Bank'ed

Going deep into INEGI's latest financial inclusion survey.

A couple of weeks ago, INEGI and the CNBV published their latest Financial Inclusion Survey report (2024), a document spanning over 140 pages that contains extremely valuable insights on the current state of financial inclusion among the Mexican population.

While the document is quite thorough on its own, we decided to dive deeper into key topics that caught our attention.

We hope you find our analysis useful.

This post is exclusively for Margin subscribers.

If you’d like for us to create a corporate subscription for you team please contact us at miguel@tukanmx.com.

It’s a great investment to keep everyone on track of what’s happening with the Mexican economy.

Latest CNBV data shows that there are close to 138 million active funding banking accounts in the hands of the general public.1 This figure implies roughly 1.5 accounts per adult; and it doesn’t even consider the millions of contracts operated by digital wallets, SOFIPOs and SOCAPs in the country.

Generally, deposit accounts are considered the entry point into the financial sector. Once a person owns an account where they can receive funds, financial institutions then begin moving the client up the “funnel” of credit products.

INEGI’s latest financial inclusion survey estimates that 63% of the adult Mexican population currently owns a deposit (or savings) account — a rate 14 percentage points higher than in 2018.

For context, this estimates that 15 million people (when compared to 2018) opened a deposit account during the past 5 years — a figure equivalent to the combined population of states like Nuevo León and Veracruz.

This penetration rate would imply that an adult within the formal financial system would have (on average) more than 2 active deposit accounts. A figure which makes a lot of sense, at least, on paper.

