Stalled

Housing construction in Mexico doesn't seem to recover. What's going on?

If you take a quick look at Mexico’s construction GDP figures, you’ll notice that overall construction output in the country is now 9% higher than 2023 figures (as of 2Q24) and hovering at all-time highs.1

However, not all is great for most construction companies in the country. According to INEGI data, most of this growth has been driven by a significant increase in heavy and civil engineering construction projects — a sector that has seen production rise at a CAGR of 12% during the past five years. Residential, commercial and industrial development GDP, on the other hand, recorded a negative CAGR during the same timeframe, bringing the sector’s share on overall construction output to all-time lows.

Despite the overall negative CAGR for the standard construction sub-industry; the country’s official economic data suggests a major slowdown on housing developments. When compared to the first semester of 2019, and based on non-inflation adjusted figures, housing development has remained flat; whereas industrial & commercial construction projects have risen by more than 34% as of June 2024.

Not only this, but we are seeing housing production (in number of housing units) at all-time lows; particularly in low and medium income housing projects.

For the more than 6,000 companies that focus on housing construction projects, the data seems to paint a bleak picture. Let’s break it down.

The Foundations

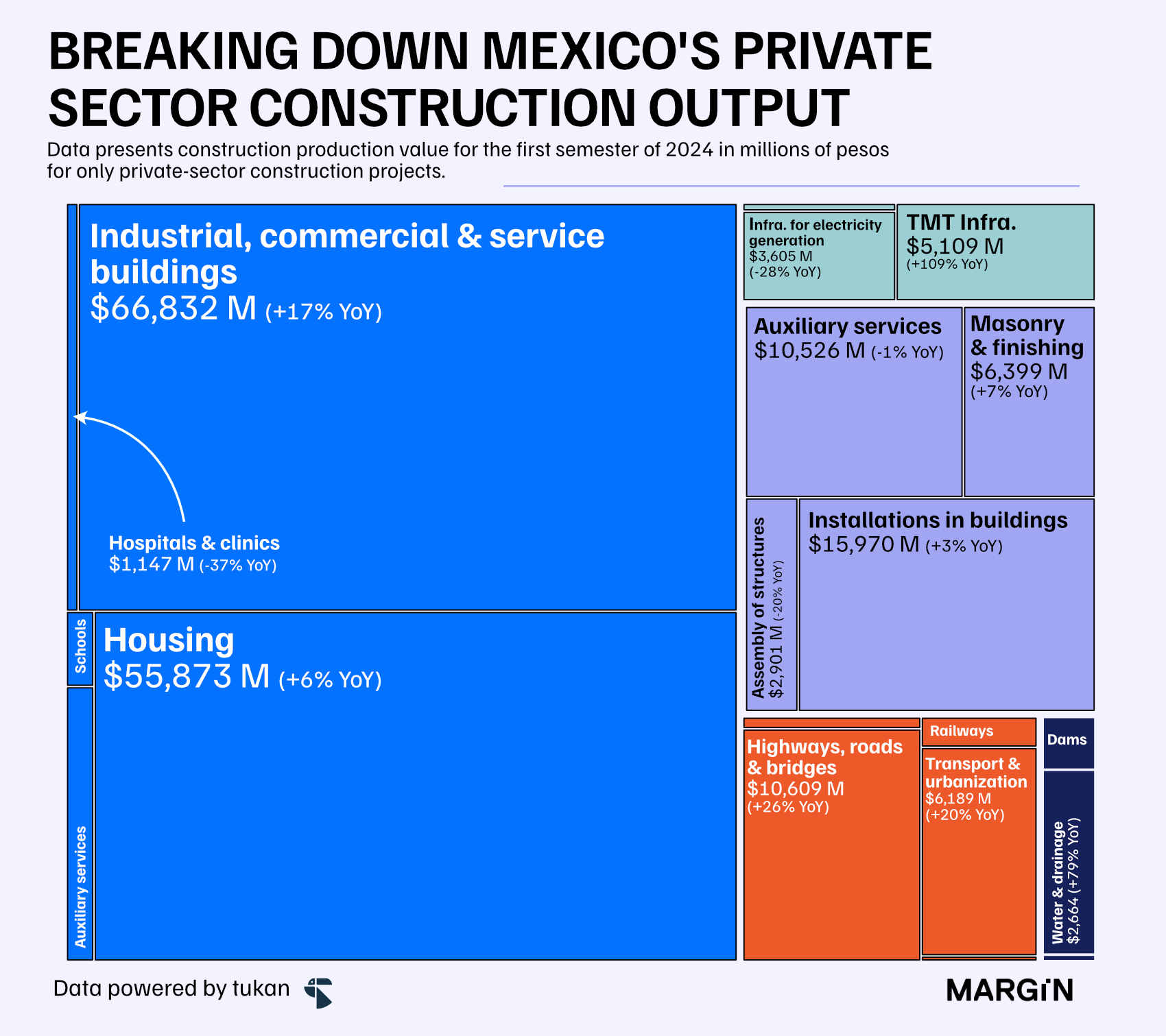

According to the latest INEGI construction survey figures, the industry’s production value amounted to more than $337 billion pesos during the first six months of 2024 (+12% YoY). Out of these, 57% were produced by the private sector (+11% YoY) with the remaining 43% generated by government funded projects (+13% YoY).

