Monday, On the Margin

IGAE; non-financial services; trade; imports & exports; construction; natural gas price index; and employment.

Slowdown

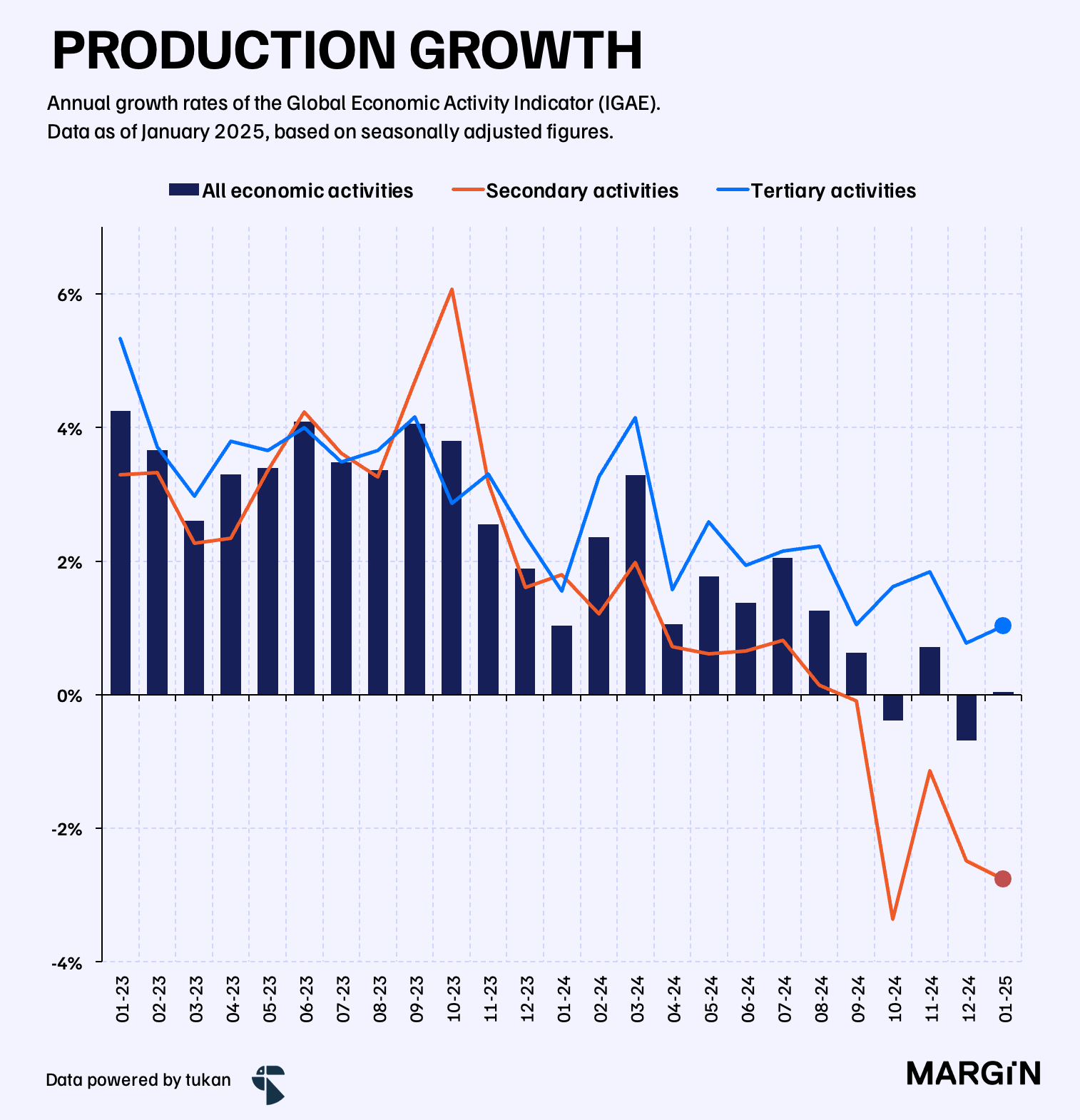

INEGI’s IGAE index — a short-term proxy for GDP growth — came in flat YoY during the month of January. On a sequential basis, Mexico’s economic activity decreased by 0.2% (MoM)1.

The slowdown was mostly explained by a strong contraction on the mining and construction industries; plus, tepid growth in the country’s trade and service industries. The double-digit increase for the agricultural sector was barely enough to offset a decline in overall growth.

