Monday, On the Margin

Financing the Mexican manufacturing industry.

Presented by:

Last week’s holiday of Semana Santa paused many statistical releases on Mexican macro and financial datasets.

Aside from seeing manufacturing rise by 1.4% YoY (on a seasonally adjusted basis); and pension funds recording an 18% annual growth rate on net assets1, there is little to highlight this week with regards to data published during the holidays.

This is why this Monday we decided to write a short essay exploring the changes in financing opportunities for manufacturing companies in Mexico since the end of the pandemic.

We think the data raises some interesting questions.

In case you missed it, we published an update on the state of Mexican non-regulated SOFOMs last week.

Mexican manufacturing’s credit-to-GDP ratio stands at 10.2% — a figure in line with the non-manufacturing economy.

Between 2010 and 2019, Mexico’s manufacturing industry saw dramatic financing growth, with loan-to-GDP ratios surging from 9.0% to 12.7% over 9 years. However, this statistic has significantly contracted since the impact of the pandemic — with credit-to-GDP ratios decreasing by over 2 percentage points in the span of 4 years.

At the same time, the “credit penetration” ratio has remained flat for the rest of the economy.

What could be going on?

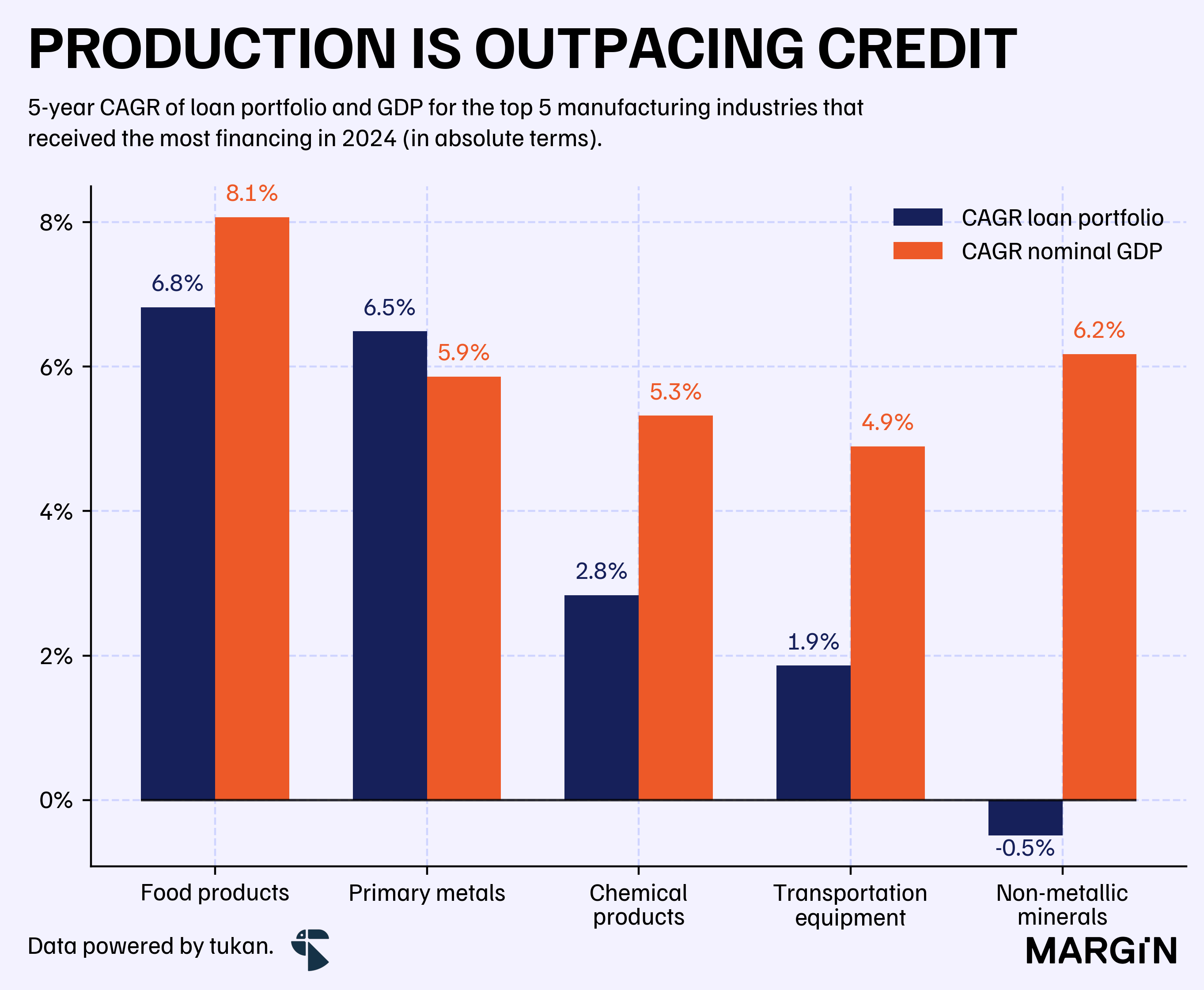

According to Mexico's central bank data, 4 out of 5 of the top-funded manufacturing subsectors have experienced shrinking loan-to-GDP ratios over the past 5 years.

These five leading subsectors represent 64% of total bank loan exposure to manufacturing as of 2024.

With only food and primary metal manufacturing as exceptions, loan portfolios for these critical sectors have grown below inflation rates — or even contracted outright. Implying real-term financing contractions for these key sectors in the Mexican industrial landscape.

The bigger picture reveals economic growth outpacing bank financing availability across most industrial subsectors.

