Tight

Thoughts on credit card profitability.

Credit cards are often considered the primary entry point for consumer financing, especially for fintechs and non-traditional financial companies aiming to compete in this space.

In most cases, new market entrants tend to incur losses—a phenomenon typically attributed to the “training” of sophisticated risk models, significant marketing expenditures, and high customer acquisition costs (CAC). These efforts are justified by the expectation of future profitability as CAC stabilizes, risk models reduce the probability of default, and the growing customer network enables the introduction of additional financial products, such as payroll and personal loans.

But how profitable are credit cards as a standalone product? And what insights can we draw from the regulatory data published by commercial banks?

For non-traditional finance companies, we recommend revisiting our deep dive from a few months ago on Liverpool’s credit card business.

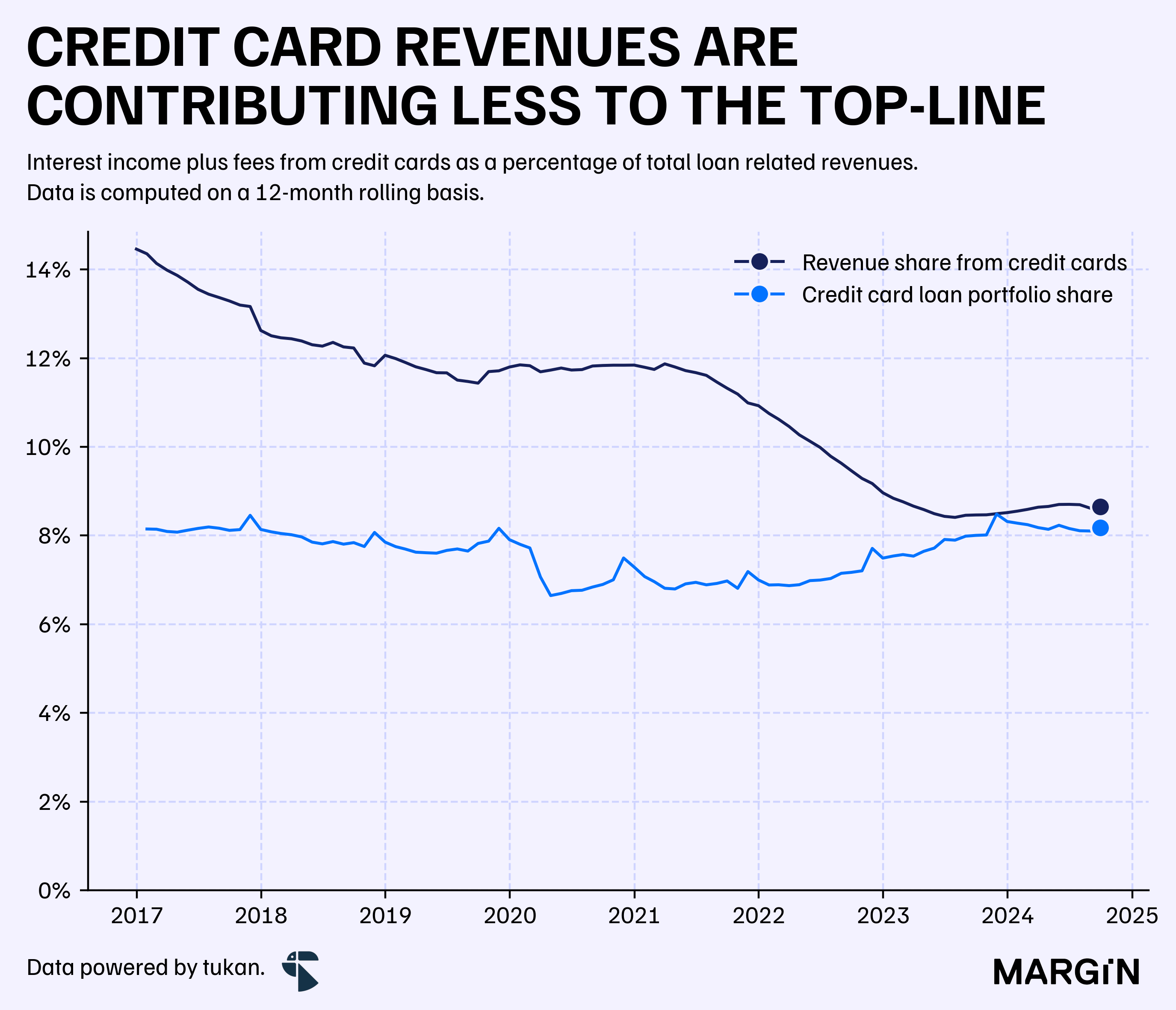

Over the past 12 months, credit card income accounted for just 8% of total loan-related revenues for commercial banks in the country. This figure marks a record low since the CNBV began publishing data on the subject.

This is particularly surprising given that credit card portfolios (as a percentage of total loans) have remained relatively stable over the past seven years. However, the “revenue share” has declined by more than five percentage points during the same period.