Last week we explored how manufacturing in the country is showing increasingly worrying signs of deceleration. This week, we focus on analyzing the performance of other major industries such as: services and trade.

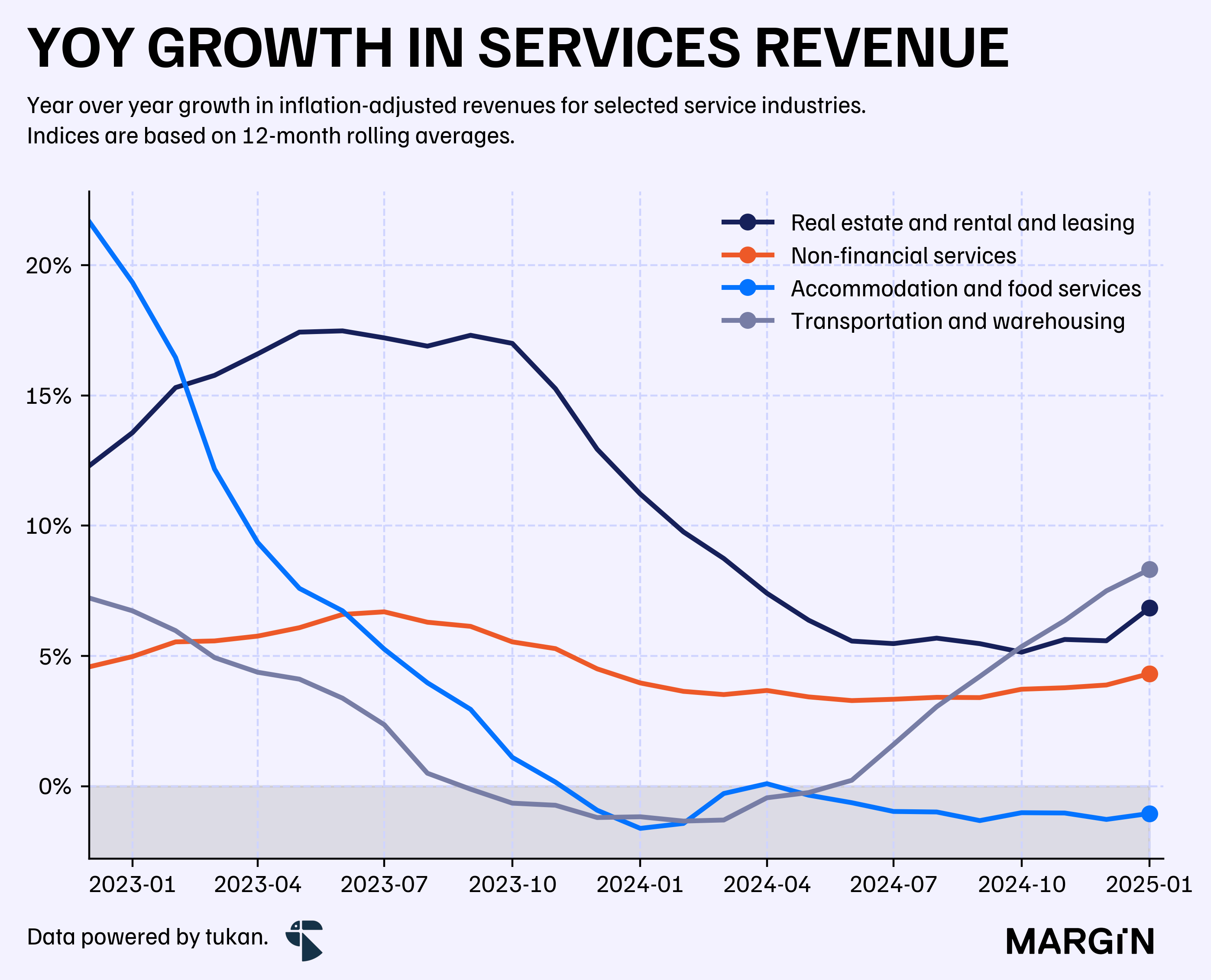

Non-financial services continue to show some resilience amidst a tough economic environment (+7% YoY revenue growth in January)2. The main boost coming from real estate and leasing services; plus, a resilient transportation sector (+3% YoY).