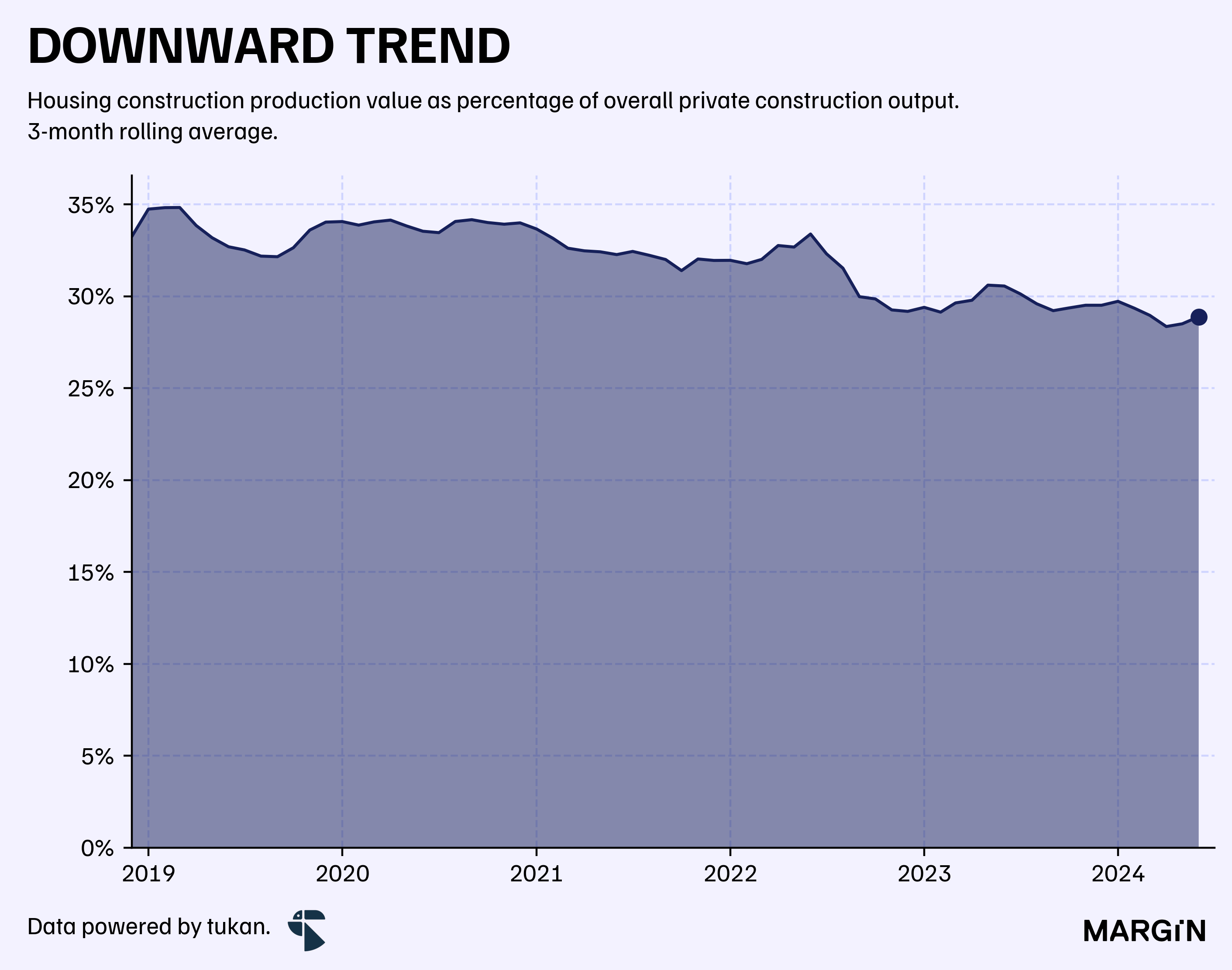

Zooming into the country’s private sector projects, we find that commercial, industrial and service development continues to be the major player for the Mexican construction industry at 35%; followed closely by housing construction works with 29%.

As stated earlier, the housing construction industry has been consistently losing ground to other construction projects and developments. To give a sense of the long term impact, residential development accounted for 34% of total private construction output in 2018 — a figure 5 percentage points higher than in 2024.