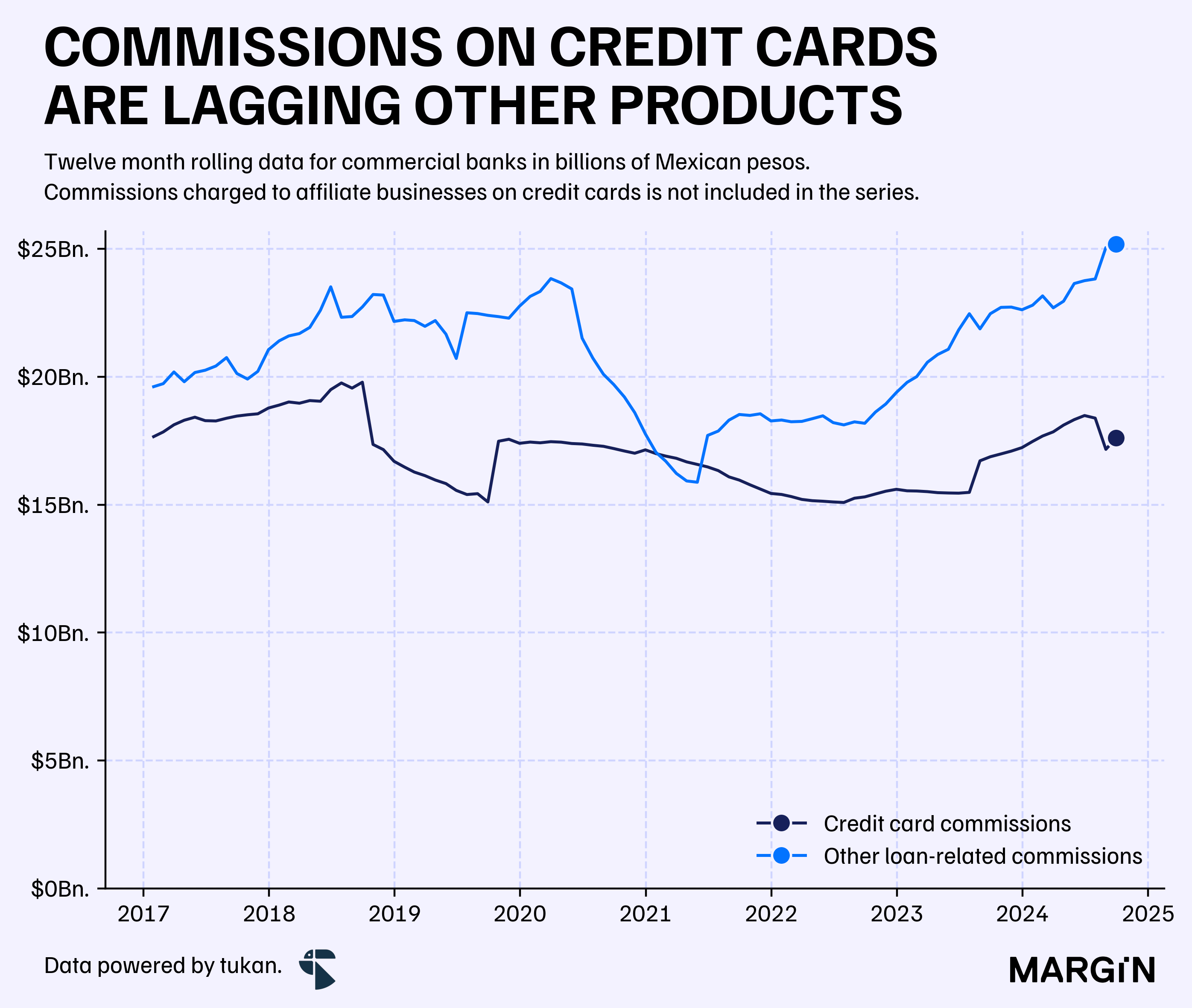

This decline is largely driven by a significant contraction in commissions as a key revenue source for credit card products. To illustrate the impact, commissions charged to credit card holders made up nearly 17% of total credit card revenues for banks in 2017—a figure that has now fallen to just under 11%.

In our previous article exploring competitiveness in the credit card market, we highlighted that many banks have stopped charging annuity fees to consumers. Additionally, the market has consistently grown more competitive in recent years.

We believe this “overcrowding” has forced banks to reduce commissions as a strategy to attract and retain customers, with the hope of eventually compensating for these lost revenues through interest generated on issued credit cards.

Notice how in 2017, commissions from credit cards only lagged tariffs on other loans by a margin of 10%; a gap hat has now widened to more than 30%.

On the other hand, credit card loan loss provisions—i.e., the amount banks allocate from their balance sheets each month to cover expected losses—remained near all-time highs in September.

This marks the third consecutive month in which expected losses for credit card debt have exceeded the MXN $6 billion threshold, a first since the CNBV began publishing data on this metric.

For reference, between 2020 and 2022, we only observed two months with over MXN $6 billion in loan loss provisions for the commercial banking system.

This trend could be partially explained by the remarkable overall growth of credit card portfolios in recent years and regulatory changes within the banking sector. However, recent data suggests that provisions have been increasing at a significantly faster pace than loan balances.

According to CNBV data, since the start of 2023, provisions for expected losses on credit card products have been growing at an average monthly rate of 2.1%—nearly double the growth rate of the credit card portfolio itself.

To put this in perspective, a 2.1% monthly average growth rate translates to an annual expansion of over 28%, which is 13 percentage points higher than the annualized portfolio growth rate of 15%.

Now that we’ve explored the key trends in the credit card market, what can we infer about the product’s profitability? And how have these trends impacted some of the major banks operating in this space?