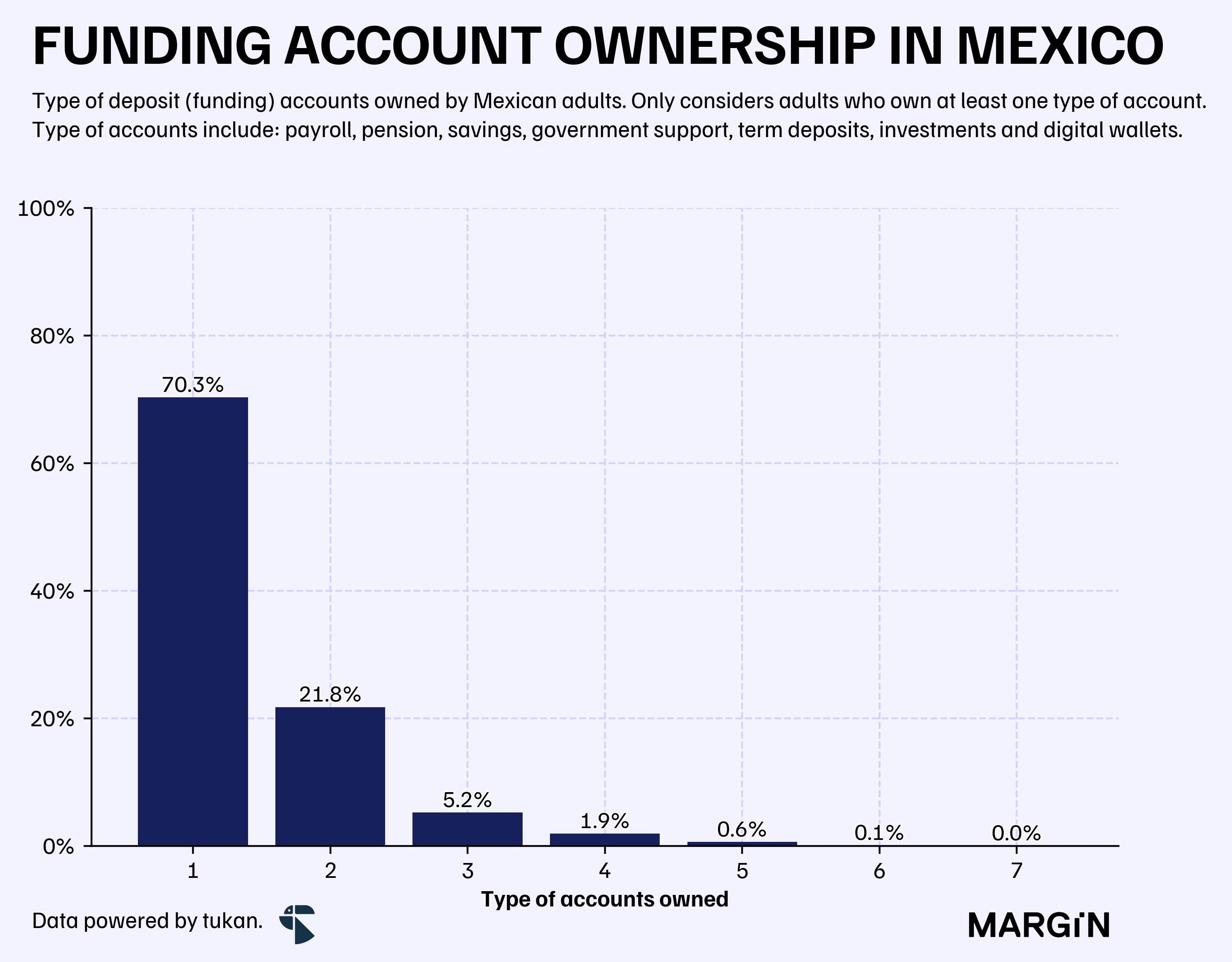

This is further backed by the ENIF (Encuesta Nacional de Inclusión Financiera) which suggests that close to 30% of Mexicans with a deposit account have 2 or more different types of accounts — for example, a payroll account, and a fully-digital account (Nu, Mercado Pago, Stori, etc.).

This refers to the number of types of accounts they hold, not the total number of accounts. For example, a person could have only one type of account (i.e. payroll) but with multiple banks.

As expected, most of the population begins their relationship with the financial system through their payroll account (81%). That is, the account which is chosen by their employer when that person enters the formal job market.

This has generated a massive moat for banks that hold relationships with large corporates in the Mexican market. In fact, CNBV data shows that 88% of the country's total payroll accounts are in the hands of just 5 players.

And in turn, has translated into banks overlooking regions of the country where there are high rates of informality.

If you’re interested on this topic we did a deep dive on the relationship of informality and banking accessibility in October.