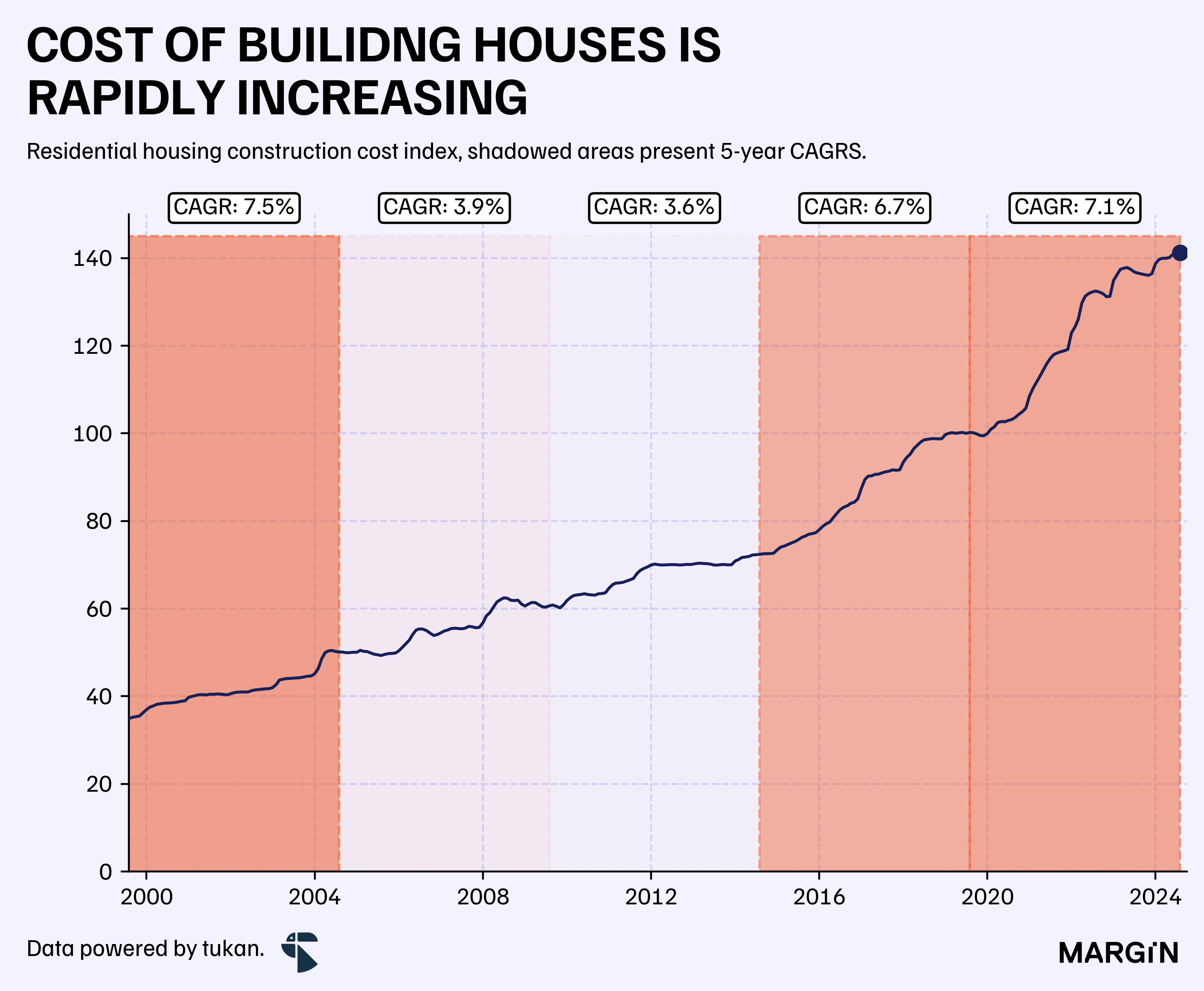

To add salt to injury, housing developers have been facing important pressure from rising construction costs. According to INEGI data, residential construction costs have been increasing at a 7.1% 5-year CAGR — the highest long-term growth rate for the index since 2004.

This means that the cost of building a house has risen by more than 40% in just 5 years. Most of this increase has been propelled by a 7.3% CAGR on material costs, followed by 6.3% on labor prices and finally a 4.2% rise on machinery and equipment.