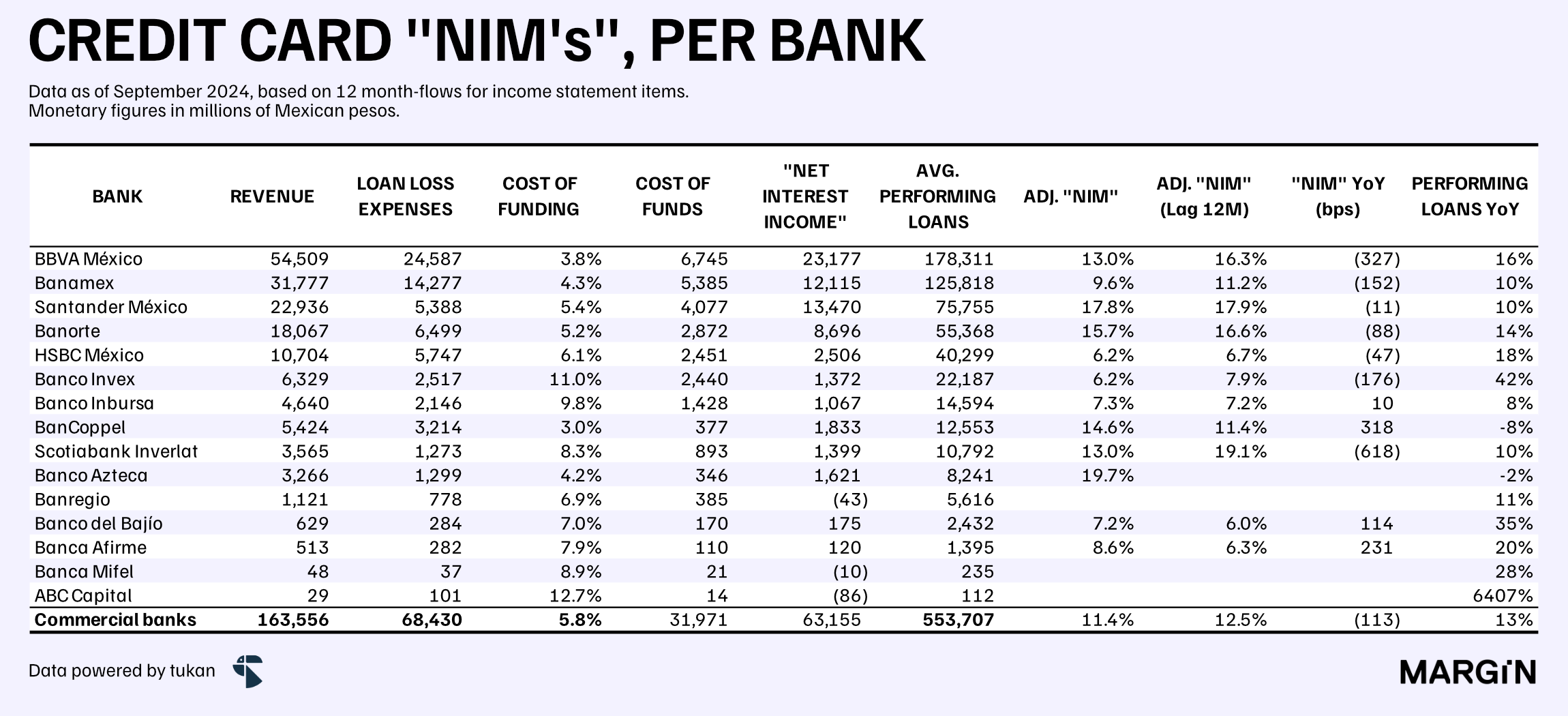

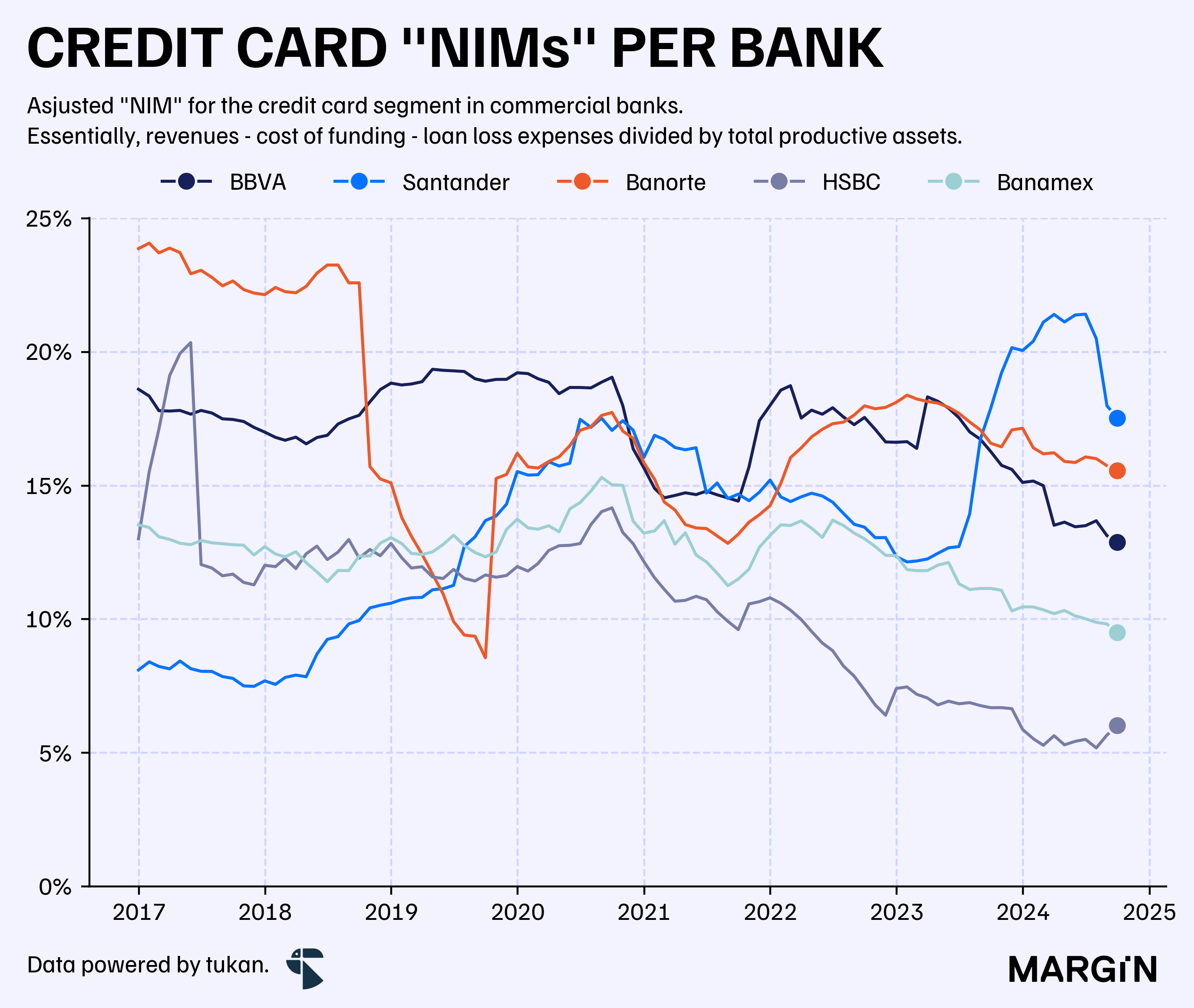

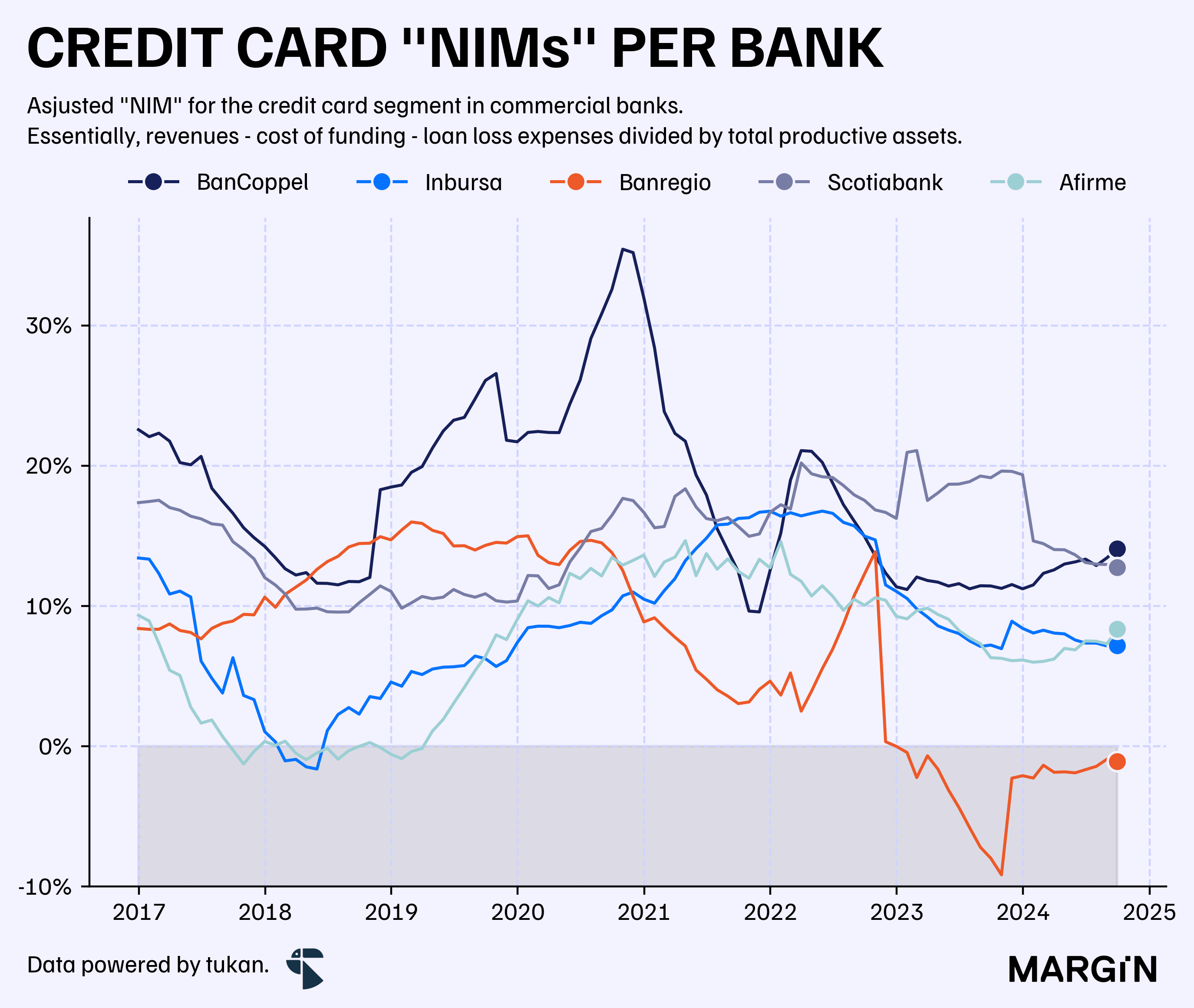

To address these questions, we estimated an “adjusted net interest margin (NIM)” specifically for credit cards. For details on our methodology, we’ve included a spreadsheet at the end of the article, available exclusively to our paid subscribers.

Here’s what we discovered:

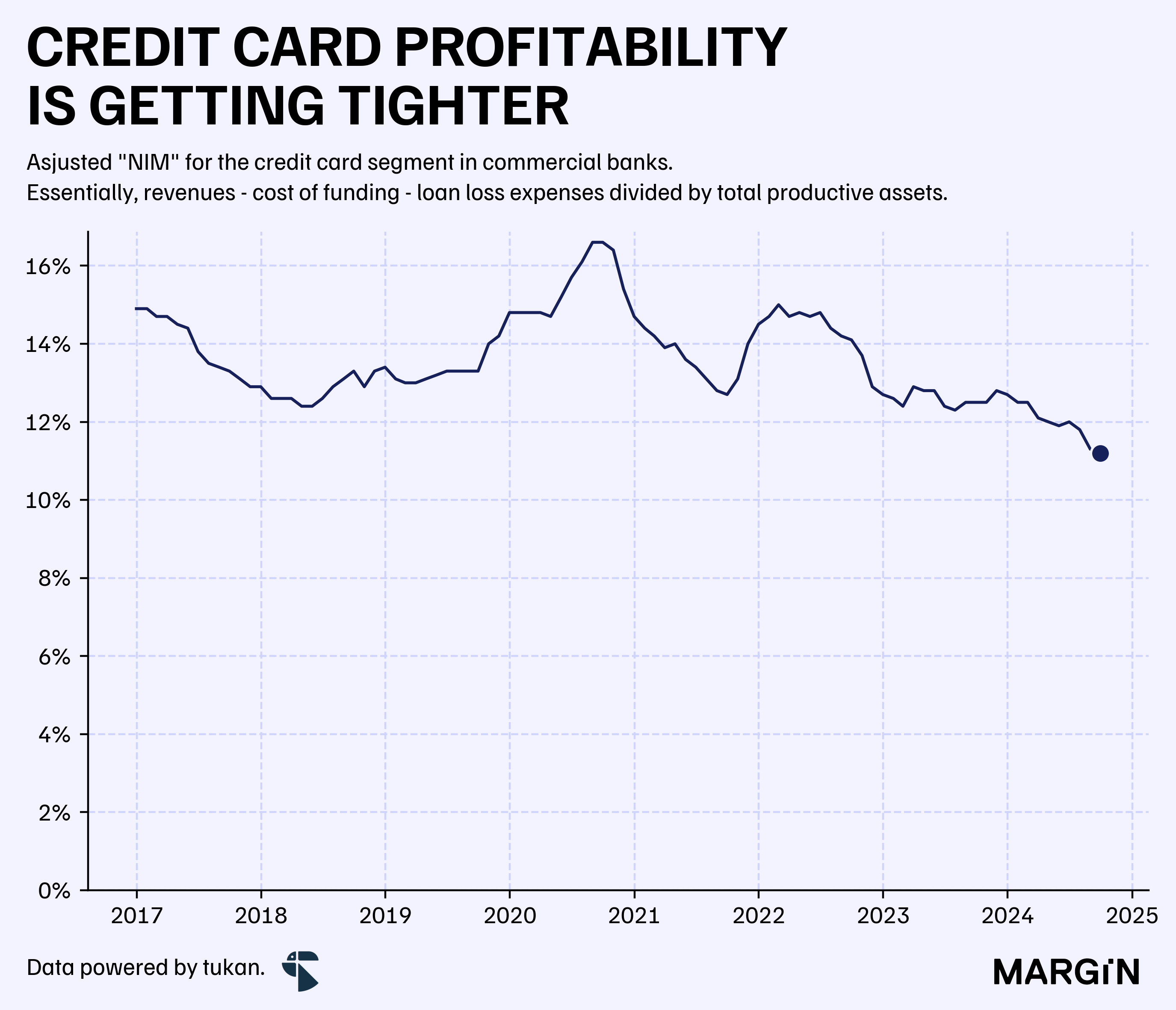

According to our estimates, the “net interest margin” for credit cards, adjusted for loan loss provisions, stands at 11.4% for the commercial banking system as a whole. This represents a decline of 113 basis points compared to the previous year and nearly 500 basis points below the historical high observed in 2020.