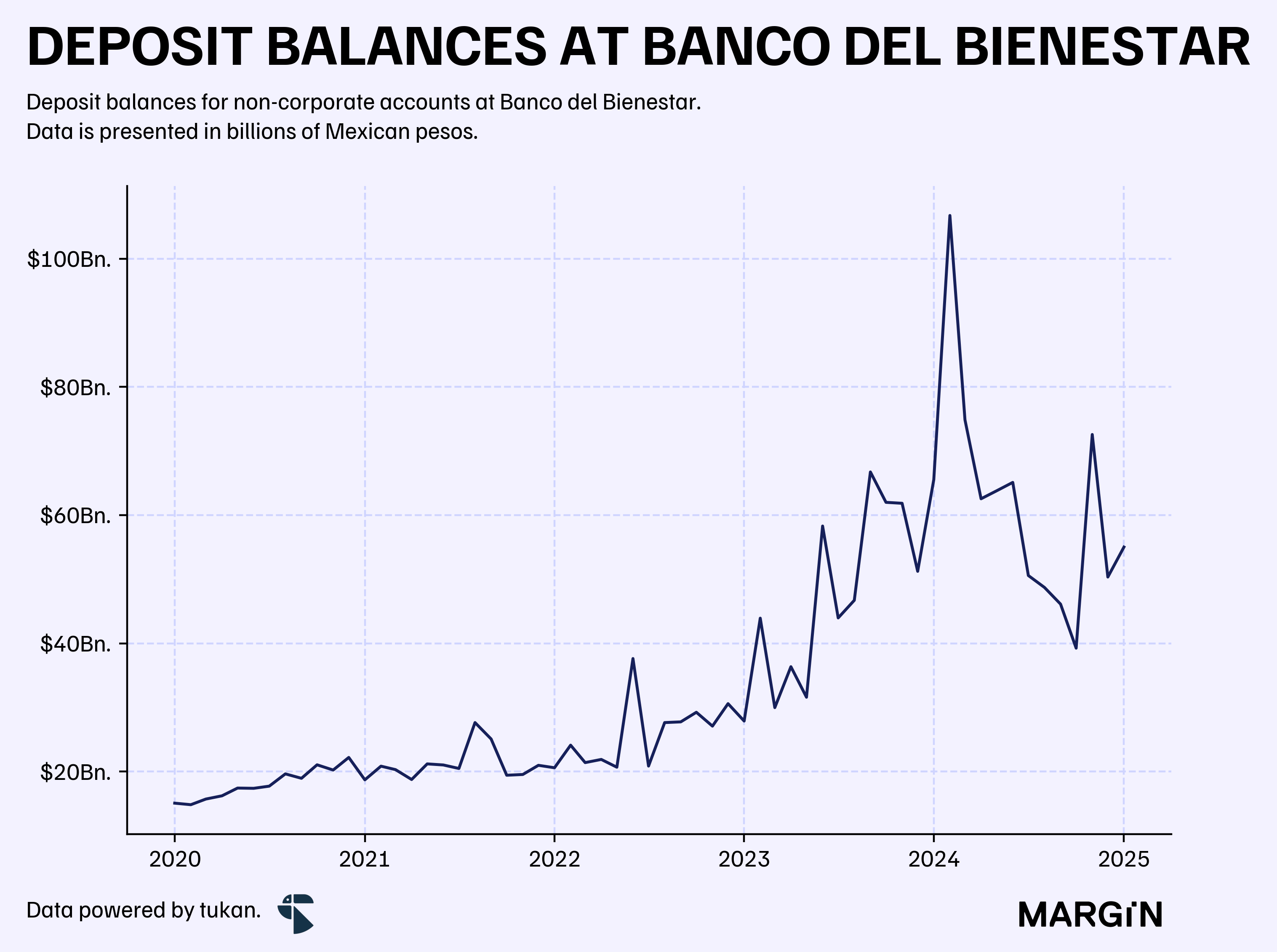

This partially explains why during the past 5 years, one of the major drivers of financial inclusion in the country have been government support programs. According to the ENIF, 11% of the population opened their first account to receive funds from the Mexican government.

To visualize the impact of this phenomenon take a look at the chart below which shows the evolution of deposit balances for Banco del Bienestar since 2020.

According to data from the CNBV, el Banco del Bienestar currently has more than 19 million accounts and over $37 billion pesos in demand deposits and close to $17 billion pesos in time deposits from the general public.

For context, a bank like Banregio would have $25 billion in demand deposits and $75 billion in time deposits from non-corporate accounts.

Then there’s the effect from digital account such as Nu, Mercado Pago, Spin and Stori — companies, which according to INEGI, were responsible for banking 2% of the adult population.2

Much of this success has been driven by the insanely high yields offered by these deposit accounts in order to attract users and consolidate their place in the market.