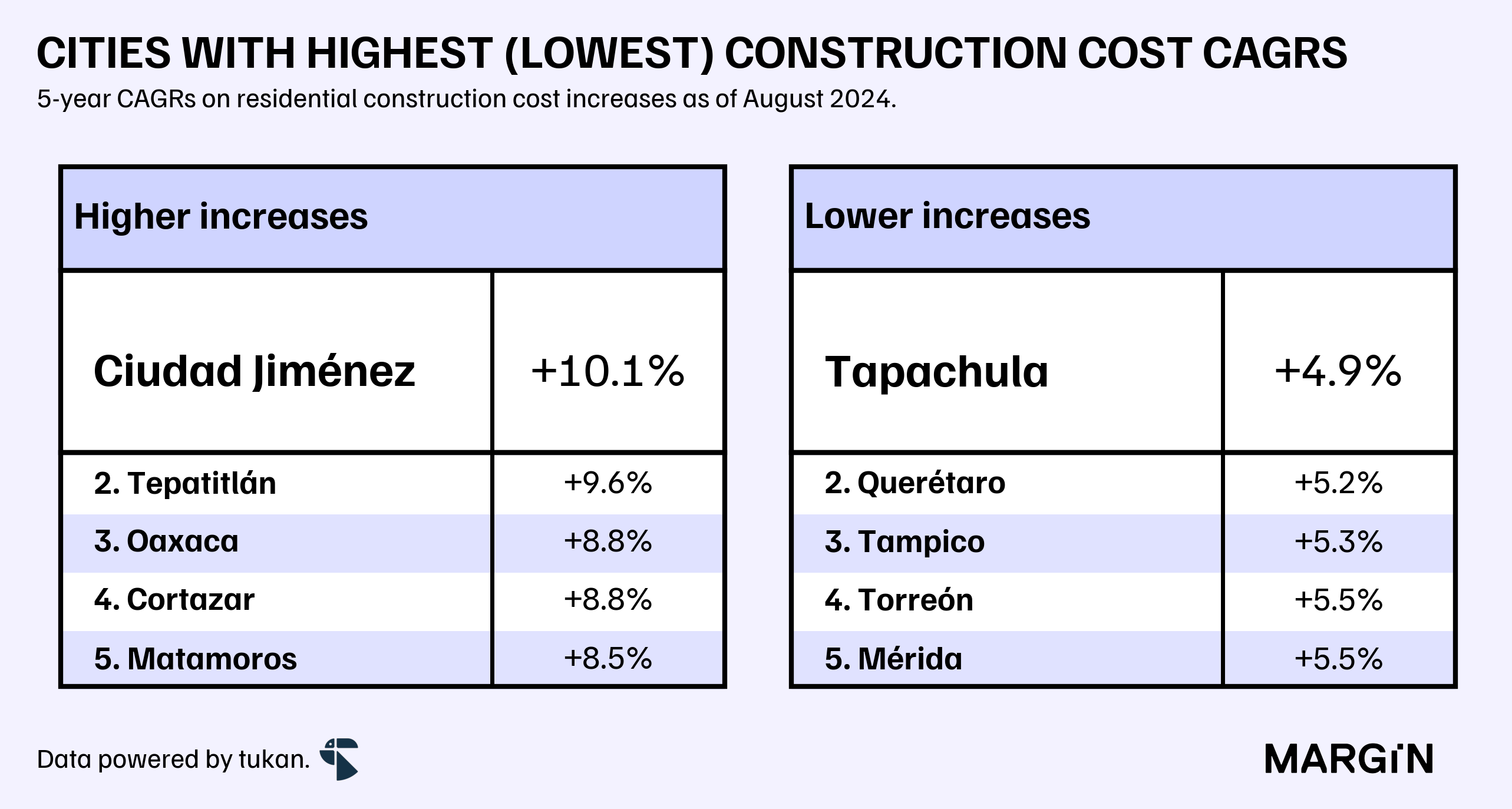

In some cities, such as: Ciudad Jiménez (Chihuahua), Tepatitlán (Jalisco), Oaxaca and Cortazar (Guanajuato) the rise has been even more daunting; surpassing 8% average growth rates since 2019.

