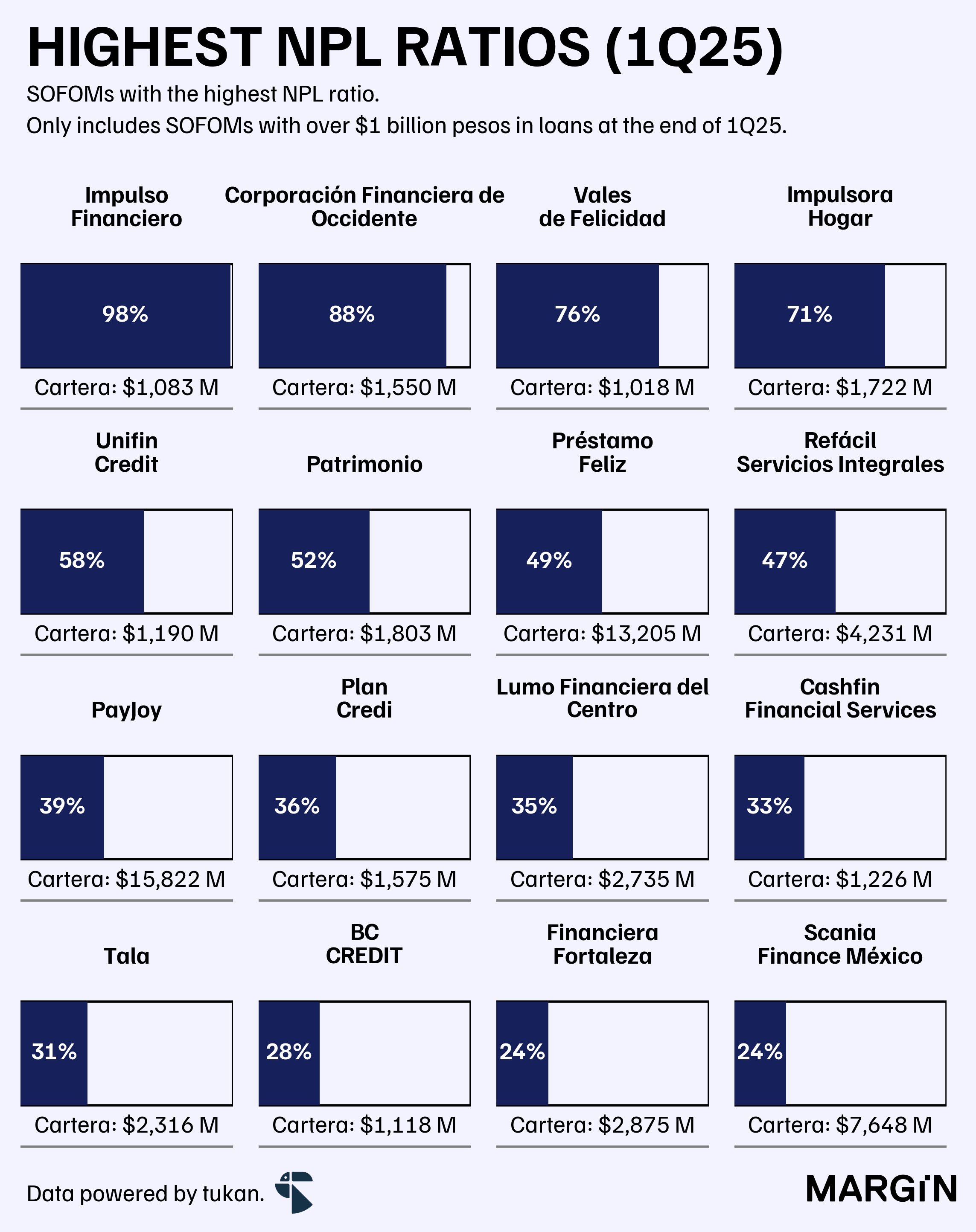

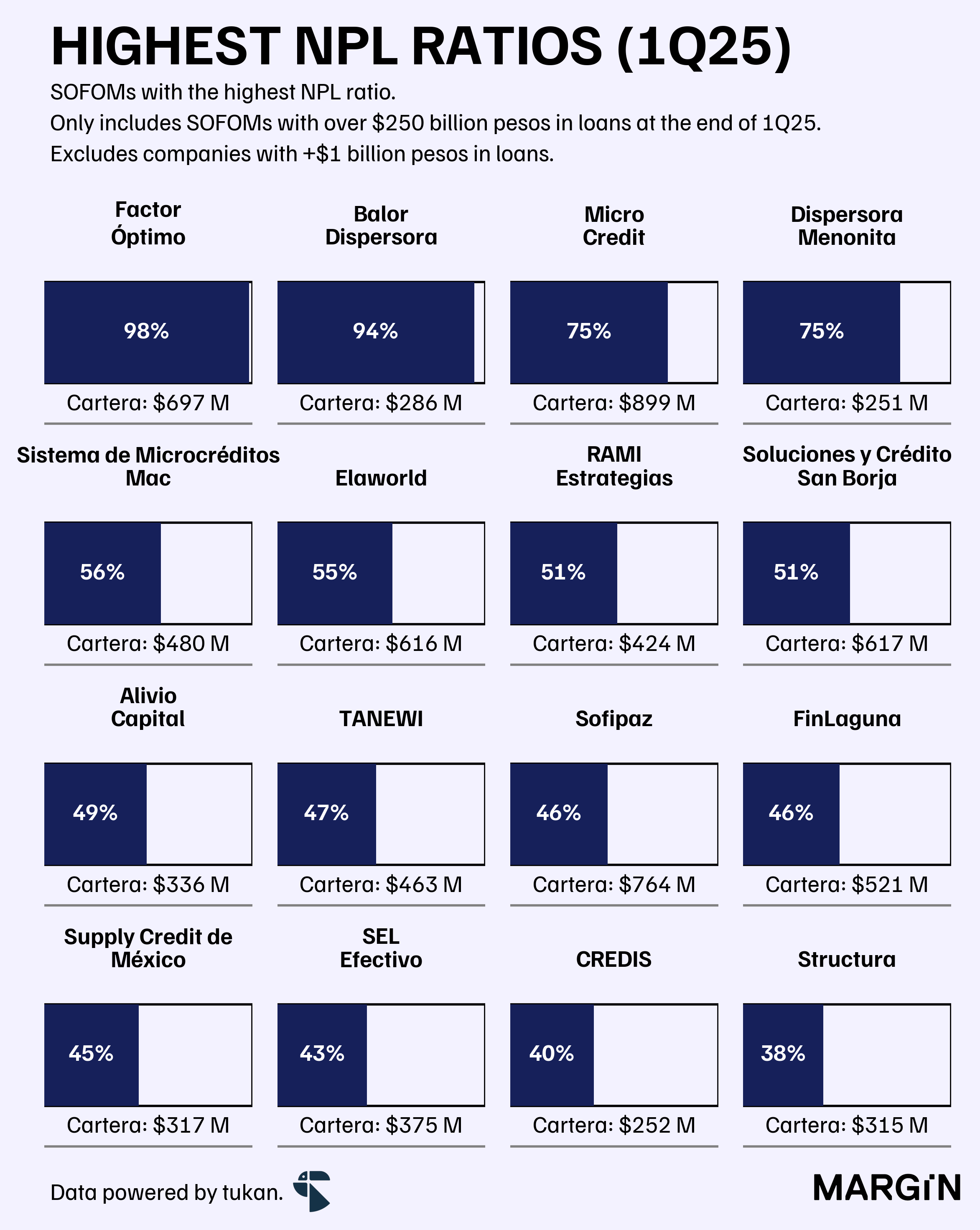

Then we have those companies that had the highest NPL ratios at the end of the quarter. As can be seen on the chart below, Impulso Financiero, a company that joined the “three comma club” during the past 12 months reported almost all of it’s loan portfolio as in default according to official sources.

The median NPL ratio for the 130 companies in this group was of 2.8% at the end of 1Q25.