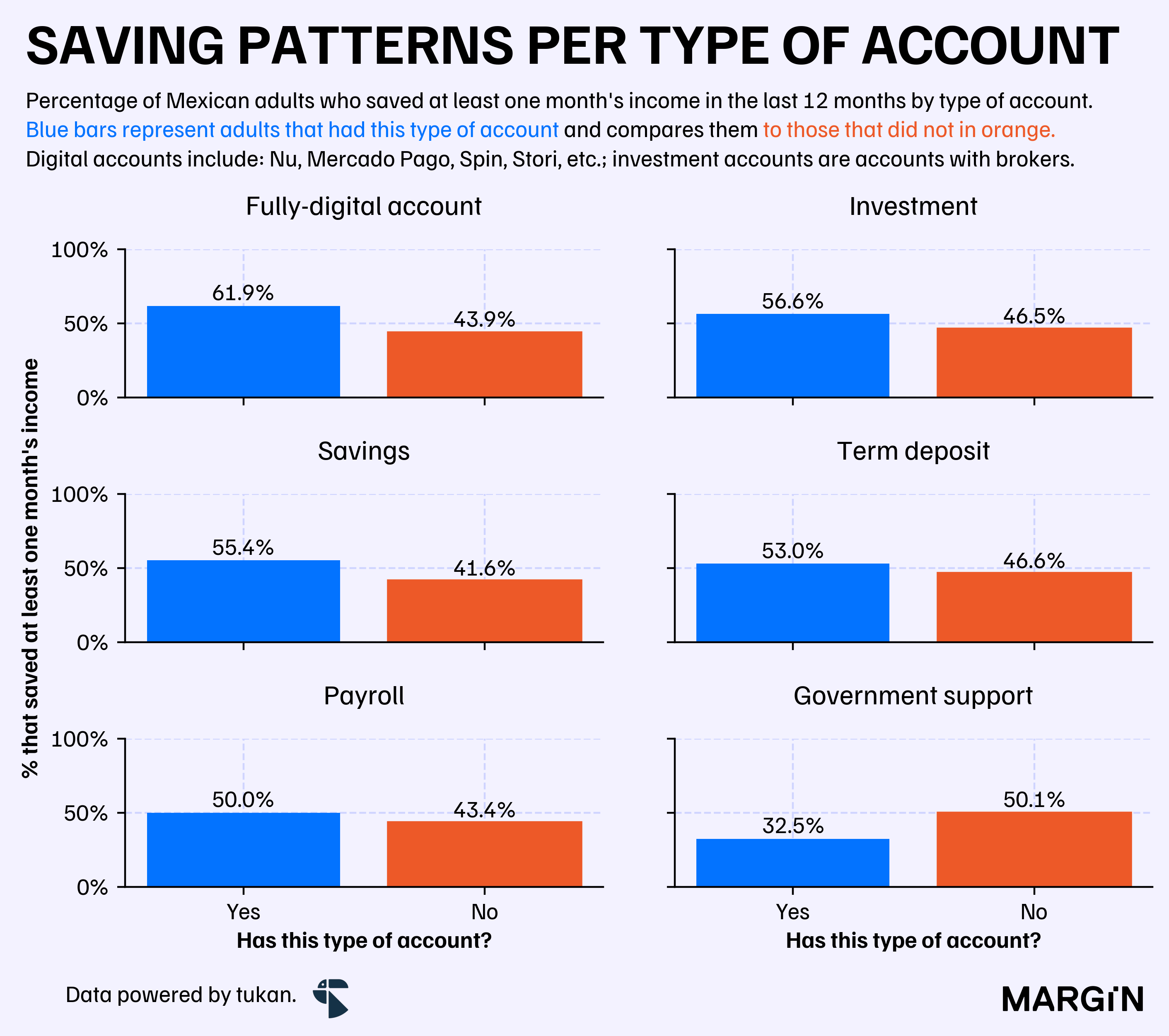

This in turn has had a positive effect on the saving patterns of the Mexican population — at least, according to the results of the ENIF. INEGI’s estimates suggest that adults who had a digital fintech account were more likely to save money than those who didn’t.

The chart below shows how 62% of people with a fintech account saved at least one month of their regular income during the past year — a rate almost 20 points higher than those adults who didn’t have this type of product (44%).

Surprisingly this was even higher than for other savings related products such as: investment accounts with brokers (GBM, Bursanet, etc.), or term deposit accounts.

In our opinion this is a massive result and is likely one of the major reasons behind the exponential growth of these services among the Mexican population.