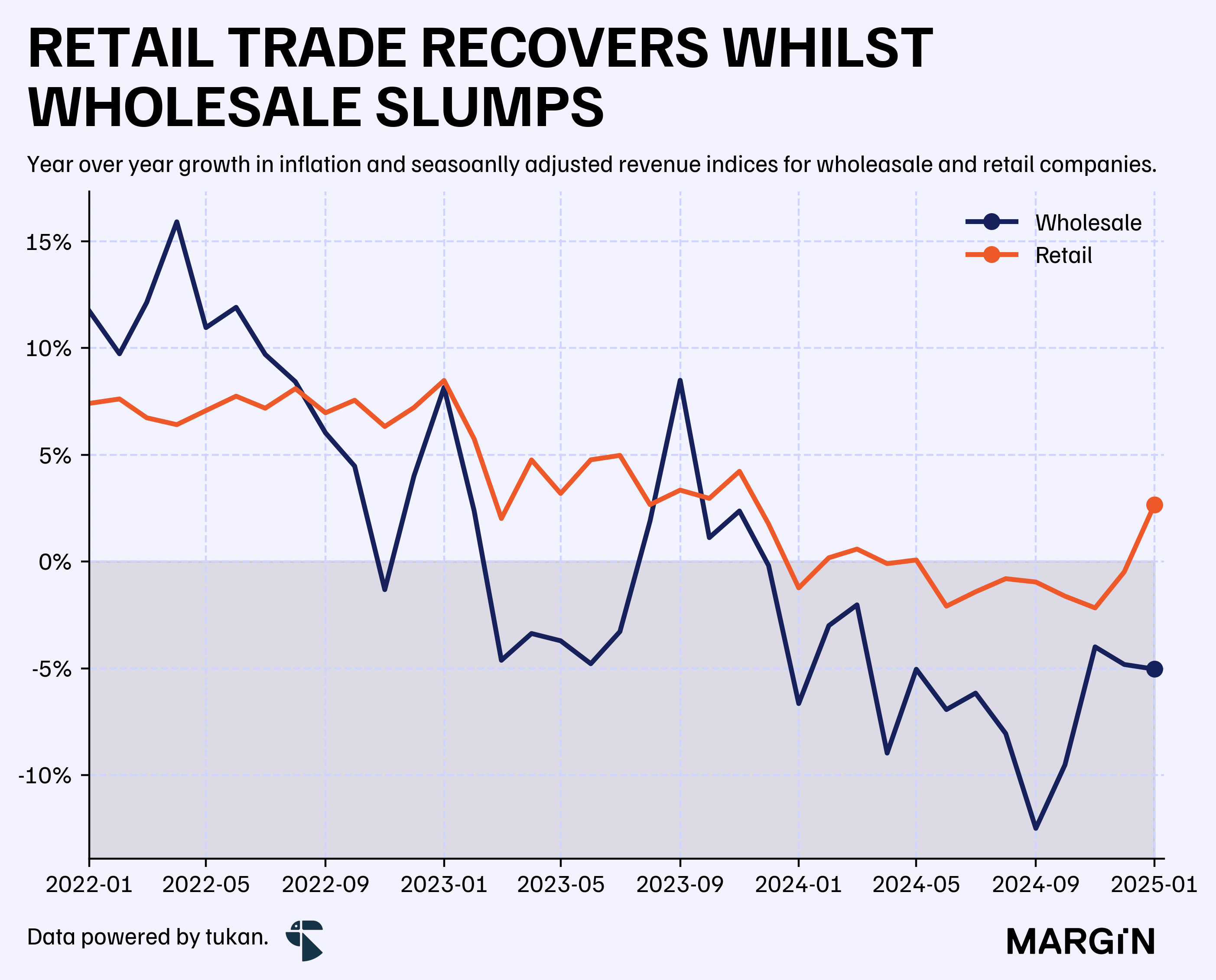

In contrast, wholesale companies continue to struggle during the beginning of the year as they reported a 5% annual decline in inflation-adjusted revenues. As of January, these companies have now posted 14 consecutive periods of annual contractions.

Meanwhile, retail revenues rebounded by 2.7% YoY, breaking a streak of 7 consecutive months of declines since June 2024.

A significant boost to revenue recovery over the past year came from online sales, which grew by 19% YoY.

If you're interested in the e-commerce market in Mexico, don't miss our recent article where we analyze key statistics to understand the online boom.