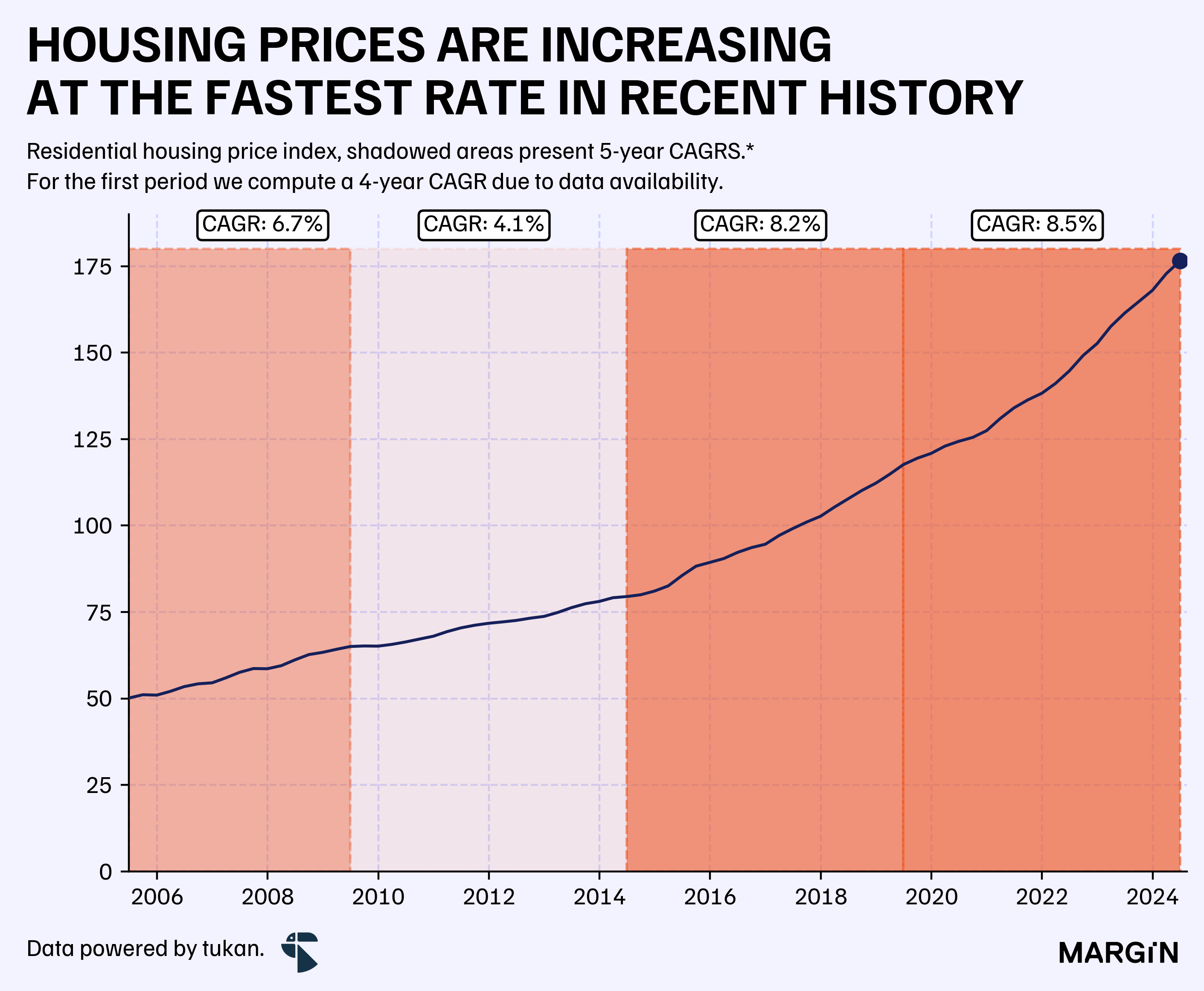

This has directly translated into higher housing prices for consumers at an unprecedented rate. According to data from the SHF (Sociedad Hipotecaria Federal), housing costs in Mexico increased at a CAGR of 8.5% in the country during the past 5 years. Again, the highest long-term growth rate for the index since the SHF publishes data.