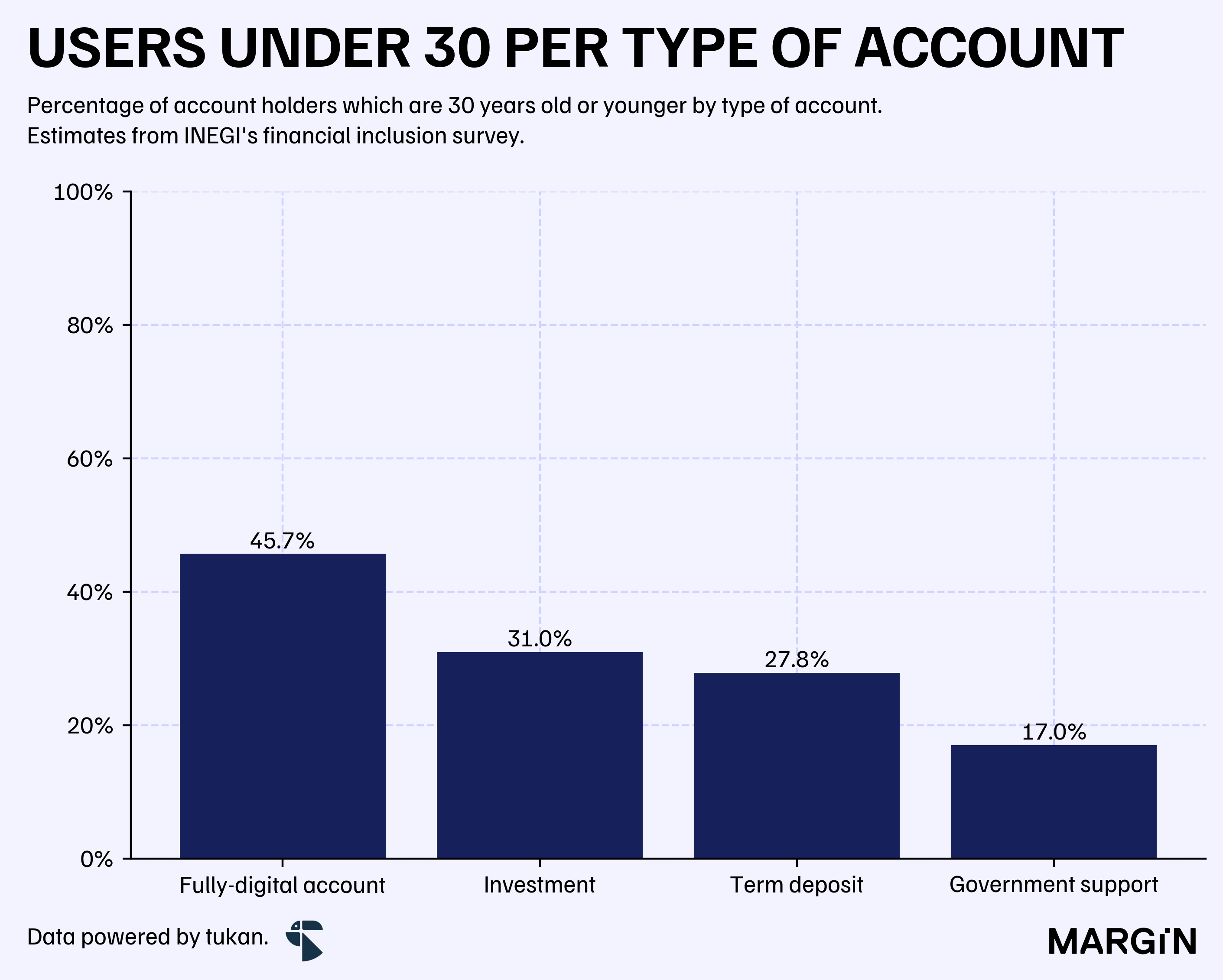

Furthermore, data from the ENIF points towards a much younger user base for clients of digital wallets. For example, 46% of fintech users are younger than 30 years old — a figure that contrasts heavily with the 31% and 28% recorded for users of investment and term deposit accounts, respectively.

Interestingly, at first glance, users of digital wallets don’t necessarily seem to have a similar customer profile to those targeted by major banks. Based on the survey’s data, only 50% of digital account holders also have a payroll account and for more than 20% of users this is the only deposit product that they own.