Despite the recovery in the macro indicator, we have reasons to believe that retail sales in February could be set for a major slump when INEGI posts data for next month as card transaction data for big-box stores declined for the first time ever (excluding COVID) during the second month of the year.

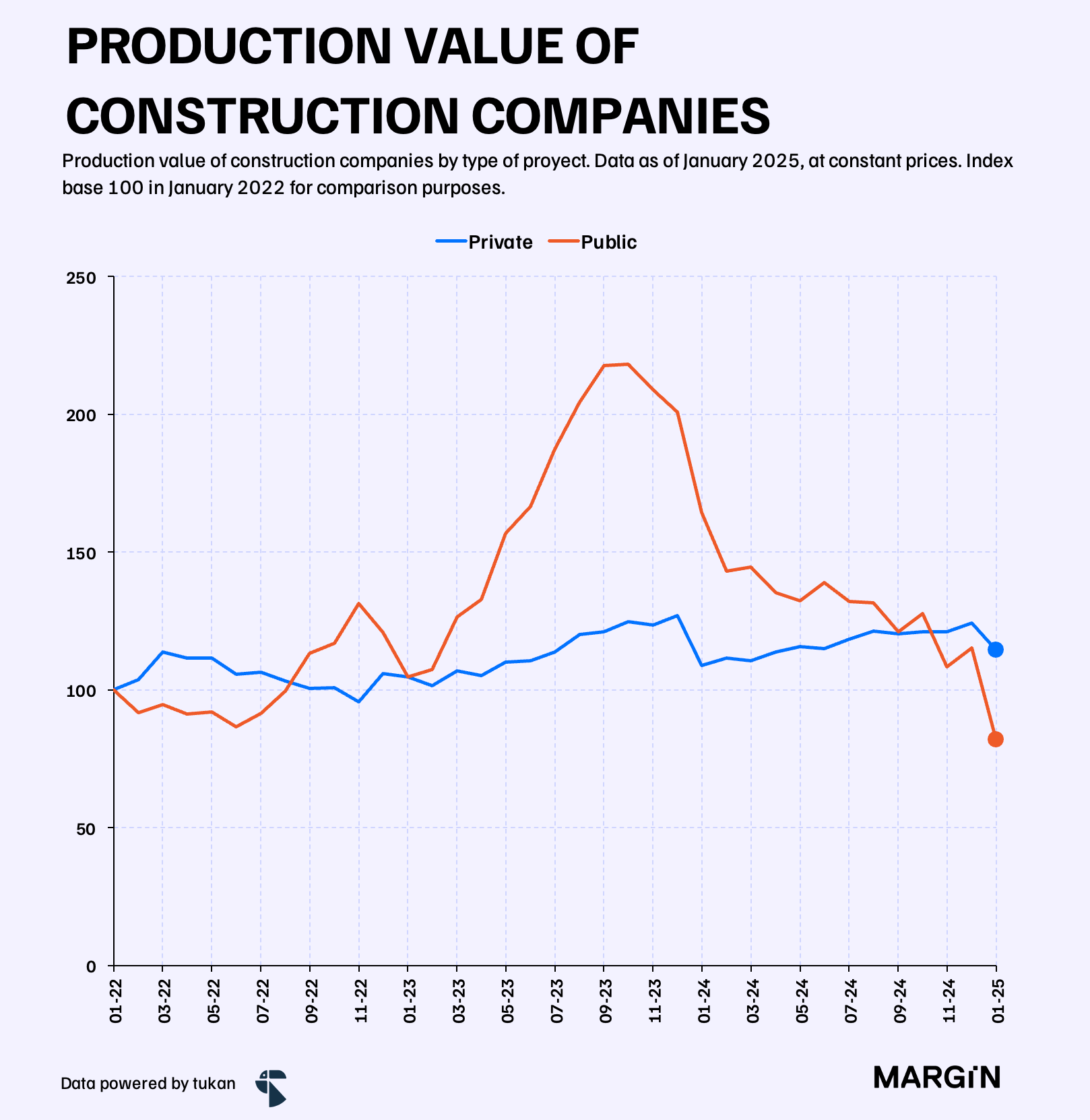

Construction companies show an even greater deterioration. Seasonally adjusted figures indicate a 4.2% MoM and a 19.2% YoY decline in production value during January of this year3. This downturn is entirely due to the performance of public projects, where production fell by approximately 50% YoY in real terms, marking nine consecutive months of double-digit annual declines.