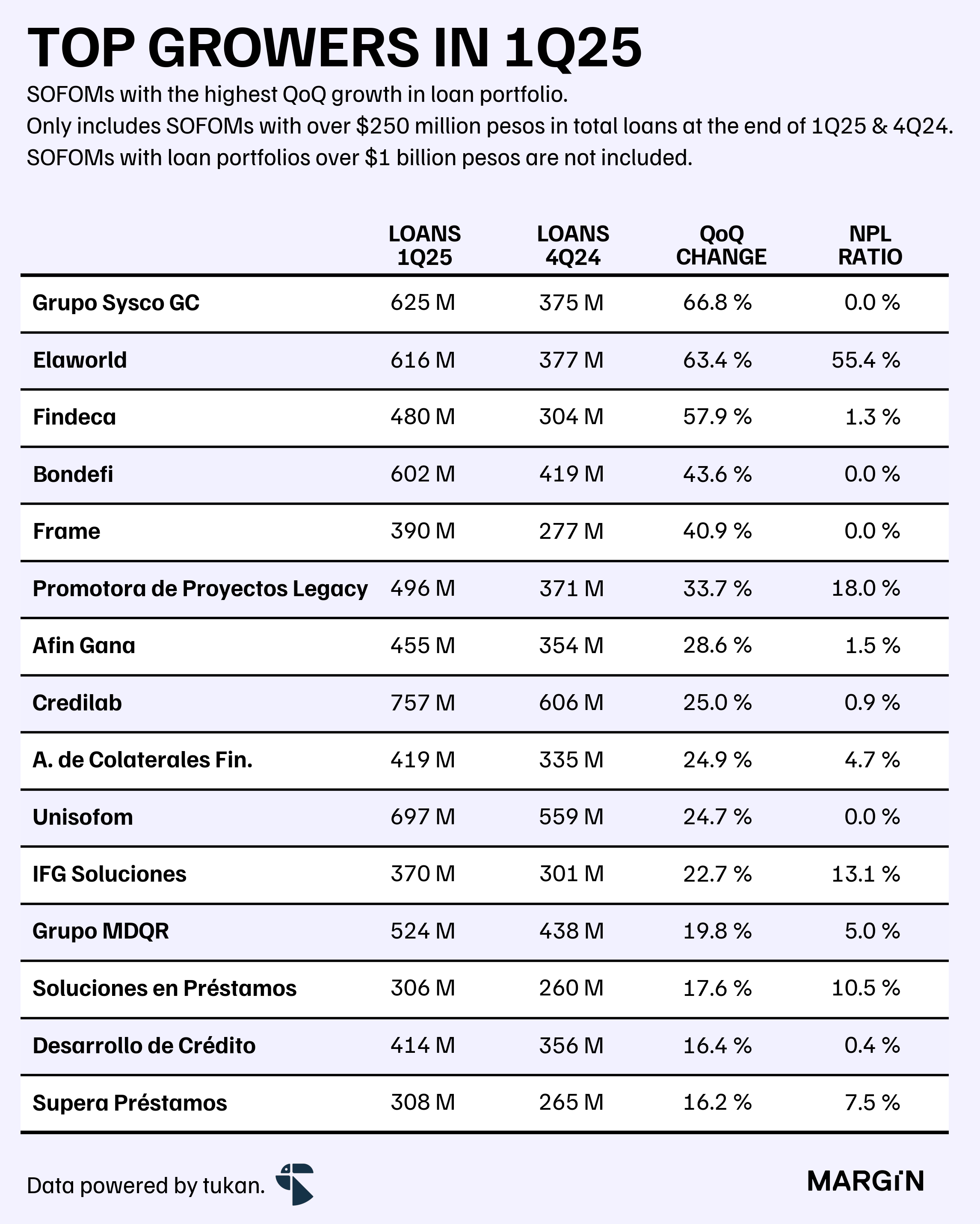

+$250 million

On the other end we have 231 companies that reported having over $250 million pesos and $999 million pesos in total loans.

The median quarterly growth rate for this set of companies was close to 2% for the first quarter of the year, and close to 38% of businesses recorded contractions across their loan balances. Furthermore, there were 31 companies (i.e. 15%) that posted double-digit growth rates during the first three months of 2025.

In this “bucket” we found that the median NPL ratio closed the month of March at around 2.8%, and that around 16% of companies in this space reported NPL ratios surpassing 15%.

We’ve had to adjust portfolio figures for some companies due to major inconsistencies across the dataset.

Over 5% QoQ growth.