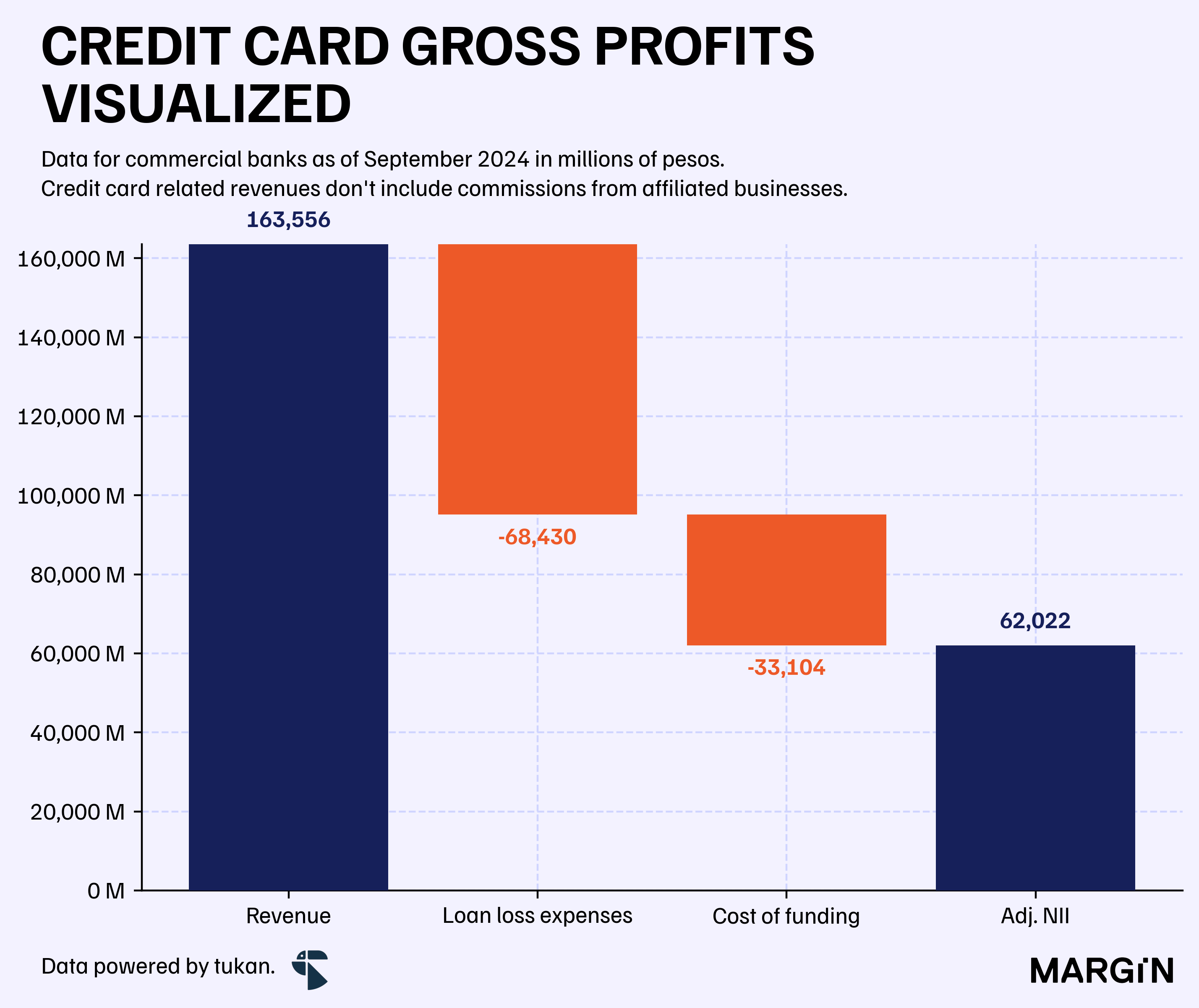

To arrive at this figure, we calculated total credit card-related revenues, subtracted the interest expense required to fund those loans (based on the bank’s cost of funding rate), and deducted provisions for expected losses on the portfolio.

In terms of “gross profit”, this translates to a margin of approximately 38% of total revenues, before accounting for marketing and general operating expenses. For context, one of the most efficient commercial banks in the country, Inbursa, allocates roughly 22% of total revenues to operating and marketing expenses, while the broader banking system is currently spending close to 46%.

We believe this exemplifies the major challenges fintechs face when attempting to compete and become profitable at the same time within this market. Especially when they face considerably higher funding costs than regulated players, which should put even more pressure on margins.

According to our calculations, the highest funding cost the “product” could sustain to remain at break-even point would be a funding rate of 16.5%, assuming an unchanged level of provisioning for expected losses and interest yields.

To make matters even more complicated, this “equilibrium” funding rate is further pressured, dropping to around 13.7%, if we consider that new entrants typically don’t charge commissions to attract users—a revenue source that accounts for about 10% of banks’ total revenues.

We found it quite surprising that these “equilibrium” funding rates are hovering near what Nu, Mercado Pago, Stori and Klar are offering their deposit base.

Not surprisingly, established banks which have been betting heavily on growing market share across the credit card line have also the lowest “NIMs”. Ualá and Banregio also stand out by recording negative net interest income for the product.

The case for Banregio is quite strange. Prior to 2022, the banks had quite a “healthy” position in terms of profitability for the product.

Weird…Hey?

All in all, we believe the key takeaway is that sustaining a profitable credit card operation is far more complex than it may initially appear.

Unit economics offer limited room for margin, particularly for those aiming to be pure-play credit card providers—especially when facing significantly higher funding costs compared to traditional banks.

Since at least 2020, many fintechs that initially launched with only a credit card product have either expanded their offerings to include additional financial products or sought banking or SOFIPO licenses. These measures aim to lower funding costs and enable a broader range of financing options for consumers.

For those unwilling or unable to diversify, the path forward looks particularly challenging.

Appendix

Please refer to the following spreadsheet for the calculation breakdown and other historical statistics per bank.

If you like what you’re reading, or have any ideas on topics you’d like us to explore, please let us know! You can share your thoughts in the comments or send your feedback directly to miguel@tukanmx.com. Your input helps us improve our content and deliver even more value to your subscription.

See you next week.