On the other hand, production in private sector construction projects rebounded by 5% in the first month of the year, following four months of annual declines in real terms.

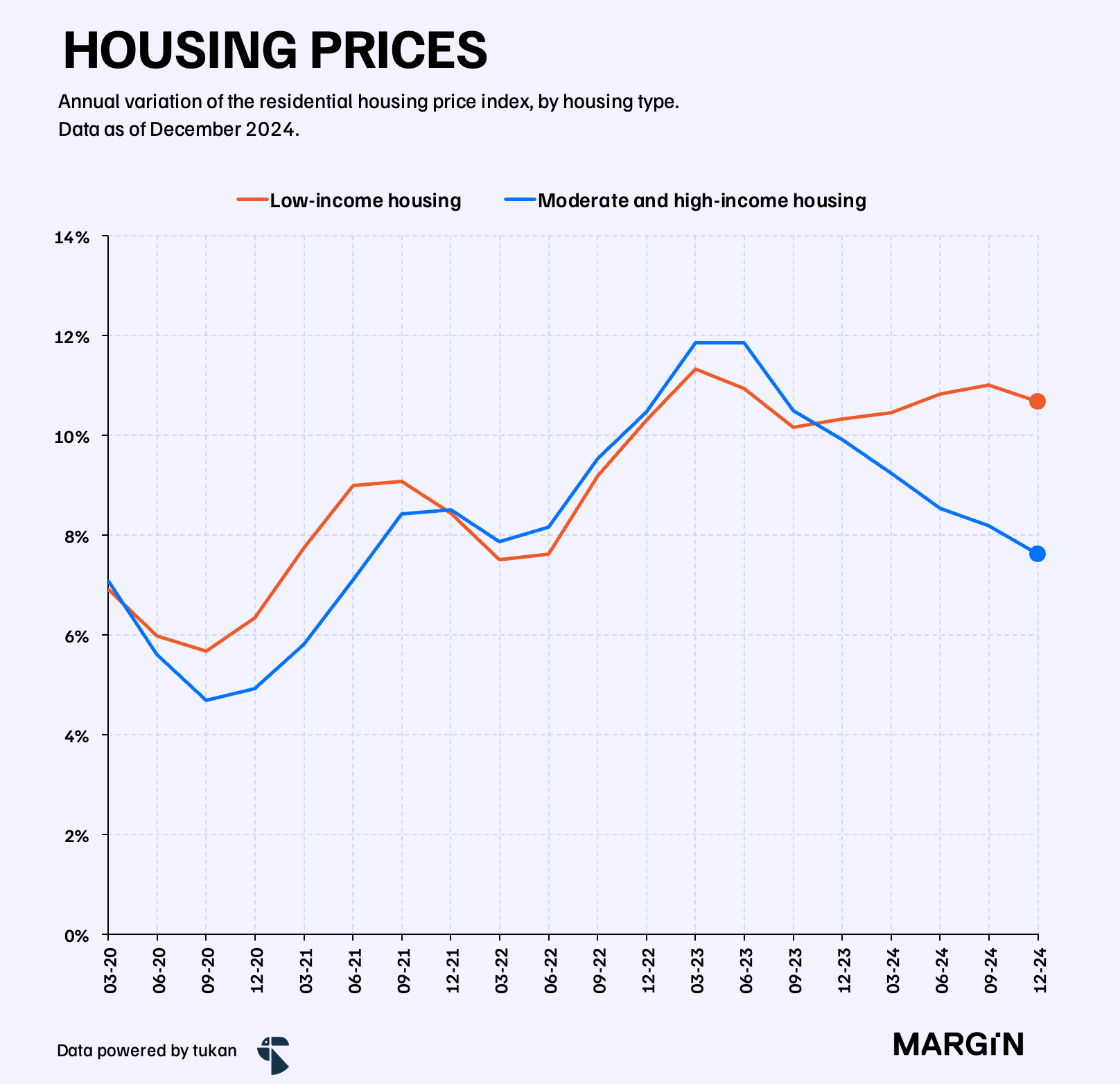

The recent change in the growth trend of home construction is unfolding amid persistent inflation in housing prices, particularly for low-income homes. By the end of 2024, the housing price index for these properties had risen to 10.7%, compared to 7.6% for medium-to-high-income homes, while the overall inflation rate remained around 4.5%.