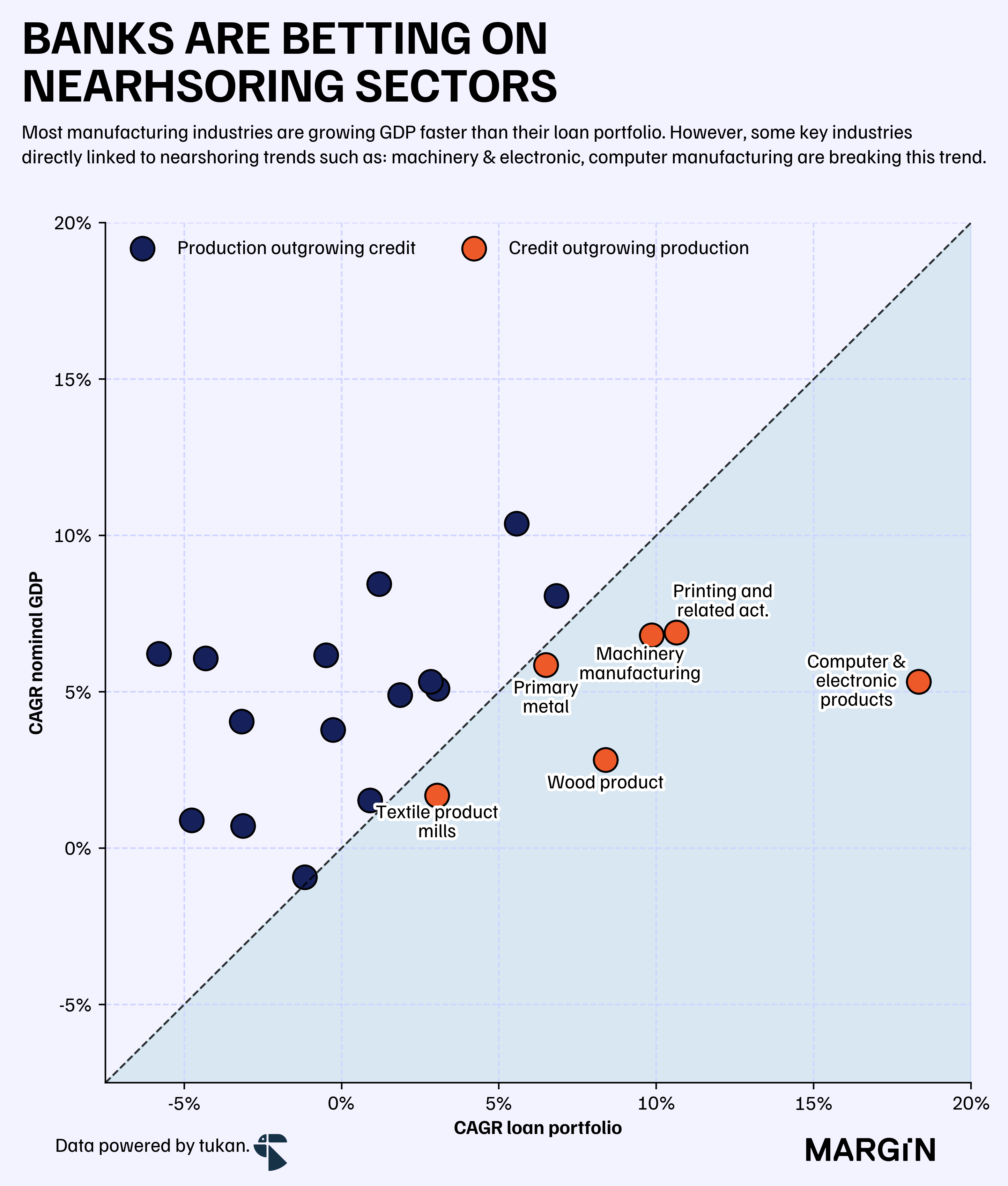

Yet, two significant outliers emerge directly linked to nearshoring trends: machinery and computer, & electronic equipment manufacturing. These subsectors have bucked the trend, posting double-digit 5-year CAGRs in their loan portfolios — translating to at least 61% total loan growth over the five-year period.