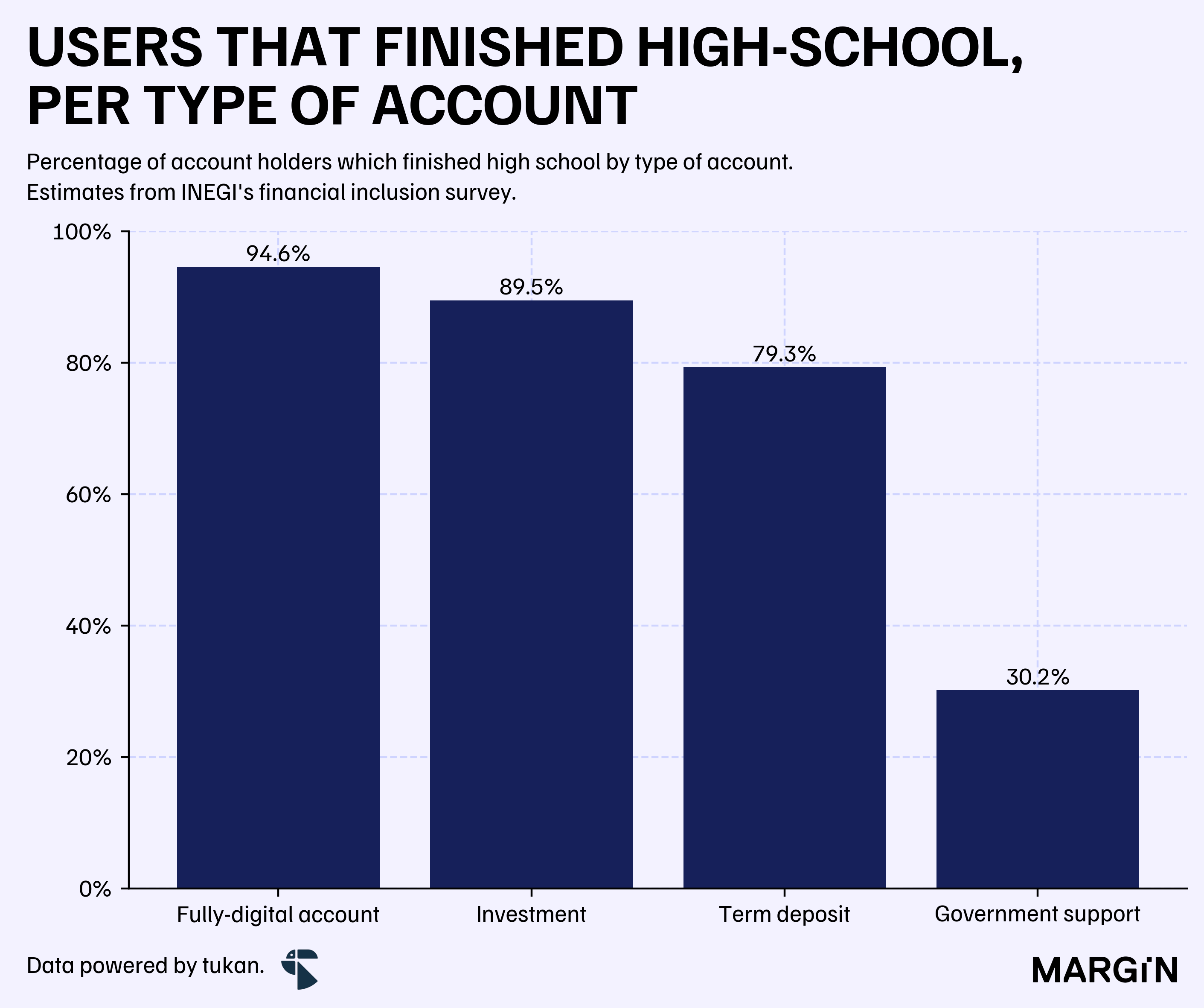

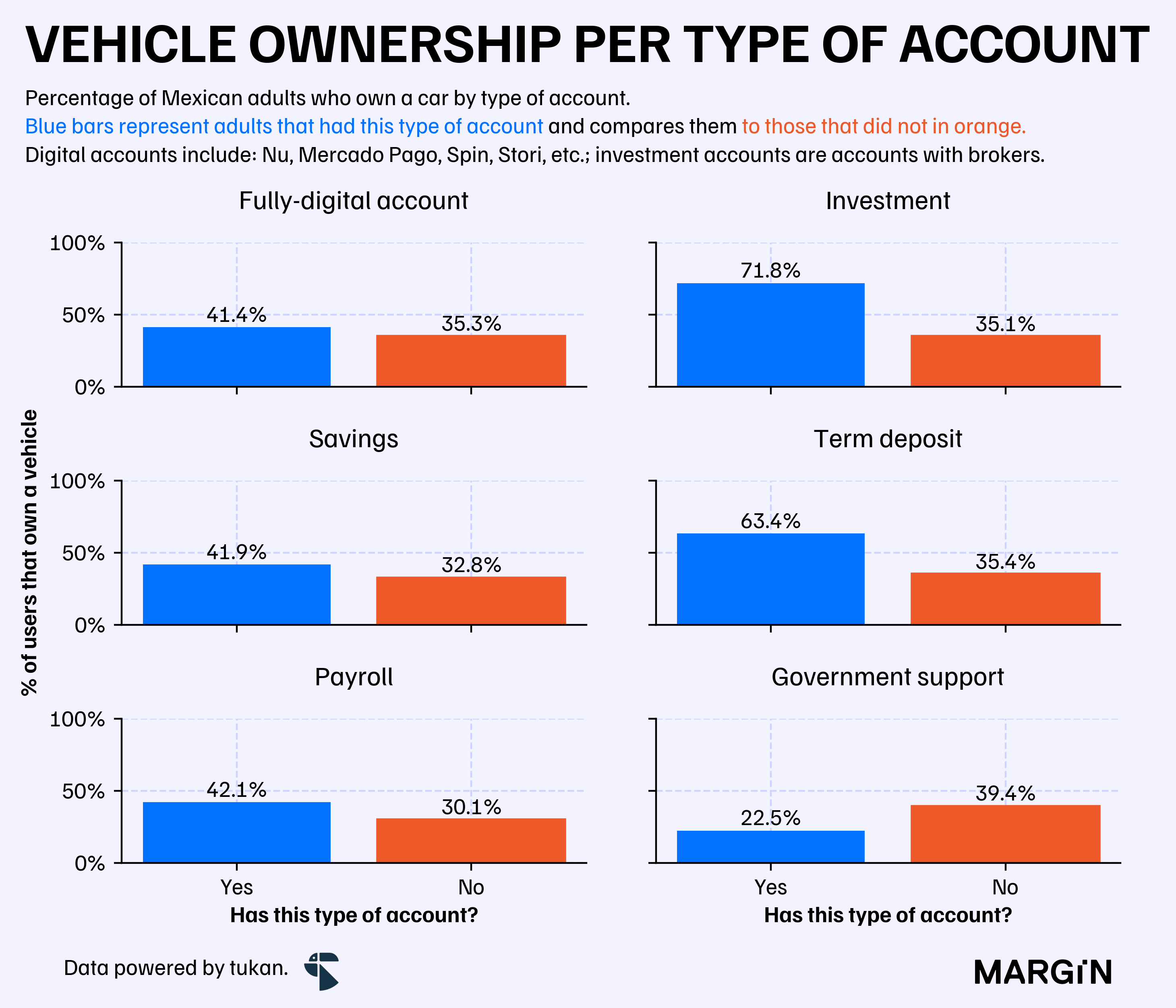

However, when digging deep into the data we can see that estimates point to almost 95% of customers having completed (at least) high school studies. Furthermore, almost half of users own a vehicle despite being much younger (on average).

Based on this data, we believe that digital wallet users are mostly highly educated young adults from the Mexican middle and upper class. The ideal customer profile for traditional banks.

Will we see these new entrants capitalize on this attractive user base when the time comes to offer them a mortgage or a payroll loan?

The upcoming banking licenses will certainly help.

Nonetheless, we believe that banks and fintechs will likely end up fighting for the same user base that legacy banks have always coveted. Just under different terms and on a different “battlefield”; the truly underbanked, however, will most likely depend on the development of physical financial infrastructure from development banks and maybe, just maybe, the strategy implemented by Spin.

We’ll have to wait and see.

We think that (as of today) there’s only one fintech that can truly “bank” the underbanked population in Mexico, and that’s Spin by OXXO.

Across both commercial and development banks.

I.e. that the first account opened by that person was a digital account by one of these companies.