Trade balance

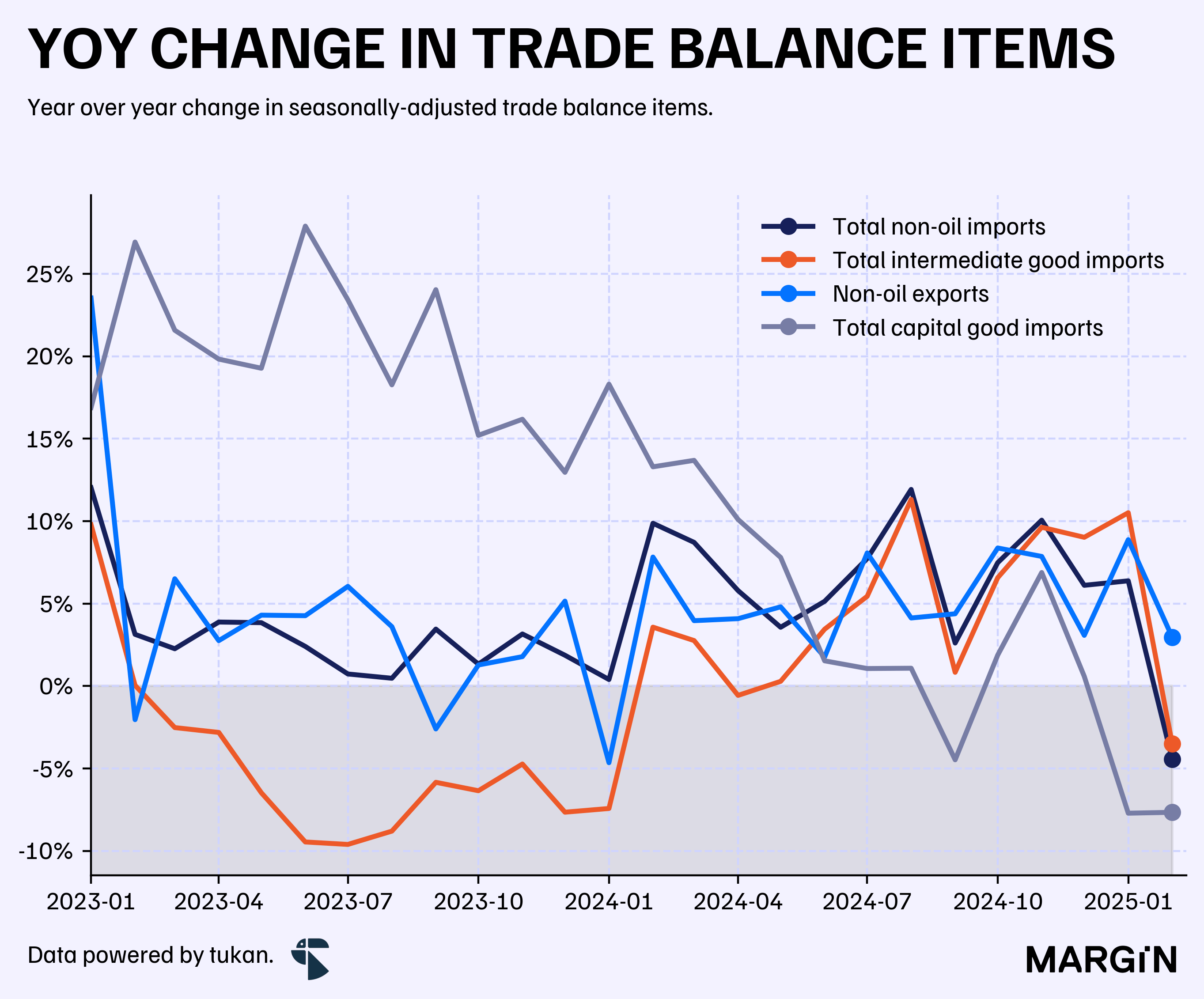

Exports and imports declined during February according to preliminary and non-adjusted data from Mexico’s trade balance statistics.

Non-oil imports declined by 8% YoY, affected mainly by a strong contraction in intermediate goods — i.e. goods imported into the country for transformation into finished goods.

We also saw capital good imports (machinery and equipment) decline for the second consecutive month at high-single digit rates.