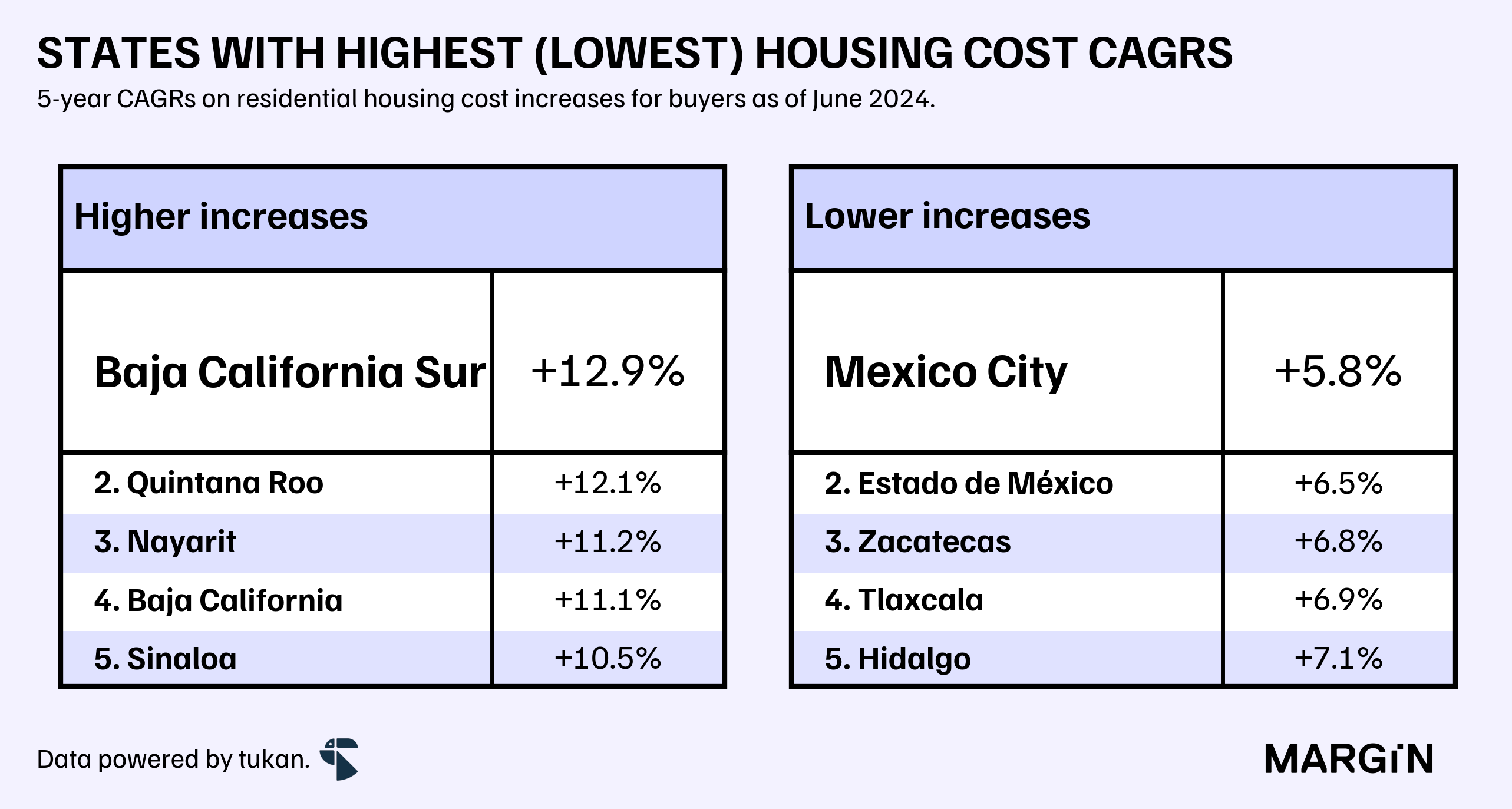

At a state level, Baja California Sur leads the way as the most-pressured state in terms of rising housing prices at a 13% CAGR; with the northern state being followed closely by Quintana Roo in the south with a 12% CAGR.

Mexico City, surprisingly, boasts the lowest increase in prices for the country.

For reference, a 13% 5-year CAGR equates to a total increase of 84%.

How does this reflect on the number of housing units being produced?