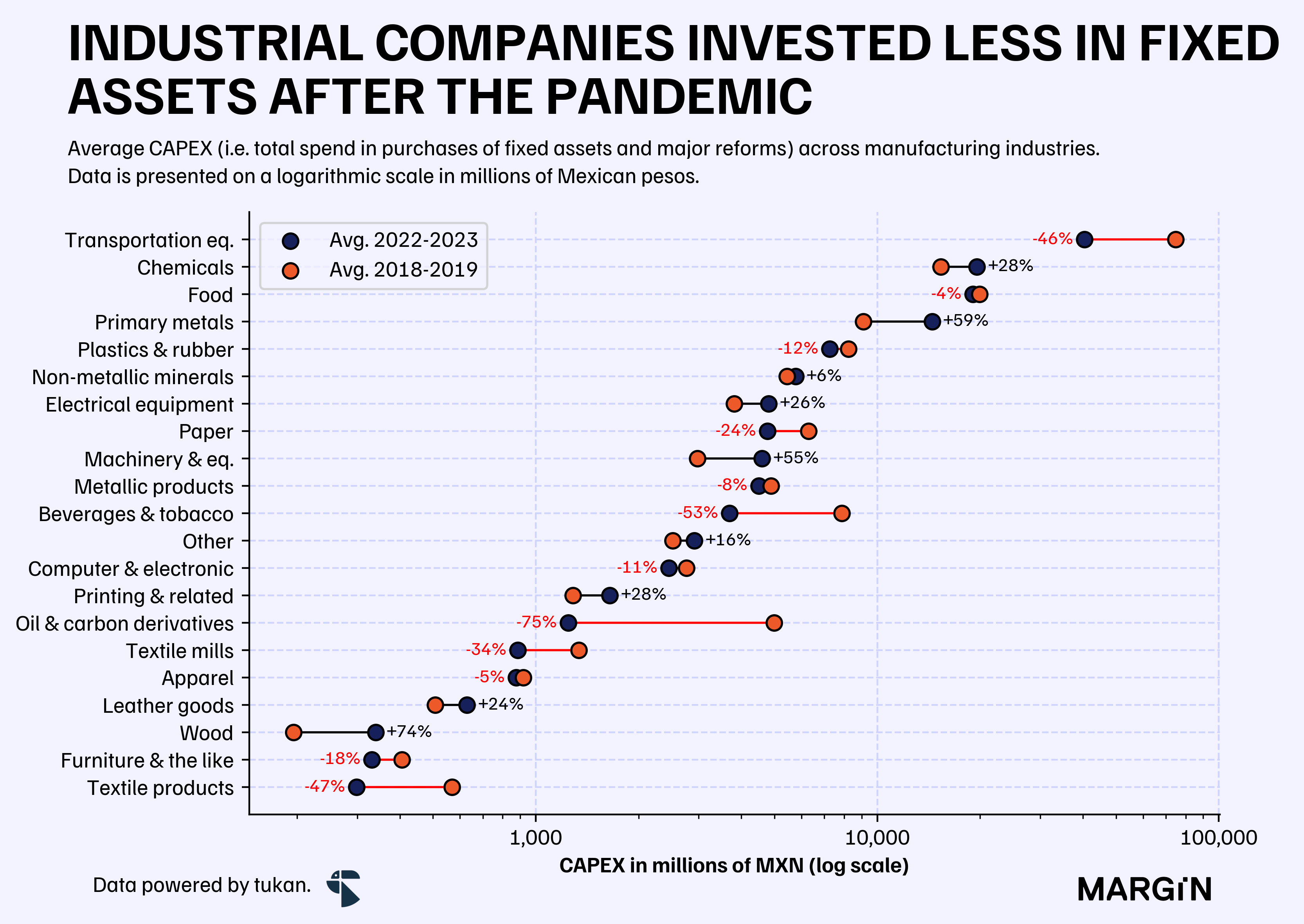

Interestingly, INEGI’s CAPEX estimates for manufacturing companies in the country have also posted a strong contraction when compared to pre-pandemic figures. According to the latest data, the manufacturing sector (as a whole) invested an average of $140 billion Mexican pesos in fixed assets during 2022 and 2023 — a figure 20% lower than the one averaged between 2018 and 2019.

Furthermore, most industries where credit is outpacing growth also recorded expansions in their CAPEX figures according to INEGI. The big exceptions being:

Computer & electronic products, which saw CAPEX figures decline by 11%.

Textile product mills, who recorded a CAPEX contraction of over 47%.

On the other end, we saw these industries recording significant CAPEX expansions; but little (to none) growth in terms of financing:

Leather product manufacturing saw CAPEX increase by 24%, but loans contracted by almost 15%.

Chemical manufacturing registered a 28% expansion in CAPEX figures and 29% in GDP growth but just a 15% expansion in total financing.

Whether this contraction is coming from the supply or demand side is still unclear.

That is, are companies spending less in fixed assets because they’re not receiving enough financing or are they not receiving enough financing because there is no need to invest in fixed assets?

Furthermore, we’re also missing data from financing opportunities outside the realm of commercial banks. Non-regulated SOFOMs, for example, have grown their loan portfolios by over 20% since 2019 — and are traditionally associated with providing credit opportunities to SMEs.

It’s quite possible that most of this gap may be being served by other players outside of the banking space. If not, are the conditions there for an attractive opportunity?

Presented by:

tukan is the premier platform for data-driven strategists operating in the Mexican financial industry.

We’ve processed, cleaned and standardized over 300 datasets from public sources so that you and your team can:

Automate your benchmarking analysis against competitors.

Find opportunities for growth within the noise.

Reduce risk with hundreds of economic and sociodemographic indicators at a municipal and industry level.

Dozens of financial companies trust us as an input to their strategy, including 3 of Mexico’s top 5 banks.2

Schedule a call with us to see how we can help.

Profuturo grew by almost 23% YoY during March and sits now just 1% below Banorte’s XXI in the race to become the country’s largest pension fund.

In terms of total assets.