Similar to imports, Mexican non-oil exports also declined in February, albeit, at a smaller rate (-3% YoY). However, this could be explained by seasonality effects as INEGI’s estimates on seasonally adjusted data showed a slight YoY expansion on non-oil export figures.

Worryingly, automotive exports declined by almost 15% YoY during February.

Natural gas

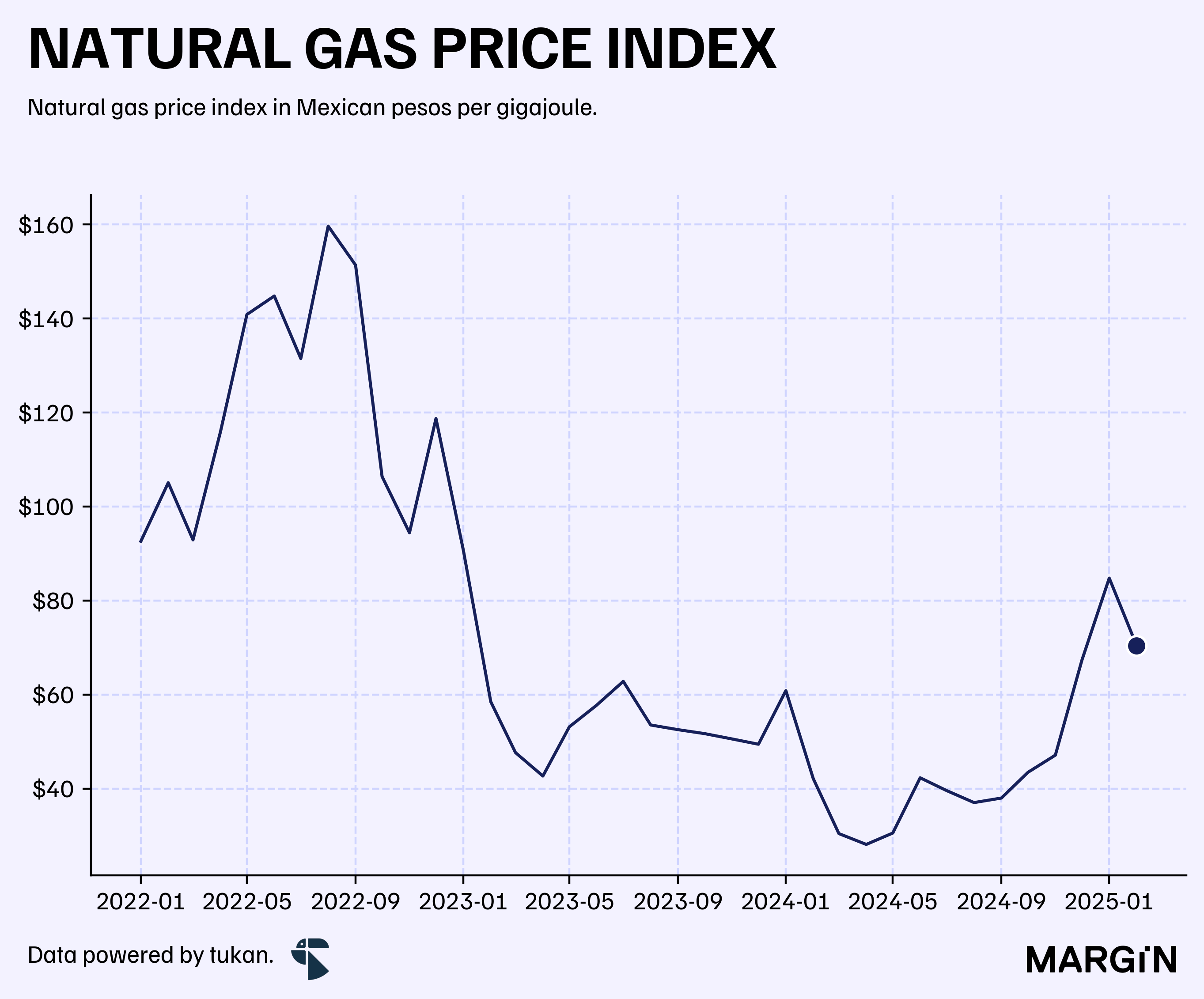

The price of natural gas corrected slightly after continuous increases in the last few months of 2024 and January 2025 according to data from the Comisión Reguladora de Energía.