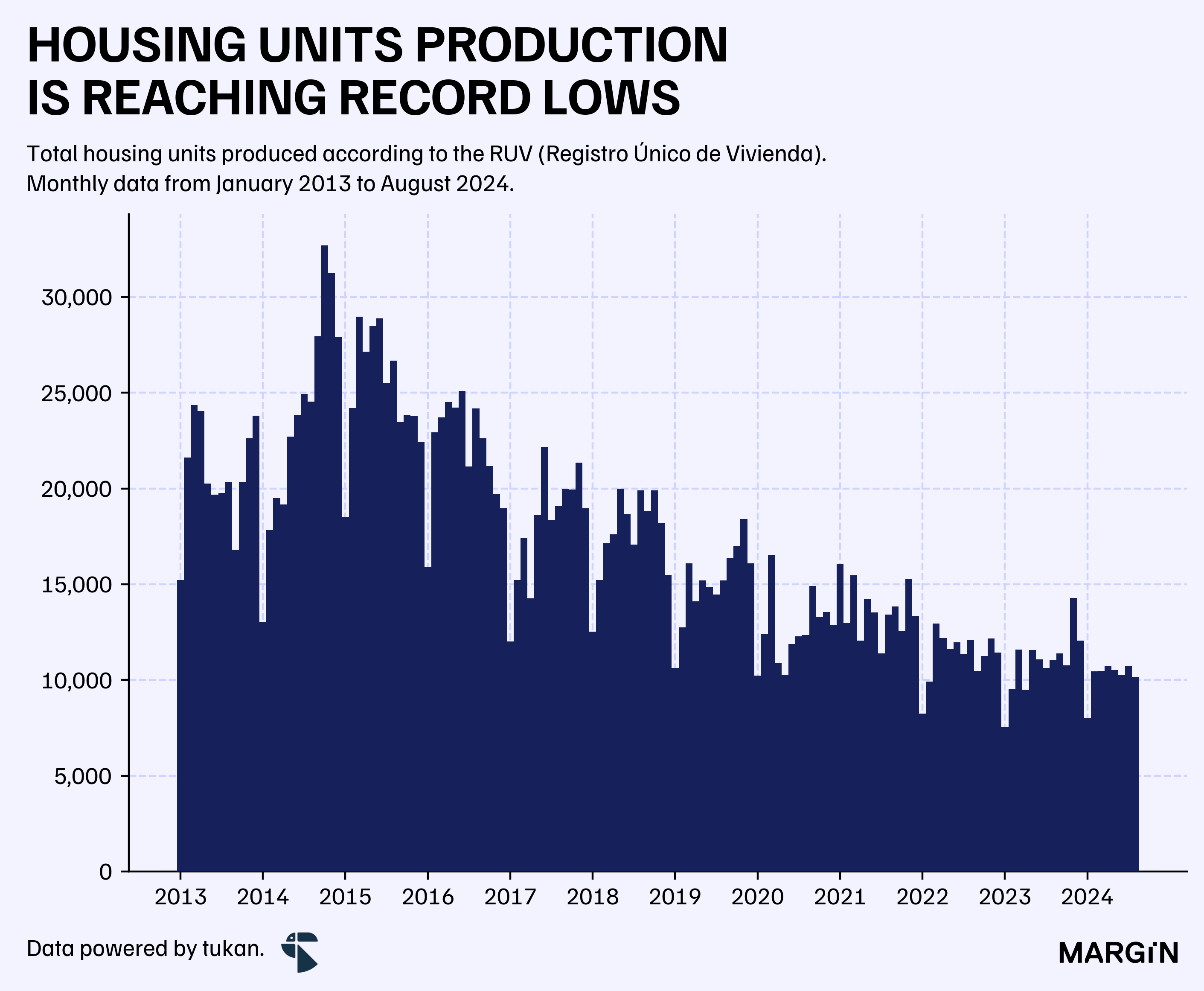

According to the Registro Único de Vivienda (RUV), the official registry for housing developers in Mexico, the production of housing units in the country has been on a downward trend since 2013. Recording just shy of 131 thousand units in 2023, the lowest for a single year in the past decade, and half of what was produced in 2016.

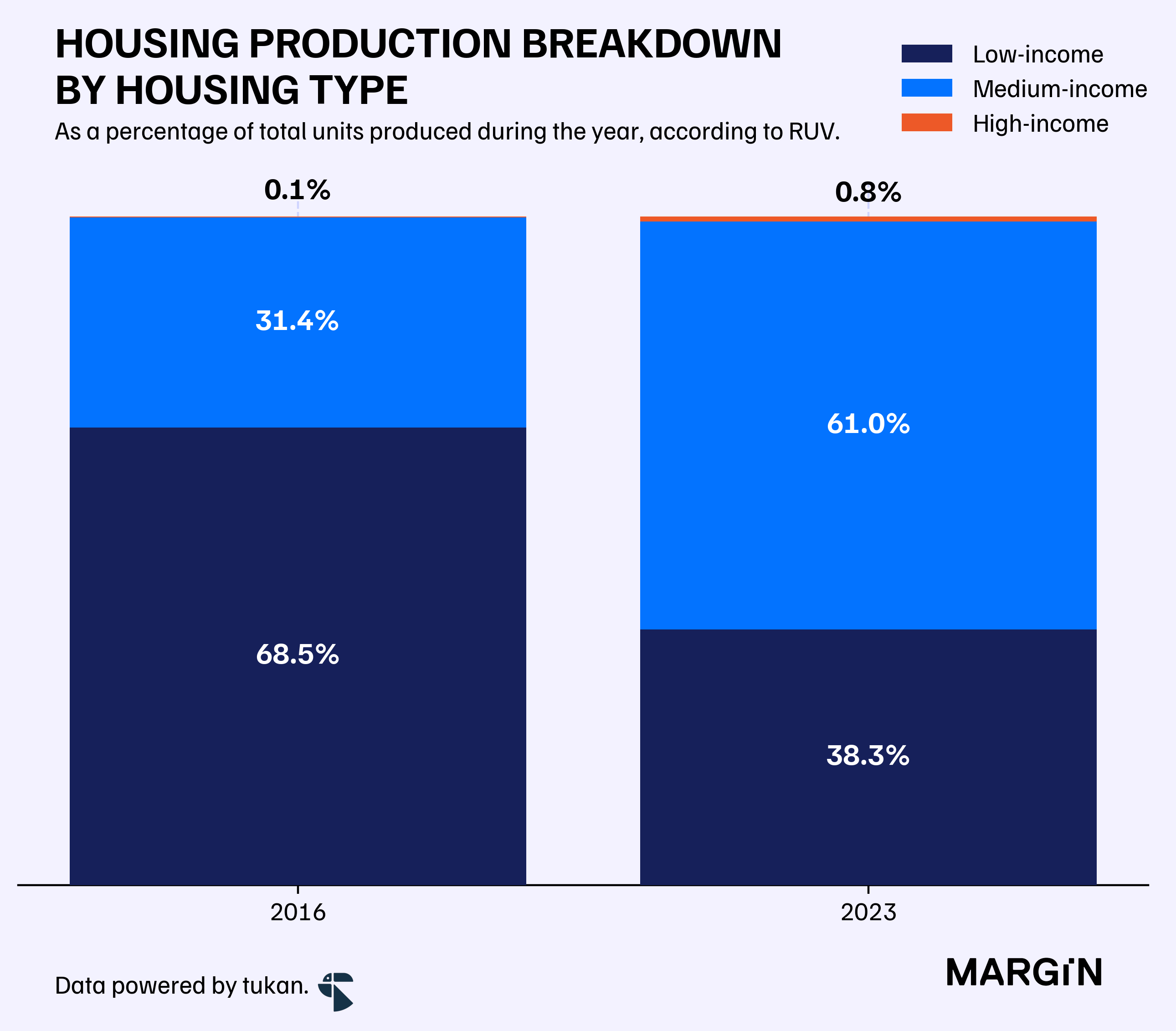

Furthermore, most of this impact can be directly seen on lower income housing developments. For example, in 2016, close to 68% of total housing production (in number of units) were tied to lower income housing projects — a percentage that has now declined to just 38% of units “produced”.

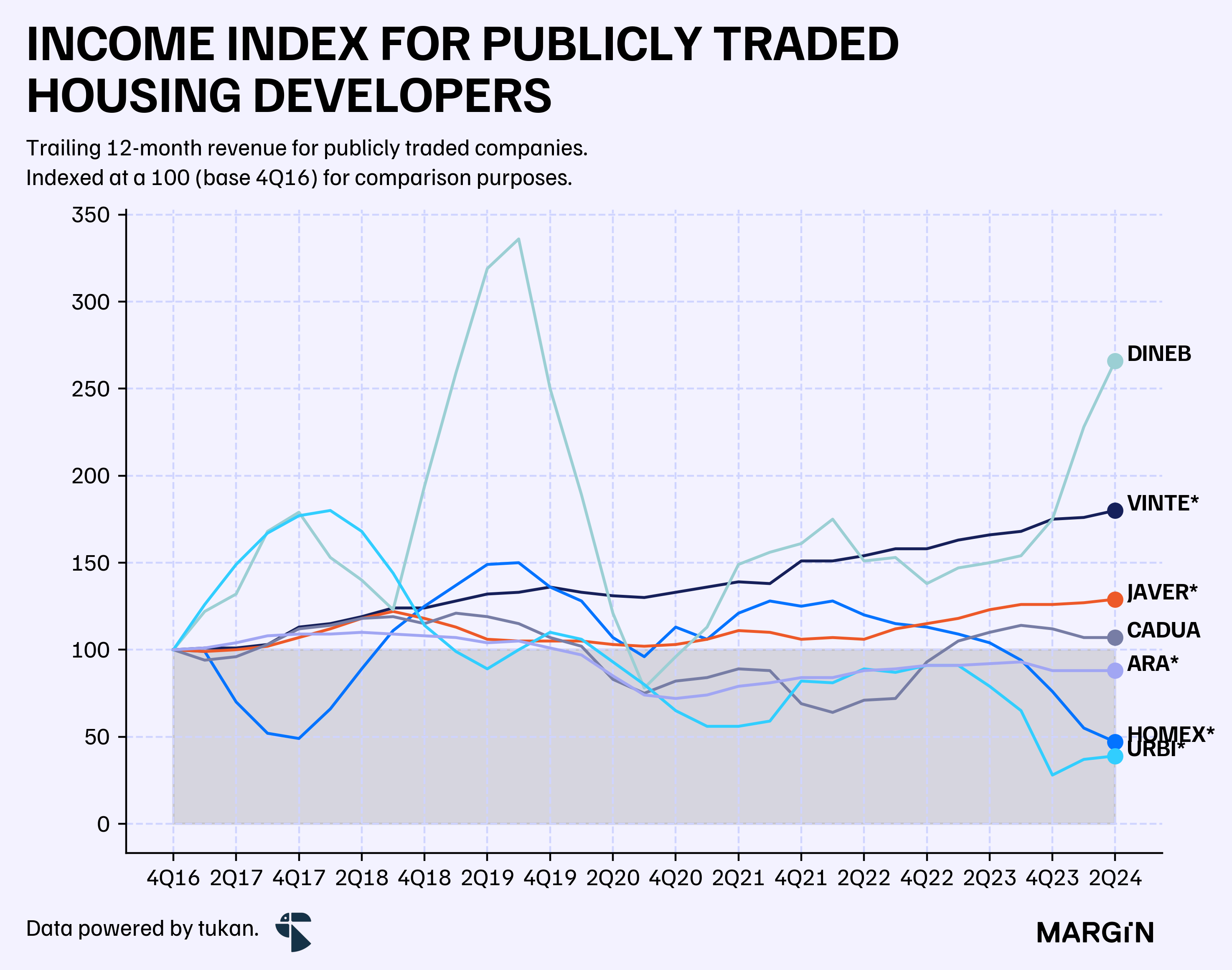

Finally, what does the data show for publicly traded companies in the space?

In total, the 7 companies focused on housing developments that trade on the Mexican Stock Exchange2, reported trailing 12-month income just shy of $30 billion pesos — a figure 6% higher than the one recorded at the end of 2Q19 (12-month trailing revenue).

Out of the six companies, just DINE and VINTE, recorded revenue CAGRs of over 5% since the end of 2016. Two of them, URBI and HOMEX, are reporting income figures almost half of what they had reported eight years ago.

Overall, experts believe the “housing supply crisis” in the country could be attributed to multiple factors, such as: rising construction costs, low financing opportunities to real-estate developers, government bureaucracy, and high-interest rates. A set of factors that seem to be affecting the housing supply not only in Mexico, but at a global scale.

In Mexico, will we see the industry recover during the next couple of years? Or will the housing construction segment remain stagnant?

In constant prices, i.e., adjusted by inflation.

VINTE, HOMEX, JAVER, CADUA, DINE, URBI and ARA.