After remaining relatively low throughout 2023, natural gas prices began to rise in late 2024, primarily due to climate-related factors that boosted demand. However, upward pressure on prices may intensify in the coming months, given the heavy reliance on imports from the United States and low domestic production.

Remittances

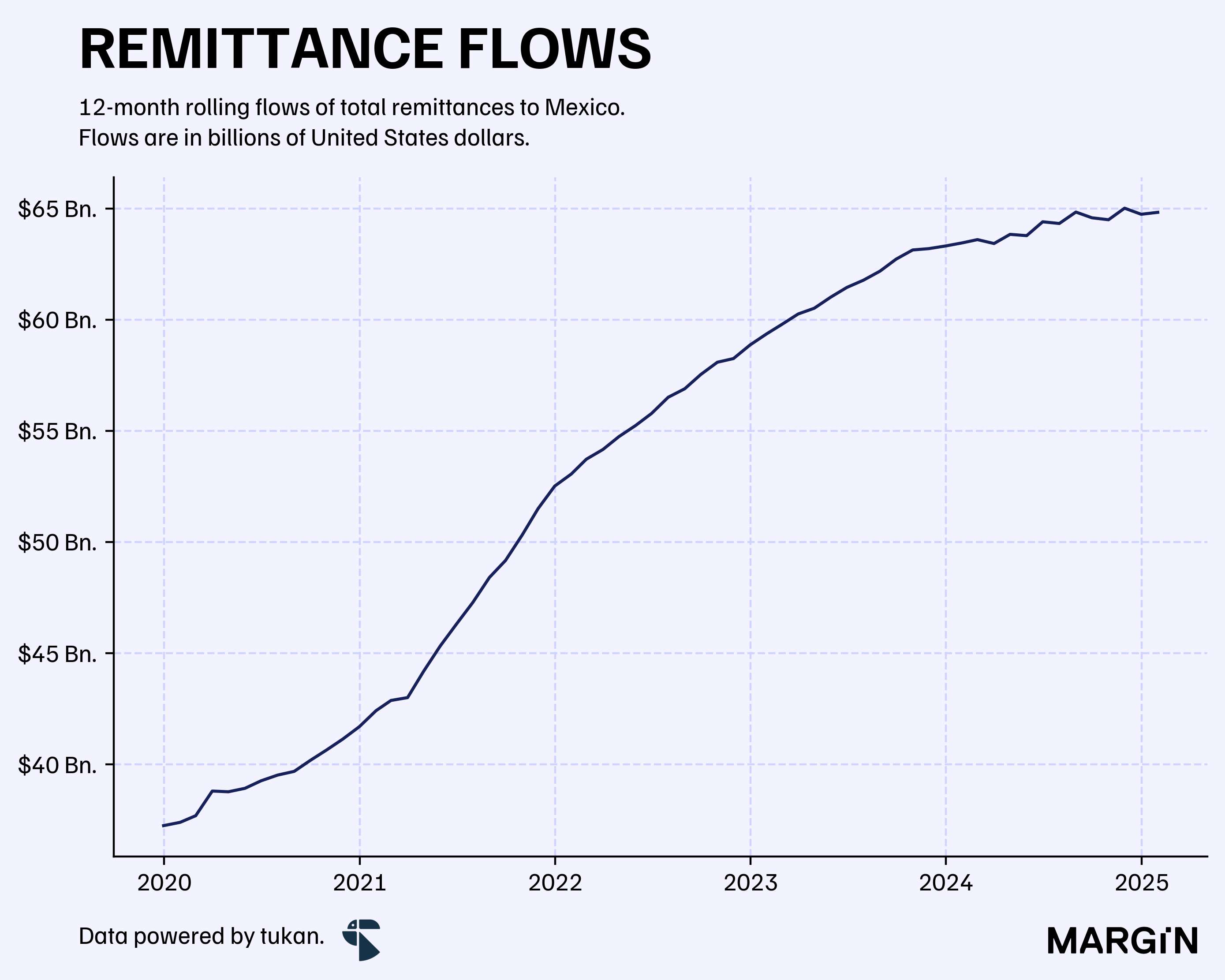

Remittances during January came in at $4.6 billion USD (+2% YoY).

Based on 12-month rolling flows, total remittances amounted to $64 billion USD — +2% YoY, and showing slight signs of deceleration against long-term growth trends.

Based on seasonally adjusted data.

According to seasonally adjusted figures.

Adjusted for inflation.